Advertisement

- United Kingdom

- /

- Professional Services

- /

- AIM:LTG

This Is The Reason Why We Think Learning Technologies Group plc's (LON:LTG) CEO Might Be Underpaid

The solid performance at Learning Technologies Group plc (LON:LTG) has been impressive and shareholders will probably be pleased to know that CEO Jonathan Satchell has delivered. At the upcoming AGM on 26 May 2021, they would be interested to hear about the company strategy going forward and get a chance to cast their votes on resolutions such as executive remuneration and other company matters. Here we will show why we think CEO compensation is appropriate and discuss the case for a pay rise.

See our latest analysis for Learning Technologies Group

Comparing Learning Technologies Group plc's CEO Compensation With the industry

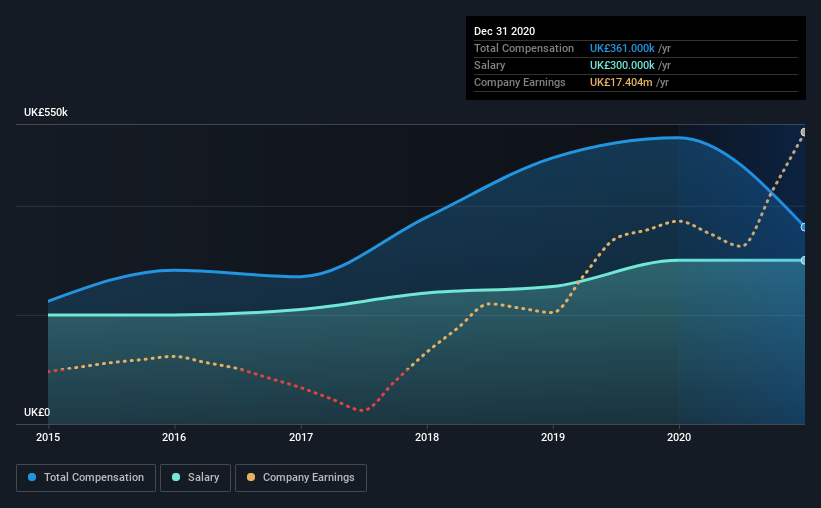

Our data indicates that Learning Technologies Group plc has a market capitalization of UK£1.3b, and total annual CEO compensation was reported as UK£361k for the year to December 2020. That's a notable decrease of 31% on last year. In particular, the salary of UK£300.0k, makes up a huge portion of the total compensation being paid to the CEO.

For comparison, other companies in the same industry with market capitalizations ranging between UK£706m and UK£2.3b had a median total CEO compensation of UK£1.2m. In other words, Learning Technologies Group pays its CEO lower than the industry median. What's more, Jonathan Satchell holds UK£128m worth of shares in the company in their own name, indicating that they have a lot of skin in the game.

| Component | 2020 | 2019 | Proportion (2020) |

| Salary | UK£300k | UK£300k | 83% |

| Other | UK£61k | UK£225k | 17% |

| Total Compensation | UK£361k | UK£525k | 100% |

Speaking on an industry level, nearly 70% of total compensation represents salary, while the remainder of 30% is other remuneration. Learning Technologies Group is paying a higher share of its remuneration through a salary in comparison to the overall industry. If salary dominates total compensation, it suggests that CEO compensation is leaning less towards the variable component, which is usually linked with performance.

A Look at Learning Technologies Group plc's Growth Numbers

Learning Technologies Group plc's earnings per share (EPS) grew 118% per year over the last three years. Its revenue is up 1.7% over the last year.

Overall this is a positive result for shareholders, showing that the company has improved in recent years. It's also good to see modest revenue growth, suggesting the underlying business is healthy. Looking ahead, you might want to check this free visual report on analyst forecasts for the company's future earnings..

Has Learning Technologies Group plc Been A Good Investment?

Most shareholders would probably be pleased with Learning Technologies Group plc for providing a total return of 67% over three years. As a result, some may believe the CEO should be paid more than is normal for companies of similar size.

To Conclude...

Seeing that the company has put in a relatively good performance, the CEO remuneration policy may not be the focus at the AGM. However, investors will get the chance to engage on key strategic initiatives and future growth opportunities for the company and set their longer-term expectations.

While it is important to pay attention to CEO remuneration, investors should also consider other elements of the business. That's why we did some digging and identified 1 warning sign for Learning Technologies Group that you should be aware of before investing.

Arguably, business quality is much more important than CEO compensation levels. So check out this free list of interesting companies that have HIGH return on equity and low debt.

If you decide to trade Learning Technologies Group, use the lowest-cost* platform that is rated #1 Overall by Barron’s, Interactive Brokers. Trade stocks, options, futures, forex, bonds and funds on 135 markets, all from a single integrated account. Promoted

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About AIM:LTG

Learning Technologies Group

Provides talent and learning solutions, content, services, and digital platforms to corporate and government clients.

Solid track record with excellent balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroStrategy: Volatile Gamble or Golden Opportunity?

Fair Value US$663.00|36.2% undervalued

BL

Community Contributor

Emerging Markets and Debt Reduction Will Propel Bath & Body Works Forward

Fair Value US$40.73|22.0% undervalued

ZW

Community Contributor

An amazing opportunity to potentially get a 100 bagger

Fair Value US$10.00|46.4% overvalued

DA

Community Contributor