Undiscovered Gems in Hong Kong Promising Stocks for October 2024

Reviewed by Simply Wall St

As geopolitical tensions in the Middle East have influenced global markets, Hong Kong's Hang Seng Index has shown resilience, climbing 10.2% amid optimism about China's supportive economic measures. This environment presents a unique opportunity for investors to explore lesser-known stocks that may benefit from current market dynamics and economic policies. Identifying promising stocks often involves looking at companies with strong fundamentals and growth potential, especially in sectors poised to thrive under these conditions.

Top 10 Undiscovered Gems With Strong Fundamentals In Hong Kong

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| PW Medtech Group | 0.06% | 22.33% | -17.56% | ★★★★★★ |

| C&D Property Management Group | 1.32% | 37.15% | 41.55% | ★★★★★★ |

| Uju Holding | 21.23% | -4.96% | -15.33% | ★★★★★★ |

| COSCO SHIPPING International (Hong Kong) | NA | -3.84% | 16.33% | ★★★★★★ |

| Tianyun International Holdings | 10.09% | -5.59% | -9.92% | ★★★★★★ |

| S.A.S. Dragon Holdings | 60.96% | 4.62% | 10.02% | ★★★★★☆ |

| Carote | 2.36% | 85.09% | 92.12% | ★★★★★☆ |

| Lee's Pharmaceutical Holdings | 14.22% | -1.39% | -14.93% | ★★★★★☆ |

| Billion Industrial Holdings | 3.63% | 18.00% | -11.38% | ★★★★★☆ |

| Pizu Group Holdings | 48.34% | -4.53% | -19.78% | ★★★★☆☆ |

Below we spotlight a couple of our favorites from our exclusive screener.

Bank of Gansu (SEHK:2139)

Simply Wall St Value Rating: ★★★★★★

Overview: Bank of Gansu Co., Ltd., along with its subsidiary Pingliang Jingning Chengji Rural Bank Co., Ltd., offers a range of banking services in the People’s Republic of China and has a market capitalization of approximately HK$5.58 billion.

Operations: Bank of Gansu generates revenue primarily from retail banking (CN¥2.10 billion) and corporate banking (CN¥1.21 billion), while its financial market operations show a negative contribution (CN¥-368.60 million).

With total assets of CN¥422.2 billion, Bank of Gansu stands out due to its solid asset base and a sufficient allowance for bad loans at 135%. This bank's price-to-earnings ratio is 8.1x, which is below the Hong Kong market average of 10.6x, hinting at potential value. Despite earnings decreasing by an average of 6.4% annually over five years, the bank maintains high-quality past earnings and primarily low-risk funding sources comprising 86% customer deposits.

- Dive into the specifics of Bank of Gansu here with our thorough health report.

Understand Bank of Gansu's track record by examining our Past report.

