Advertisement

- United Kingdom

- /

- Specialty Stores

- /

- AIM:G4M

These 4 Measures Indicate That Gear4music (Holdings) (LON:G4M) Is Using Debt Reasonably Well

David Iben put it well when he said, 'Volatility is not a risk we care about. What we care about is avoiding the permanent loss of capital.' So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. As with many other companies Gear4music (Holdings) plc (LON:G4M) makes use of debt. But the real question is whether this debt is making the company risky.

When Is Debt Dangerous?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. Ultimately, if the company can't fulfill its legal obligations to repay debt, shareholders could walk away with nothing. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. When we think about a company's use of debt, we first look at cash and debt together.

View our latest analysis for Gear4music (Holdings)

What Is Gear4music (Holdings)'s Debt?

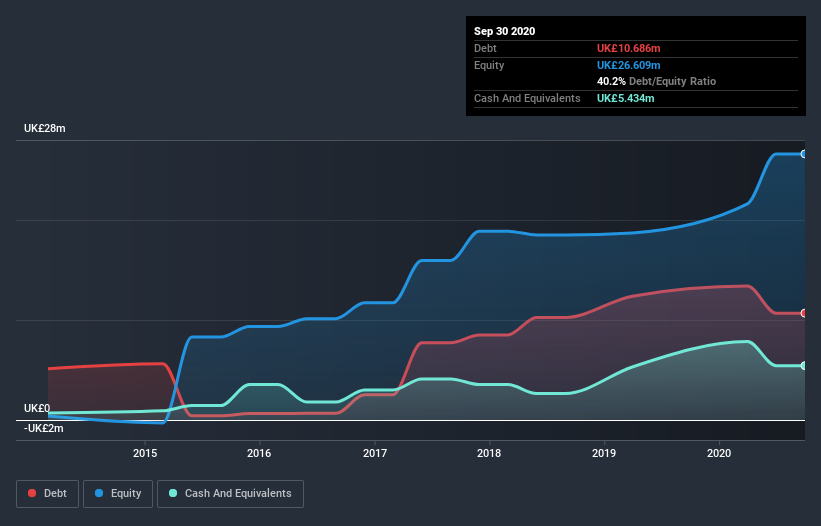

You can click the graphic below for the historical numbers, but it shows that Gear4music (Holdings) had UK£10.7m of debt in September 2020, down from UK£13.4m, one year before. On the flip side, it has UK£5.43m in cash leading to net debt of about UK£5.25m.

How Strong Is Gear4music (Holdings)'s Balance Sheet?

Zooming in on the latest balance sheet data, we can see that Gear4music (Holdings) had liabilities of UK£27.4m due within 12 months and liabilities of UK£14.1m due beyond that. On the other hand, it had cash of UK£5.43m and UK£3.55m worth of receivables due within a year. So its liabilities total UK£32.5m more than the combination of its cash and short-term receivables.

Since publicly traded Gear4music (Holdings) shares are worth a total of UK£176.0m, it seems unlikely that this level of liabilities would be a major threat. However, we do think it is worth keeping an eye on its balance sheet strength, as it may change over time.

In order to size up a company's debt relative to its earnings, we calculate its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and its earnings before interest and tax (EBIT) divided by its interest expense (its interest cover). This way, we consider both the absolute quantum of the debt, as well as the interest rates paid on it.

Gear4music (Holdings)'s net debt is only 0.50 times its EBITDA. And its EBIT covers its interest expense a whopping 13.5 times over. So you could argue it is no more threatened by its debt than an elephant is by a mouse. Even more impressive was the fact that Gear4music (Holdings) grew its EBIT by 398% over twelve months. If maintained that growth will make the debt even more manageable in the years ahead. When analysing debt levels, the balance sheet is the obvious place to start. But ultimately the future profitability of the business will decide if Gear4music (Holdings) can strengthen its balance sheet over time. So if you're focused on the future you can check out this free report showing analyst profit forecasts.

Finally, while the tax-man may adore accounting profits, lenders only accept cold hard cash. So the logical step is to look at the proportion of that EBIT that is matched by actual free cash flow. Looking at the most recent three years, Gear4music (Holdings) recorded free cash flow of 34% of its EBIT, which is weaker than we'd expect. That's not great, when it comes to paying down debt.

Our View

The good news is that Gear4music (Holdings)'s demonstrated ability to cover its interest expense with its EBIT delights us like a fluffy puppy does a toddler. But truth be told we feel its conversion of EBIT to free cash flow does undermine this impression a bit. Taking all this data into account, it seems to us that Gear4music (Holdings) takes a pretty sensible approach to debt. While that brings some risk, it can also enhance returns for shareholders. There's no doubt that we learn most about debt from the balance sheet. However, not all investment risk resides within the balance sheet - far from it. Be aware that Gear4music (Holdings) is showing 4 warning signs in our investment analysis , and 1 of those is a bit concerning...

If you're interested in investing in businesses that can grow profits without the burden of debt, then check out this free list of growing businesses that have net cash on the balance sheet.

If you’re looking to trade Gear4music (Holdings), open an account with the lowest-cost* platform trusted by professionals, Interactive Brokers. Their clients from over 200 countries and territories trade stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About AIM:G4M

Gear4music (Holdings)

Engages in the retail of musical instruments, musician equipment, and audio-visual equipment in the United Kingdom, rest of Europe, and internationally.

Excellent balance sheet with proven track record.

Market Insights

Advertisement

Community Narratives

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value US$300.00|6.3% undervalued

OS

Community Contributor

Flowers Foods Pays A Fair Price For Health

Fair Value US$16.12|26.0% undervalued

NV

Community Contributor

TMX Group will thrive with 33.3% profit margin and enduring market moat

Fair Value CA$49.90|3.7% overvalued

LI

Community Contributor