- United Kingdom

- /

- IT

- /

- AIM:ING

It Looks Like Shareholders Would Probably Approve Ingenta plc's (LON:ING) CEO Compensation Package

We have been pretty impressed with the performance at Ingenta plc (LON:ING) recently and CEO Gregory Winner deserves a mention for their role in it. Shareholders will have this at the front of their minds in the upcoming AGM on 11 November 2022. This would also be a chance for them to hear the board review the financial results, discuss future company strategy and vote on any resolutions such as executive remuneration. We think the CEO has done a pretty decent job and we discuss why the CEO compensation is appropriate.

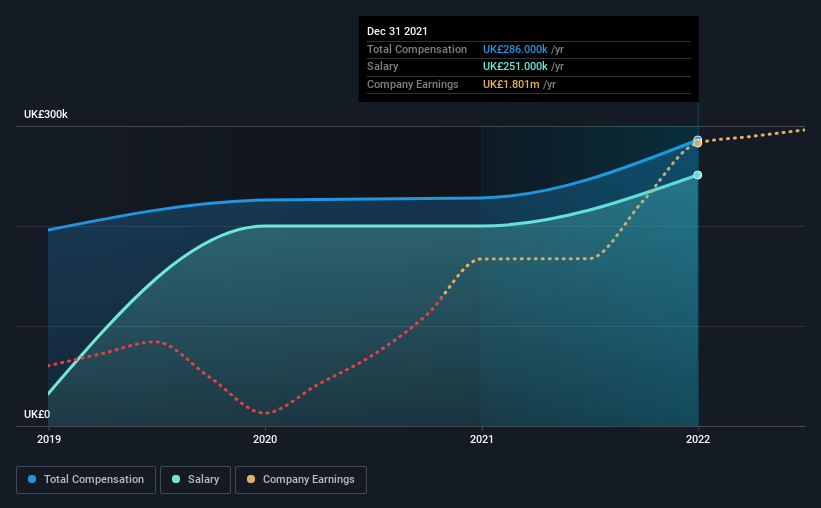

See our latest analysis for Ingenta

How Does Total Compensation For Gregory Winner Compare With Other Companies In The Industry?

Our data indicates that Ingenta plc has a market capitalization of UK£20m, and total annual CEO compensation was reported as UK£286k for the year to December 2021. We note that's an increase of 25% above last year. In particular, the salary of UK£251.0k, makes up a huge portion of the total compensation being paid to the CEO.

On comparing similar-sized companies in the industry with market capitalizations below UK£177m, we found that the median total CEO compensation was UK£286k. So it looks like Ingenta compensates Gregory Winner in line with the median for the industry.

| Component | 2021 | 2020 | Proportion (2021) |

| Salary | UK£251k | UK£200k | 88% |

| Other | UK£35k | UK£28k | 12% |

| Total Compensation | UK£286k | UK£228k | 100% |

Talking in terms of the industry, salary represented approximately 65% of total compensation out of all the companies we analyzed, while other remuneration made up 35% of the pie. According to our research, Ingenta has allocated a higher percentage of pay to salary in comparison to the wider industry. If salary dominates total compensation, it suggests that CEO compensation is leaning less towards the variable component, which is usually linked with performance.

A Look at Ingenta plc's Growth Numbers

Over the past three years, Ingenta plc has seen its earnings per share (EPS) grow by 114% per year. It achieved revenue growth of 2.3% over the last year.

Overall this is a positive result for shareholders, showing that the company has improved in recent years. It's nice to see revenue heading northwards, as this is consistent with healthy business conditions. Looking ahead, you might want to check this free visual report on analyst forecasts for the company's future earnings..

Has Ingenta plc Been A Good Investment?

We think that the total shareholder return of 63%, over three years, would leave most Ingenta plc shareholders smiling. As a result, some may believe the CEO should be paid more than is normal for companies of similar size.

In Summary...

Seeing that the company has put in a relatively good performance, the CEO remuneration policy may not be the focus at the AGM. However, investors will get the chance to engage on key strategic initiatives and future growth opportunities for the company and set their longer-term expectations.

We can learn a lot about a company by studying its CEO compensation trends, along with looking at other aspects of the business. That's why we did our research, and identified 3 warning signs for Ingenta (of which 1 doesn't sit too well with us!) that you should know about in order to have a holistic understanding of the stock.

Switching gears from Ingenta, if you're hunting for a pristine balance sheet and premium returns, this free list of high return, low debt companies is a great place to look.

Mobile Infrastructure for Defense and Disaster

The next wave in robotics isn't humanoid. Its fully autonomous towers delivering 5G, ISR, and radar in under 30 minutes, anywhere.

Get the investor briefing before the next round of contracts

Sponsored On Behalf of CiTechNew: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About AIM:ING

Ingenta

Provides content management, advertising, and commercial enterprise solutions and services in the United Kingdom, the United States, the Netherlands, France, and internationally.

Outstanding track record with flawless balance sheet.

Market Insights

Weekly Picks

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Recently Updated Narratives

Airbnb Stock: Platform Growth in a World of Saturation and Scrutiny

Adobe Stock: AI-Fueled ARR Growth Pushes Guidance Higher, But Cost Pressures Loom

Thomson Reuters Stock: When Legal Intelligence Becomes Mission-Critical Infrastructure

Popular Narratives

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

The AI Infrastructure Giant Grows Into Its Valuation

Trending Discussion