Advertisement

- United Kingdom

- /

- Insurance

- /

- AIM:HUW

Big Technologies And 2 Other UK Penny Stocks To Monitor

Simply Wall St

Reviewed by Simply Wall St

The UK stock market has recently faced challenges, with the FTSE 100 and FTSE 250 indices experiencing declines due to weak trade data from China, impacting sectors closely tied to global economic performance. Amidst these broader market fluctuations, investors may find opportunities in smaller or newer companies often referred to as penny stocks. Although the term might seem outdated, these stocks can offer a blend of affordability and growth potential when they possess strong financials and resilient business models.

Top 10 Penny Stocks In The United Kingdom

| Name | Share Price | Market Cap | Financial Health Rating |

| ME Group International (LSE:MEGP) | £2.085 | £785.55M | ★★★★★★ |

| Begbies Traynor Group (AIM:BEG) | £0.924 | £145.75M | ★★★★★★ |

| Secure Trust Bank (LSE:STB) | £3.39 | £64.65M | ★★★★☆☆ |

| Ultimate Products (LSE:ULTP) | £1.165 | £99.53M | ★★★★★★ |

| Luceco (LSE:LUCE) | £1.28 | £197.41M | ★★★★★☆ |

| Stelrad Group (LSE:SRAD) | £1.38 | £175.75M | ★★★★★☆ |

| Next 15 Group (AIM:NFG) | £3.86 | £383.9M | ★★★★☆☆ |

| Integrated Diagnostics Holdings (LSE:IDHC) | $0.45 | $261.6M | ★★★★★★ |

| Tristel (AIM:TSTL) | £3.90 | £186M | ★★★★★★ |

| Impax Asset Management Group (AIM:IPX) | £2.41 | £307.94M | ★★★★★★ |

Click here to see the full list of 472 stocks from our UK Penny Stocks screener.

Let's take a closer look at a couple of our picks from the screened companies.

