CK Hutchison Holdings (SEHK:1) recently closed at HK$51.55, showing a slight increase over the past month. Investors are keeping an eye on the stock’s performance, as it has edged up nearly 2% in that time.

After a strong run this year, CK Hutchison Holdings has racked up a 25.6% year-to-date share price return, with the one-year total shareholder return reaching an impressive 28.8%. Recent gains suggest that investor momentum is building, which may reflect renewed optimism around long-term value and growth prospects.

Still, the big question remains: given the strong returns and current valuation, is CK Hutchison Holdings trading below its true worth, or are future growth prospects already built into the price?

Advertisement

Most Popular Narrative: 15.6% Undervalued

CK Hutchison Holdings' widely followed narrative suggests a fair value 15.6% above the recent closing price of HK$51.55. The current market appears to be discounting more than the dominant storyline projects for the company's future earning power.

The successful merger of 3 UK and Vodafone UK, along with the broader ongoing review across European telecom operations, is expected to drive substantial operating and capital expense synergies (targeting GBP 700 million a year at run-rate within five years). This is anticipated to enhance recurring net margins and group earnings. Sustained investment and efficiency-driven growth in the Ports division, including expanded facilities in key geographies and increased storage income, position the company to benefit from global trade resilience and supply chain optimization. This aims to support higher revenue and stable cash flows.

Curious about the financial assumptions that fuel this narrative’s upbeat outlook? There is a bold growth target hiding behind those merger synergies and global expansion bets. Want to know if projected profit margins really leap as high as some expect? See what shapes this valuation and where expectations might surprise you.

However, ongoing reliance on one-time gains and persistent weakness in the Chinese retail segment could create challenges for the sustainability of current earnings momentum.

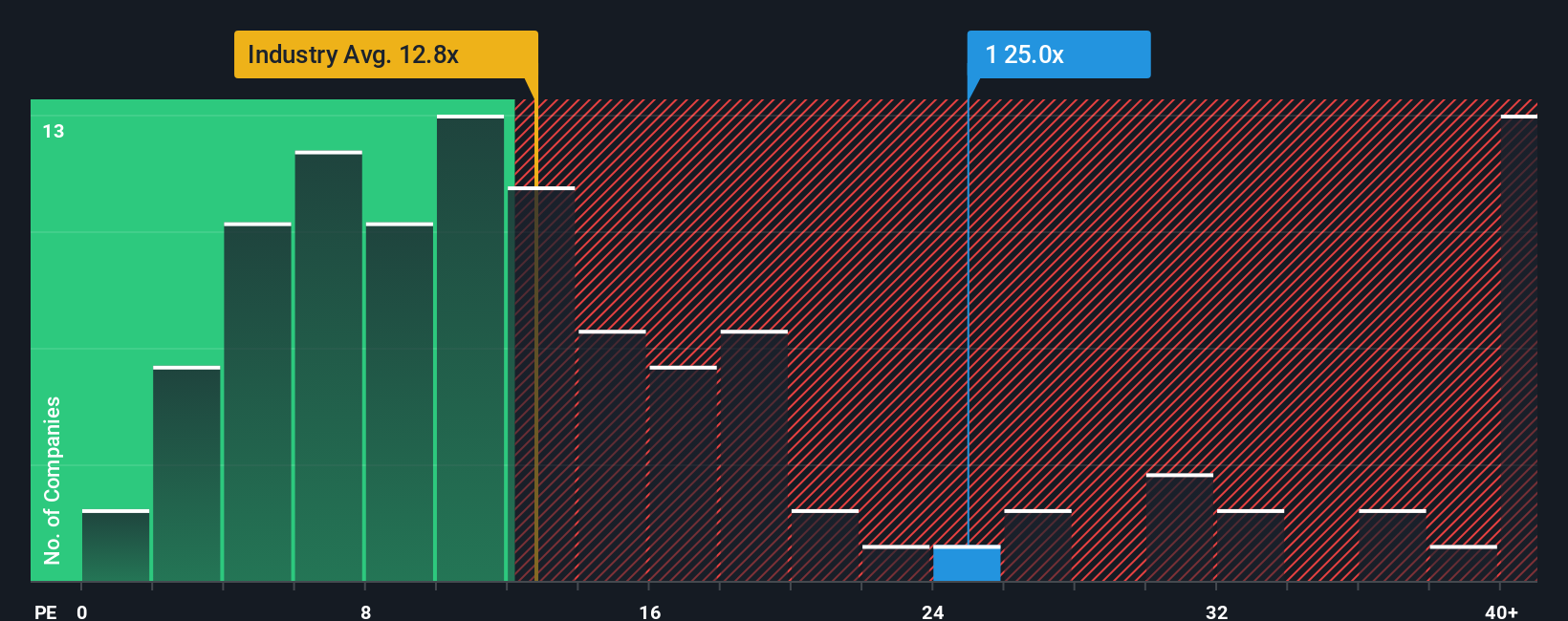

Another View: Market Ratios Paint a Different Picture

While analysts see CK Hutchison Holdings as undervalued, its price-to-earnings ratio of 25.5x is actually higher than both the Asian Industrials industry average (12.8x) and its fair ratio of 17.5x. This suggests the stock trades at a premium, which could indicate that valuation risk exists even if growth prospects seem strong. Is the market already pricing in too much optimism?

If you think the numbers tell a different story, or want to dig into the details on your own terms, you can easily put together your own narrative in just a few minutes. Do it your way

A great starting point for your CK Hutchison Holdings research is our analysis highlighting 2 key rewards and 3 important warning signs that could impact your investment decision.

Looking for more investment ideas?

Your next big win might be just a click away. Take action and check these out before the best opportunities slip through your fingers.

Access tomorrow’s top disruptors now with these 24 AI penny stocks, powering advancements in artificial intelligence and shaping how industries evolve.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield) • Undervalued Small Caps with Insider Buying • High growth Tech and AI Companies

An investment holding company, primarily operates in ports and related services, retail, infrastructure, and telecommunications businesses in Hong Kong, Mainland China, Europe, Canada, Asia, Australia, and internationally.