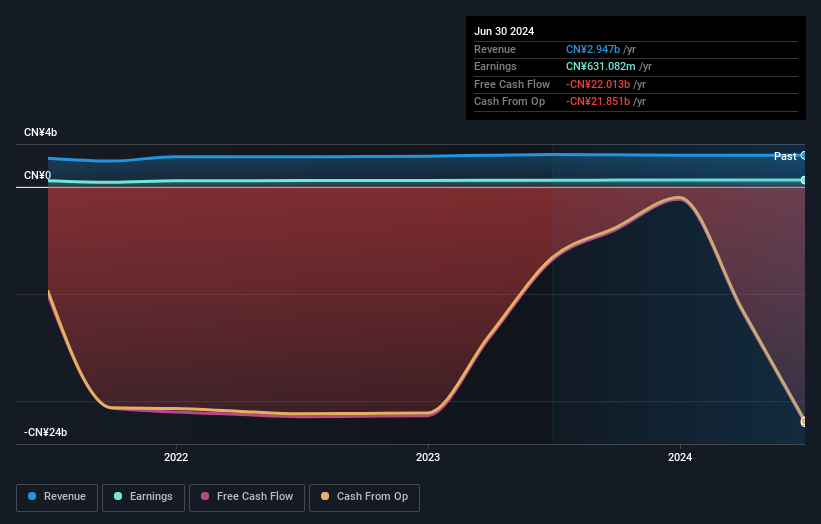

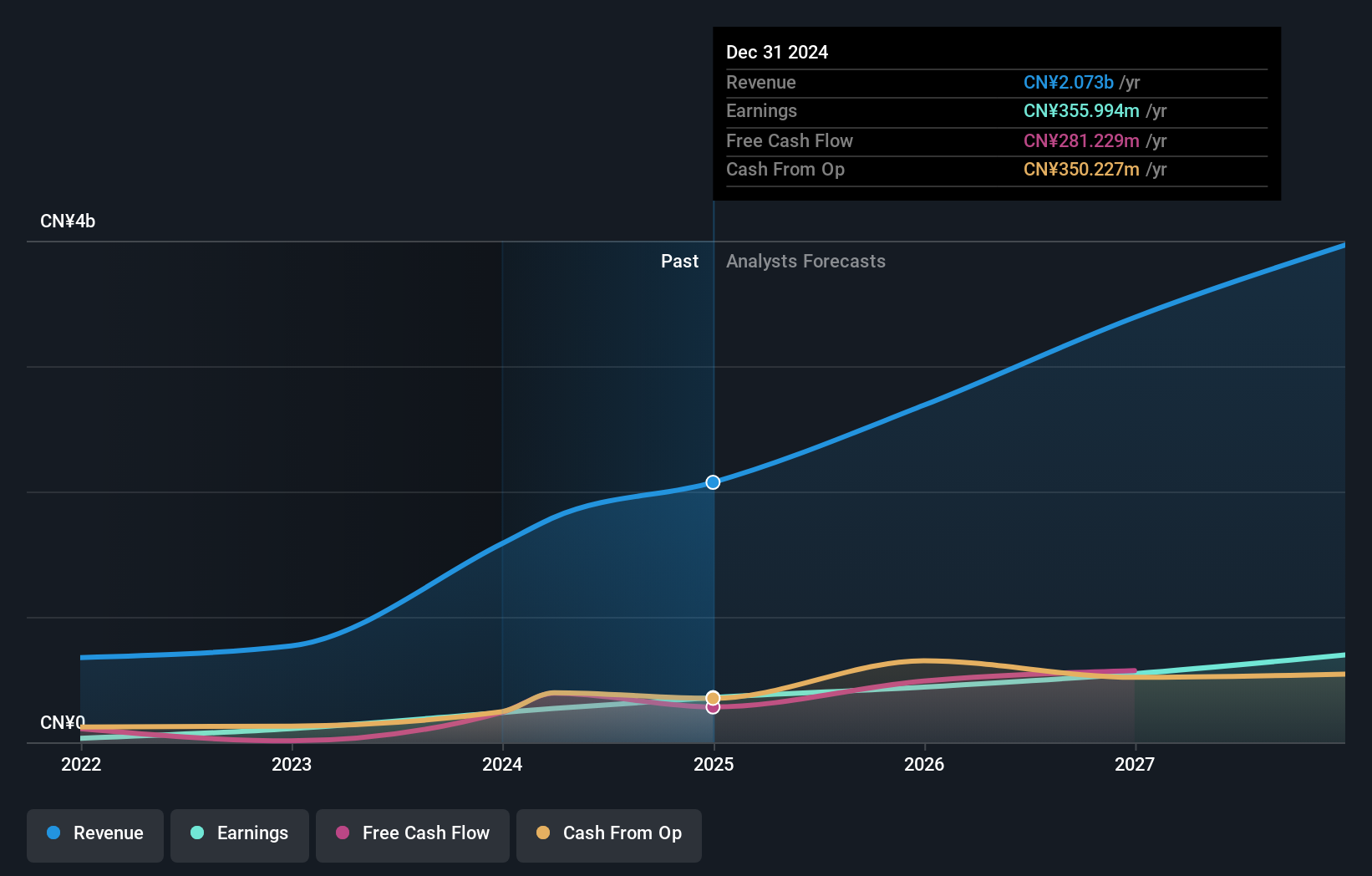

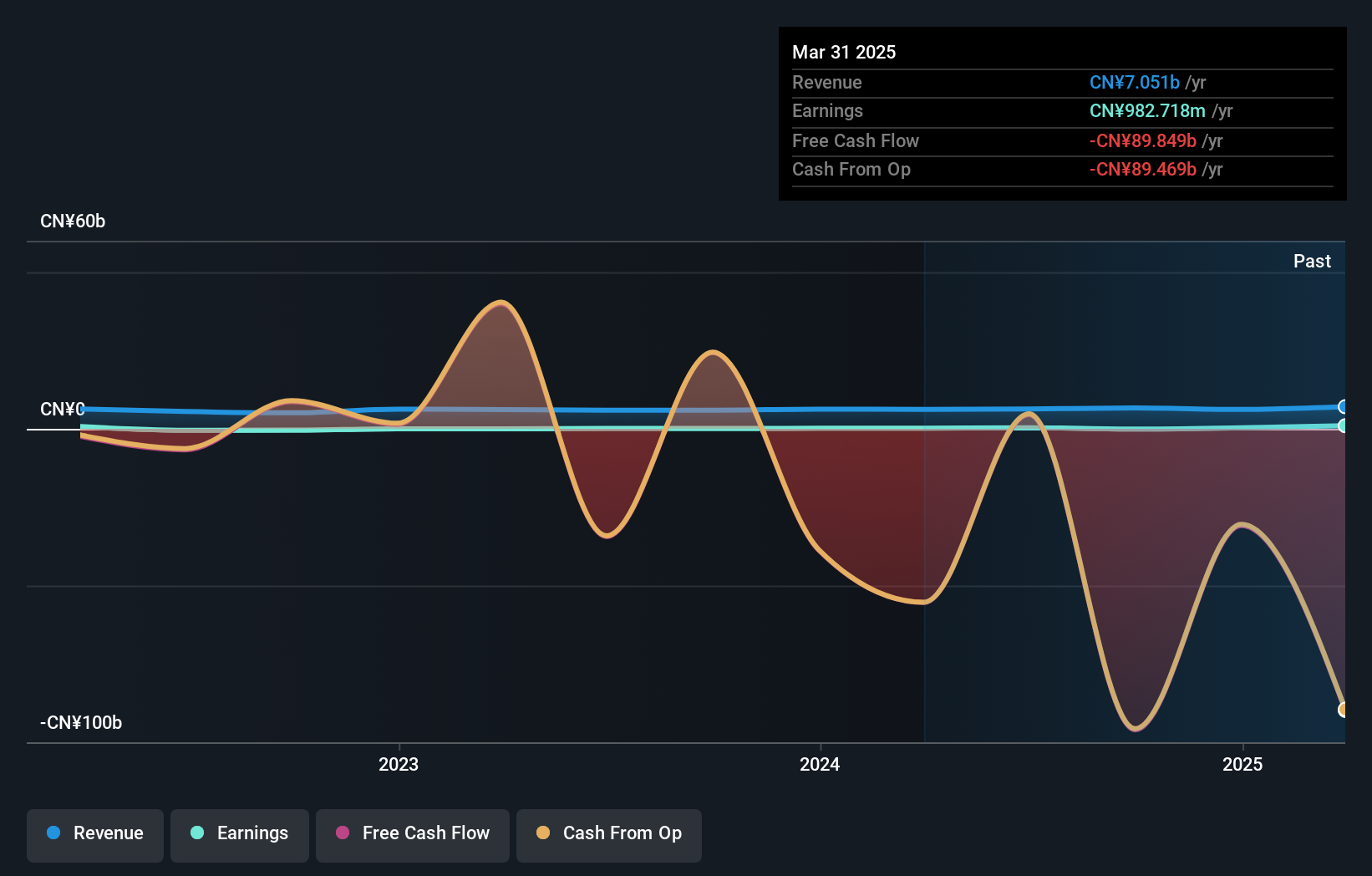

Carote (SEHK:2549)

Simply Wall St Value Rating: ★★★★★☆

Overview: Carote Ltd is an investment holding company that offers kitchenware products to brand-owners and retailers under the CAROTE brand, with a market capitalization of approximately HK$4.49 billion.

Operations: Carote Ltd generates revenue primarily through its Branded Business, contributing CN¥1.58 billion, and a smaller portion from its ODM Business at CN¥210.80 million.

Carote has recently caught attention with its IPO, raising HK$750.62 million by offering ordinary shares at HK$5.78 each, slightly discounted by HK$0.14 per share. This move comes on the heels of a standout financial year where earnings surged 92%, outpacing the Consumer Durables industry growth of 20%. Trading significantly below estimated fair value, Carote's high-quality earnings and sufficient cash position relative to debt paint a promising picture despite its illiquid shares.

- Get an in-depth perspective on Carote's performance by reading our health report here.

Explore historical data to track Carote's performance over time in our Past section.

Harbin Bank (SEHK:6138)

Simply Wall St Value Rating: ★★★★★☆

Overview: Harbin Bank Co., Ltd. provides various banking products and services primarily in China with a market capitalization of HK$5.33 billion.