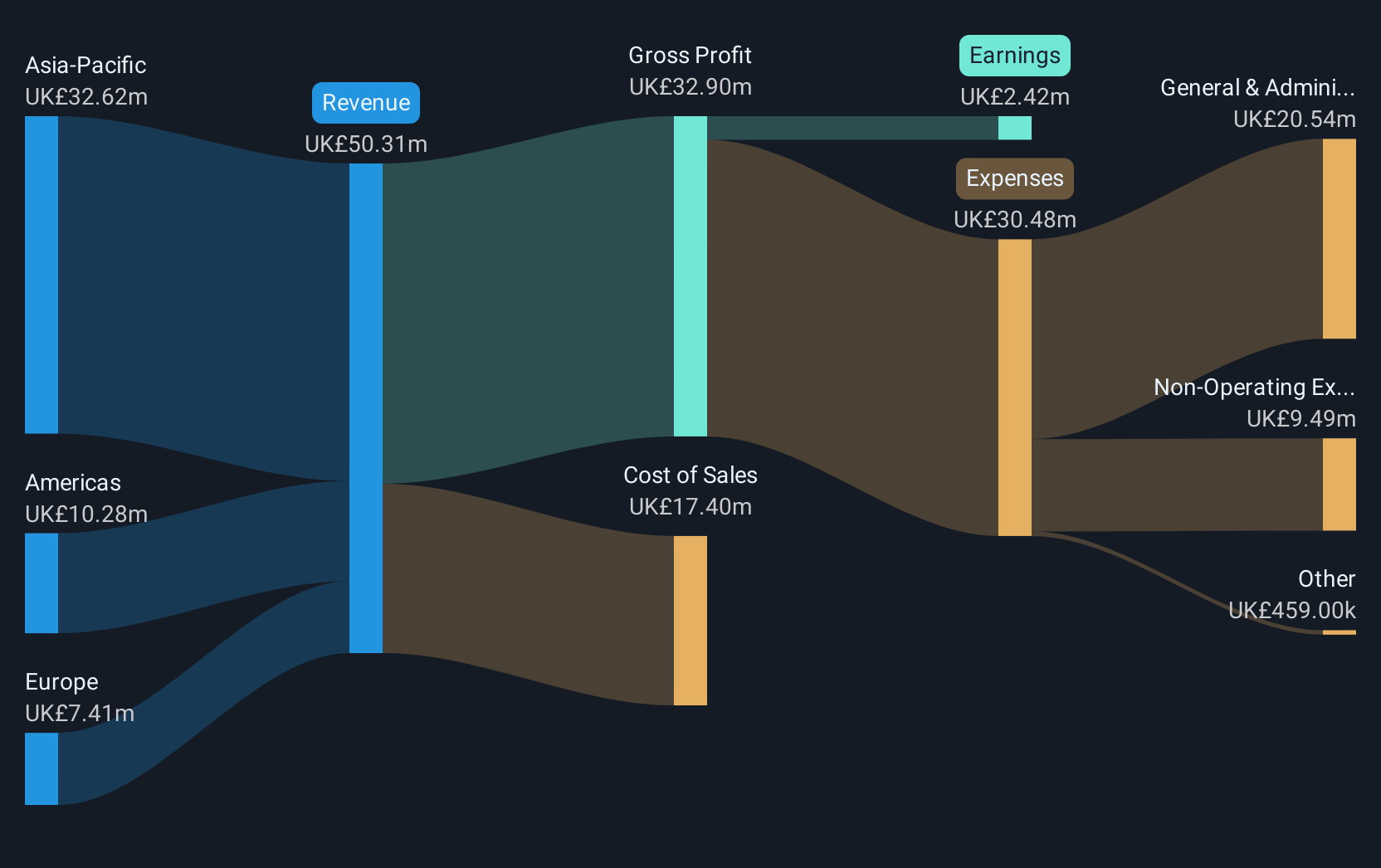

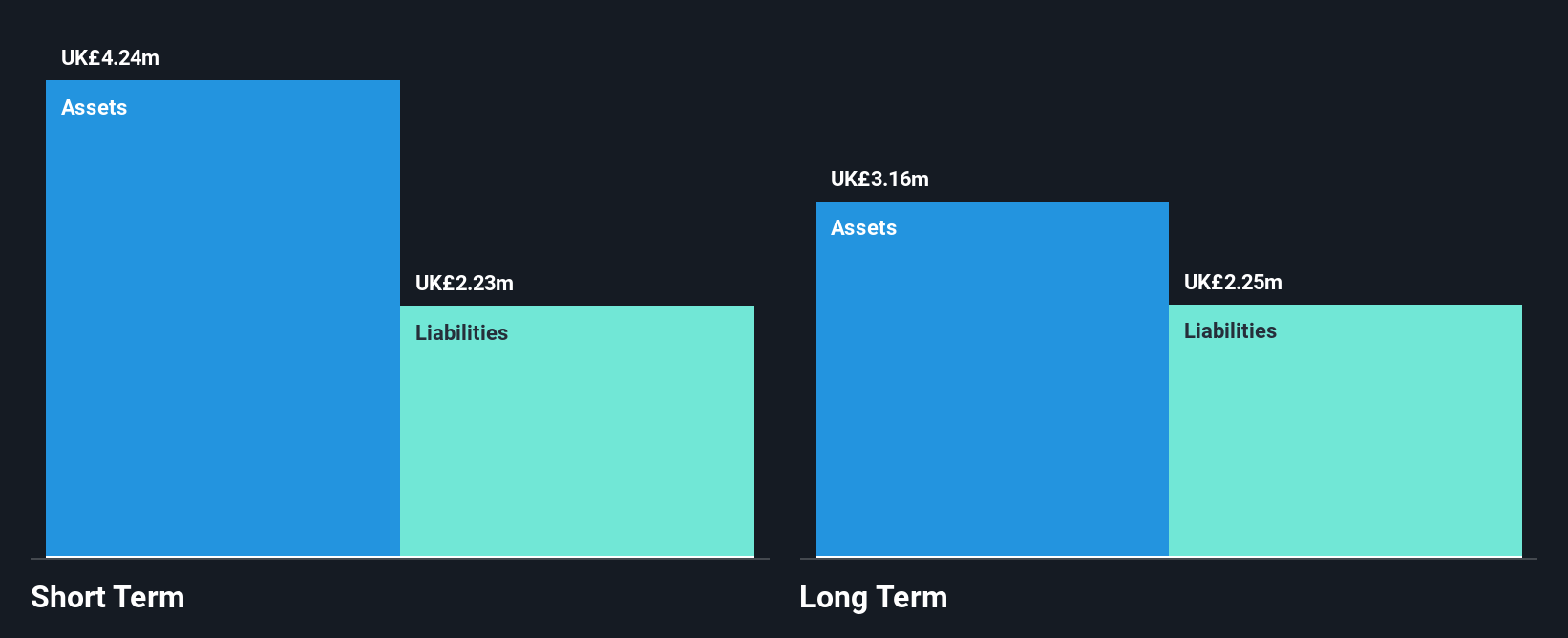

Big Technologies (AIM:BIG)

Simply Wall St Financial Health Rating: ★★★★★★

Overview: Big Technologies PLC, operating under the Buddi brand, develops and delivers remote monitoring technologies and services for the offender and personal monitoring industry across the Americas, Europe, and Asia-Pacific, with a market cap of £409.03 million.

