- United Kingdom

- /

- Software

- /

- AIM:RDT

Shareholders May Find It Hard To Justify Increasing Rosslyn Data Technologies plc's (LON:RDT) CEO Compensation For Now

Key Insights

- Rosslyn Data Technologies' Annual General Meeting to take place on 3rd of December

- CEO Paul Watts' total compensation includes salary of UK£220.0k

- The total compensation is similar to the average for the industry

- Over the past three years, Rosslyn Data Technologies' EPS grew by 20% and over the past three years, the total loss to shareholders 98%

The underwhelming share price performance of Rosslyn Data Technologies plc (LON:RDT) in the past three years would have disappointed many shareholders. However, what is unusual is that EPS growth has been positive, suggesting that the share price has diverged from fundamentals. These are some of the concerns that shareholders may want to bring up at the next AGM held on 3rd of December. They could also influence management through voting on resolutions such as executive remuneration. We discuss below why we think shareholders should be cautious of approving a raise for the CEO at the moment.

Check out our latest analysis for Rosslyn Data Technologies

Comparing Rosslyn Data Technologies plc's CEO Compensation With The Industry

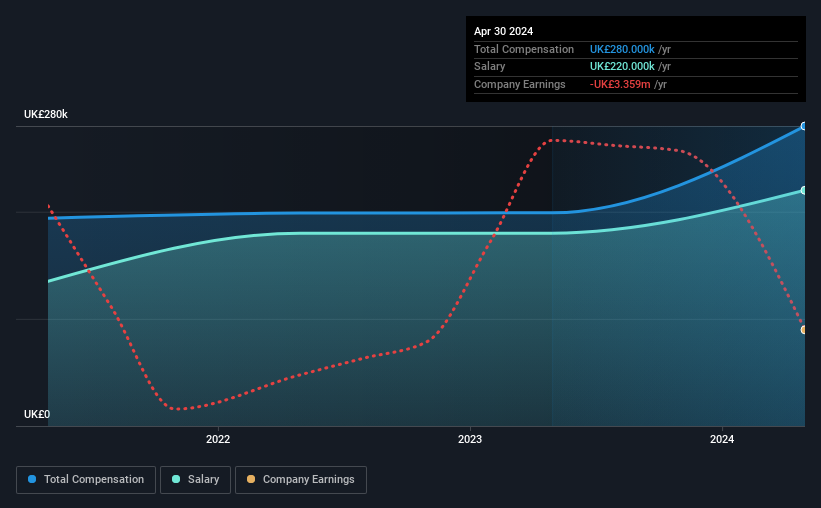

At the time of writing, our data shows that Rosslyn Data Technologies plc has a market capitalization of UK£3.3m, and reported total annual CEO compensation of UK£280k for the year to April 2024. Notably, that's an increase of 41% over the year before. In particular, the salary of UK£220.0k, makes up a huge portion of the total compensation being paid to the CEO.

On comparing similar-sized companies in the British Software industry with market capitalizations below UK£159m, we found that the median total CEO compensation was UK£280k. So it looks like Rosslyn Data Technologies compensates Paul Watts in line with the median for the industry.

| Component | 2024 | 2023 | Proportion (2024) |

| Salary | UK£220k | UK£180k | 79% |

| Other | UK£60k | UK£19k | 21% |

| Total Compensation | UK£280k | UK£199k | 100% |

On an industry level, around 65% of total compensation represents salary and 35% is other remuneration. According to our research, Rosslyn Data Technologies has allocated a higher percentage of pay to salary in comparison to the wider industry. If salary is the major component in total compensation, it suggests that the CEO receives a higher fixed proportion of the total compensation, regardless of performance.

Rosslyn Data Technologies plc's Growth

Rosslyn Data Technologies plc's earnings per share (EPS) grew 20% per year over the last three years. In the last year, its revenue is down 5.2%.

Shareholders would be glad to know that the company has improved itself over the last few years. While it would be good to see revenue growth, profits matter more in the end. Historical performance can sometimes be a good indicator on what's coming up next but if you want to peer into the company's future you might be interested in this free visualization of analyst forecasts.

Has Rosslyn Data Technologies plc Been A Good Investment?

Few Rosslyn Data Technologies plc shareholders would feel satisfied with the return of -98% over three years. Therefore, it might be upsetting for shareholders if the CEO were paid generously.

To Conclude...

Shareholders have not seen their shares grow in value, rather they have seen their shares decline. The fact that the stock price hasn't grown along with earnings may indicate that other issues may be affecting that stock. If there are some unknown variables that are influencing the stock's price, surely shareholders would have some concerns. The upcoming AGM will be a chance for shareholders to question the board on key matters, such as CEO remuneration or any other issues they might have and revisit their investment thesis with regards to the company.

CEO pay is simply one of the many factors that need to be considered while examining business performance. We did our research and identified 5 warning signs (and 3 which are a bit concerning) in Rosslyn Data Technologies we think you should know about.

Switching gears from Rosslyn Data Technologies, if you're hunting for a pristine balance sheet and premium returns, this free list of high return, low debt companies is a great place to look.

The New Payments ETF Is Live on NASDAQ:

Money is moving to real-time rails, and a newly listed ETF now gives investors direct exposure. Fast settlement. Institutional custody. Simple access.

Explore how this launch could reshape portfolios

Sponsored ContentNew: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About AIM:RDT

Rosslyn Data Technologies

Provides data analytics solutions in the United Kingdom, Europe, and North America.

Excellent balance sheet with moderate risk.

Similar Companies

Market Insights

Weekly Picks

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Recently Updated Narratives

Q3 Outlook modestly optimistic

Title: Market Sentiment Is Dead Wrong — Here's Why PSEC Deserves a Second Look

An amazing opportunity to potentially get a 100 bagger

Popular Narratives

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

MicroVision will explode future revenue by 380.37% with a vision towards success

Trending Discussion