Operations: The bank generates revenue from four main segments: Retail Financial Business (CN¥2.99 billion), Corporate Financial Business (CN¥1.02 billion), Interbank Financial Business (CN¥1.14 billion), and Other Business (CN¥1.19 billion).

Harbin Bank, with total assets of CN¥882.8 billion and equity of CN¥65 billion, is making waves in the financial sector. The bank's earnings skyrocketed by 202% over the past year, outpacing the industry average significantly. It boasts a sufficient allowance for bad loans at 203%, showcasing prudent risk management despite a high non-performing loan ratio of 2.7%. With customer deposits forming 86% of its liabilities, Harbin Bank enjoys low-risk funding stability.

- Delve into the full analysis health report here for a deeper understanding of Harbin Bank.

Evaluate Harbin Bank's historical performance by accessing our past performance report.

Summing It All Up

- Navigate through the entire inventory of 171 SEHK Undiscovered Gems With Strong Fundamentals here.

- Already own these companies? Link your portfolio to Simply Wall St and get alerts on any new warning signs to your stocks.

- Discover a world of investment opportunities with Simply Wall St's free app and access unparalleled stock analysis across all markets.

Interested In Other Possibilities?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Bank of Gansu might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SEHK:2139

Bank of Gansu

Together with its subsidiary, Pingliang Jingning Chengji Rural Bank Co., Ltd., provides various banking services in the People’s Republic of China.

Flawless balance sheet with proven track record.