Operations: The company generates revenue of £54.45 million from its electronic tracking devices, products, and services segment.

Market Cap: £409.03M

Big Technologies PLC, with a market cap of £409.03 million, has shown mixed financial performance recently. Despite having high-quality earnings and no debt, the company faced negative earnings growth of -36.9% over the past year and declining profit margins from 36.4% to 23%. Short-term assets significantly exceed liabilities, indicating strong liquidity. Recent insider selling may raise concerns for investors, though a share buyback program could signal management's confidence in the company's value. Earnings are forecasted to grow at 26.9% annually, suggesting potential future improvement despite recent setbacks in profitability and sales figures.

- Dive into the specifics of Big Technologies here with our thorough balance sheet health report.

- Examine Big Technologies' earnings growth report to understand how analysts expect it to perform.

Finseta (AIM:FIN)

Simply Wall St Financial Health Rating: ★★★★★☆

Overview: Finseta Plc is a foreign exchange and payment company that provides multi-currency accounts to businesses and individuals, with a market cap of £19.52 million.

Operations: The company's revenue is derived from its Data Processing segment, which generated £11.11 million.

Market Cap: £19.52M

Finseta Plc, with a market cap of £19.52 million, has demonstrated financial stability by covering both short and long-term liabilities with its assets (£3.8M). The company recently turned profitable, achieving an impressive Return on Equity of 112.1%. Its debt is well-managed, with operating cash flow covering 120.7% of it, and the firm holds more cash than total debt. Despite high non-cash earnings and a relatively low Price-To-Earnings ratio (7.7x), the board's inexperience could be a concern for some investors as they navigate this penny stock's potential growth trajectory in the foreign exchange sector.

- Unlock comprehensive insights into our analysis of Finseta stock in this financial health report.

- Assess Finseta's future earnings estimates with our detailed growth reports.

Helios Underwriting (AIM:HUW)

Simply Wall St Financial Health Rating: ★★★★★☆

Overview: Helios Underwriting plc, along with its subsidiaries, offers limited liability investment opportunities in the Lloyd's insurance market in the UK and has a market cap of £169.80 million.

Operations: The company's revenue is primarily generated from Syndicate Participation (£258.32 million) and Investment Management (£4.62 million).

Market Cap: £169.8M

Helios Underwriting plc, with a market cap of £169.80 million, has shown robust earnings growth, reporting revenue of £132.64 million for the half year ended June 2024, up from £93.65 million the previous year. Despite a low Return on Equity (12.6%), its financial health is supported by short-term assets (£900M) exceeding liabilities and well-covered interest payments (14.4x EBIT). The company's Price-To-Earnings ratio (9.6x) suggests potential value compared to the UK market average of 16x. However, investors should note the management's inexperience and an unstable dividend history as potential risks in this penny stock investment.

- Take a closer look at Helios Underwriting's potential here in our financial health report.

- Gain insights into Helios Underwriting's outlook and expected performance with our report on the company's earnings estimates.

Next Steps

- Access the full spectrum of 472 UK Penny Stocks by clicking on this link.

- Hold shares in these firms? Setup your portfolio in Simply Wall St to seamlessly track your investments and receive personalized updates on your portfolio's performance.

- Unlock the power of informed investing with Simply Wall St, your free guide to navigating stock markets worldwide.

Ready For A Different Approach?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Jump on the AI train with fast growing tech companies forging a new era of innovation.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Helios Underwriting might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About AIM:HUW

Helios Underwriting

Provides a limited liability investment for its shareholders in the Lloyd’s insurance market in the United Kingdom.

Reasonable growth potential with proven track record.

Similar Companies

Market Insights

Advertisement

Community Narratives

The Future of Drug Testing? Fingerprint Tech Shows Serious Promise

Fair Value US$2.98|33.6% undervalued

JO

Community Contributor

Occidental Petroleum is set to achieve a 16% profit margin improvement

Fair Value US$55.05|18.5% undervalued

DZ

Community Contributor

Argan's Revenue Set to Soar with a 13.31% Growth in the Coming Decade

Fair Value US$284.68|21.2% undervalued

KE

Community Contributor

EU#1 - From German Startup to EU’s Biggest Company

Fair Value €248.62|5.8% overvalued

TO

Community Contributor