Howard Marks put it nicely when he said that, rather than worrying about share price volatility, 'The possibility of permanent loss is the risk I worry about... and every practical investor I know worries about.' It's only natural to consider a company's balance sheet when you examine how risky it is, since debt is often involved when a business collapses. Importantly, Anchorstone Holdings Limited (HKG:1592) does carry debt. But should shareholders be worried about its use of debt?

When Is Debt A Problem?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. If things get really bad, the lenders can take control of the business. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. By replacing dilution, though, debt can be an extremely good tool for businesses that need capital to invest in growth at high rates of return. The first step when considering a company's debt levels is to consider its cash and debt together.

View our latest analysis for Anchorstone Holdings

What Is Anchorstone Holdings's Net Debt?

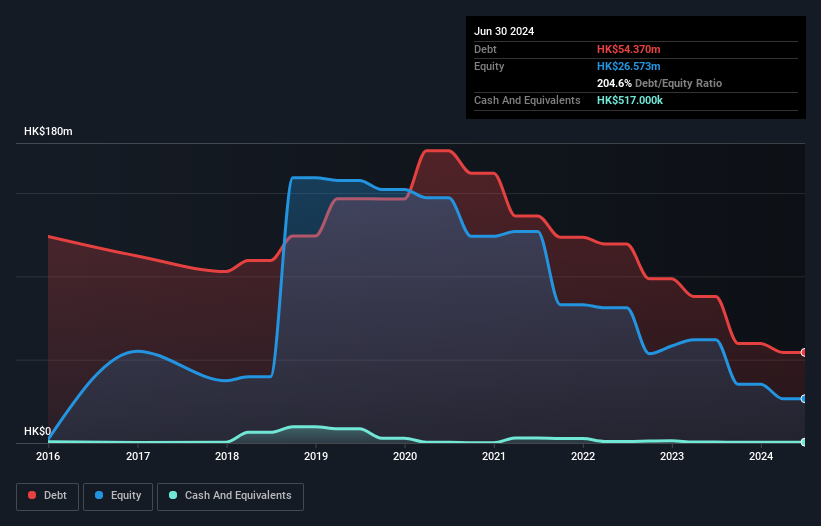

The image below, which you can click on for greater detail, shows that Anchorstone Holdings had debt of HK$54.4m at the end of June 2024, a reduction from HK$87.9m over a year. And it doesn't have much cash, so its net debt is about the same.

How Strong Is Anchorstone Holdings' Balance Sheet?

We can see from the most recent balance sheet that Anchorstone Holdings had liabilities of HK$143.6m falling due within a year, and liabilities of HK$20.8m due beyond that. On the other hand, it had cash of HK$517.0k and HK$131.1m worth of receivables due within a year. So it has liabilities totalling HK$32.8m more than its cash and near-term receivables, combined.

While this might seem like a lot, it is not so bad since Anchorstone Holdings has a market capitalization of HK$108.6m, and so it could probably strengthen its balance sheet by raising capital if it needed to. But it's clear that we should definitely closely examine whether it can manage its debt without dilution. The balance sheet is clearly the area to focus on when you are analysing debt. But it is Anchorstone Holdings's earnings that will influence how the balance sheet holds up in the future. So when considering debt, it's definitely worth looking at the earnings trend. Click here for an interactive snapshot.

In the last year Anchorstone Holdings had a loss before interest and tax, and actually shrunk its revenue by 34%, to HK$68m. That makes us nervous, to say the least.

Caveat Emptor

Not only did Anchorstone Holdings's revenue slip over the last twelve months, but it also produced negative earnings before interest and tax (EBIT). Its EBIT loss was a whopping HK$38m. When we look at that and recall the liabilities on its balance sheet, relative to cash, it seems unwise to us for the company to have any debt. So we think its balance sheet is a little strained, though not beyond repair. We would feel better if it turned its trailing twelve month loss of HK$45m into a profit. So in short it's a really risky stock. There's no doubt that we learn most about debt from the balance sheet. But ultimately, every company can contain risks that exist outside of the balance sheet. We've identified 5 warning signs with Anchorstone Holdings (at least 1 which is significant) , and understanding them should be part of your investment process.

Of course, if you're the type of investor who prefers buying stocks without the burden of debt, then don't hesitate to discover our exclusive list of net cash growth stocks, today.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SEHK:1592

Anchorstone Holdings

An investment holding company, engages in the supply and installation of marble and granite products for construction projects in Hong Kong, Macau, and the People’s Republic of China.

Adequate balance sheet low.

Market Insights

Community Narratives