Advertisement

- Greece

- /

- Electronic Equipment and Components

- /

- ATSE:INTEK

Robust Earnings May Not Tell The Whole Story For Ideal Group (ATH:INTEK)

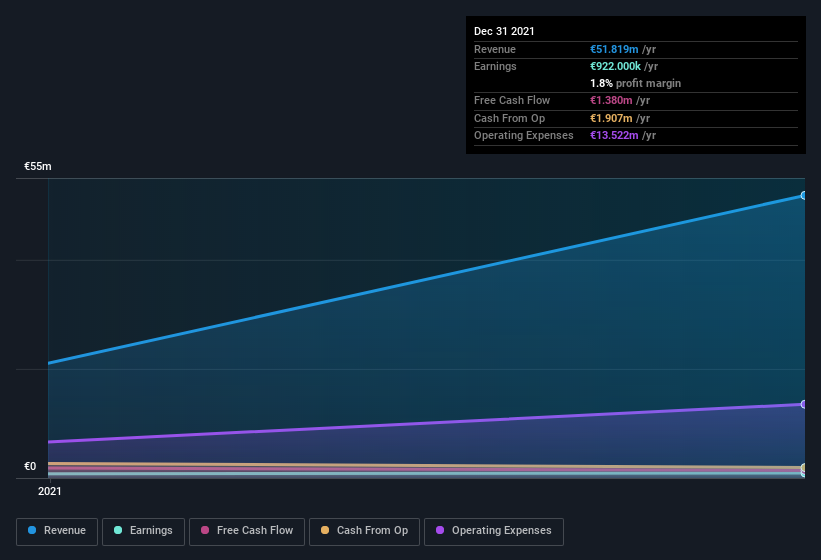

Ideal Group S.A.'s (ATH:INTEK) healthy profit numbers didn't contain any surprises for investors. However the statutory profit number doesn't tell the whole story, and we have found some factors which might be of concern to shareholders.

See our latest analysis for Ideal Group

One essential aspect of assessing earnings quality is to look at how much a company is diluting shareholders. As it happens, Ideal Group issued 279% more new shares over the last year. As a result, its net income is now split between a greater number of shares. Per share metrics like EPS help us understand how much actual shareholders are benefitting from the company's profits, while the net income level gives us a better view of the company's absolute size. You can see a chart of Ideal Group's EPS by clicking here.

How Is Dilution Impacting Ideal Group's Earnings Per Share? (EPS)

As it happens, we don't know how much the company made or lost three years ago, because we don't have the data. The good news is that profit was up 16% in the last twelve months. But EPS was far less impressive, dropping 54% in that time. This shows how dangerous it is to rely on net income alone, when measuring growth. So you can see that the dilution has had a fairly significant impact on shareholders.

In the long term, if Ideal Group's earnings per share can increase, then the share price should too. But on the other hand, we'd be far less excited to learn profit (but not EPS) was improving. For the ordinary retail shareholder, EPS is a great measure to check your hypothetical "share" of the company's profit.

Note: we always recommend investors check balance sheet strength. Click here to be taken to our balance sheet analysis of Ideal Group.

Our Take On Ideal Group's Profit Performance

Ideal Group shareholders should keep in mind how many new shares it is issuing, because, dilution clearly has the power to severely impact shareholder returns. For this reason, we think that Ideal Group's statutory profits may be a bad guide to its underlying earnings power, and might give investors an overly positive impression of the company. In further bad news, its earnings per share decreased in the last year. Of course, we've only just scratched the surface when it comes to analysing its earnings; one could also consider margins, forecast growth, and return on investment, among other factors. So while earnings quality is important, it's equally important to consider the risks facing Ideal Group at this point in time. When we did our research, we found 3 warning signs for Ideal Group (1 is concerning!) that we believe deserve your full attention.

Today we've zoomed in on a single data point to better understand the nature of Ideal Group's profit. But there is always more to discover if you are capable of focussing your mind on minutiae. For example, many people consider a high return on equity as an indication of favorable business economics, while others like to 'follow the money' and search out stocks that insiders are buying. While it might take a little research on your behalf, you may find this free collection of companies boasting high return on equity, or this list of stocks that insiders are buying to be useful.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About ATSE:INTEK

Ideal Holdings

Provides trust and cybersecurity solutions and services in Greece and internationally.

Reasonable growth potential with questionable track record.

Market Insights

Advertisement

Community Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|11.0% undervalued

BE

Community Contributor

Procter & Gamble: A Dividend Giant Facing Slowing Growth

Fair Value US$119.81|23.3% overvalued

AN

Community Contributor

Eli Lilly's Future Growth Driven by Tirzepatide and Favorable Market Conditions

Fair Value US$1.19k|13.8% undervalued

EA

Community Contributor