Advertisement

- United Kingdom

- /

- Retail REITs

- /

- LSE:NRR

NewRiver REIT plc's (LON:NRR) CEO Might Not Expect Shareholders To Be So Generous This Year

NewRiver REIT plc (LON:NRR) has not performed well recently and CEO Allan Lockhart will probably need to up their game. Shareholders will be interested in what the board will have to say about turning performance around at the next AGM on 27 July 2021. This will be also be a chance where they can challenge the board on company direction and vote on resolutions such as executive remuneration. The data we present below explains why we think CEO compensation is not consistent with recent performance.

View our latest analysis for NewRiver REIT

Comparing NewRiver REIT plc's CEO Compensation With the industry

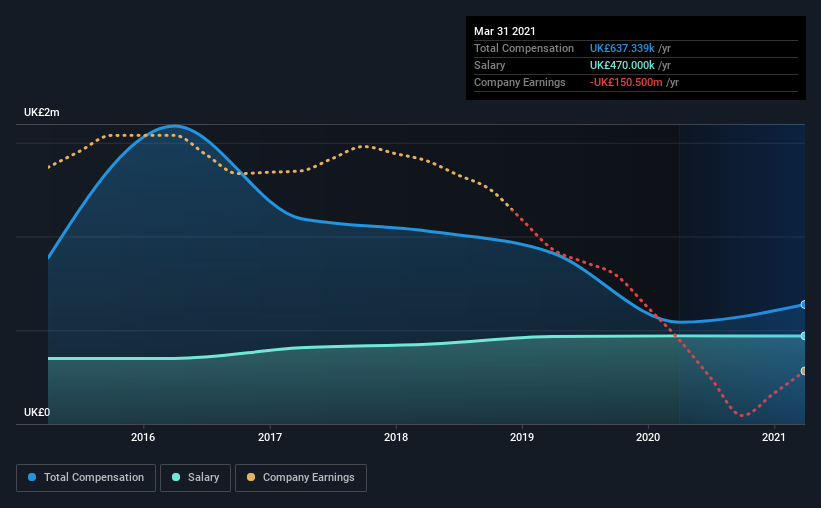

Our data indicates that NewRiver REIT plc has a market capitalization of UK£251m, and total annual CEO compensation was reported as UK£637k for the year to March 2021. That's a notable increase of 17% on last year. We note that the salary portion, which stands at UK£470.0k constitutes the majority of total compensation received by the CEO.

In comparison with other companies in the industry with market capitalizations ranging from UK£146m to UK£585m, the reported median CEO total compensation was UK£403k. Hence, we can conclude that Allan Lockhart is remunerated higher than the industry median. Moreover, Allan Lockhart also holds UK£284k worth of NewRiver REIT stock directly under their own name.

| Component | 2021 | 2020 | Proportion (2021) |

| Salary | UK£470k | UK£470k | 74% |

| Other | UK£167k | UK£73k | 26% |

| Total Compensation | UK£637k | UK£543k | 100% |

Speaking on an industry level, nearly 45% of total compensation represents salary, while the remainder of 55% is other remuneration. According to our research, NewRiver REIT has allocated a higher percentage of pay to salary in comparison to the wider industry. If total compensation veers towards salary, it suggests that the variable portion - which is generally tied to performance, is lower.

NewRiver REIT plc's Growth

Over the last three years, NewRiver REIT plc has shrunk its earnings per share by 93% per year. It saw its revenue drop 36% over the last year.

Overall this is not a very positive result for shareholders. This is compounded by the fact revenue is actually down on last year. It's hard to argue the company is firing on all cylinders, so shareholders might be averse to high CEO remuneration. Historical performance can sometimes be a good indicator on what's coming up next but if you want to peer into the company's future you might be interested in this free visualization of analyst forecasts.

Has NewRiver REIT plc Been A Good Investment?

Few NewRiver REIT plc shareholders would feel satisfied with the return of -66% over three years. Therefore, it might be upsetting for shareholders if the CEO were paid generously.

To Conclude...

Along with the business performing poorly, shareholders have suffered with poor share price returns on their investments, suggesting that there's little to no chance of them being in favor of a CEO pay raise. At the upcoming AGM, they can question the management's plans and strategies to turn performance around and reassess their investment thesis in regards to the company.

While it is important to pay attention to CEO remuneration, investors should also consider other elements of the business. That's why we did some digging and identified 2 warning signs for NewRiver REIT that investors should think about before committing capital to this stock.

Of course, you might find a fantastic investment by looking at a different set of stocks. So take a peek at this free list of interesting companies.

When trading NewRiver REIT or any other investment, use the platform considered by many to be the Professional's Gateway to the Worlds Market, Interactive Brokers. You get the lowest-cost* trading on stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

Valuation is complex, but we're here to simplify it.

Discover if NewRiver REIT might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About LSE:NRR

NewRiver REIT

NewRiver REIT plc ('NewRiver') is a leading Real Estate Investment Trust specialising in buying, managing and developing resilient retail assets throughout the UK.

Reasonable growth potential with mediocre balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

Groundbreaking therapies that could change the treatment landscape for PTSD, fibromyalgia, MS & Alzheimer’s

Fair Value US$6.20|86.9% undervalued

CM

Community Contributor

DigitalOcean Will Grow 14% by Embracing AI with Paperspace Acquisition

Fair Value US$50.00|42.8% undervalued

NE

Community Contributor

Viant Technology: A Rising AdTech Challenger in the AI-Powered CTV Market

Fair Value US$38.61|66.0% undervalued

BL

Community Contributor

Volvo will Accelerate Forward into Electric and Autonomous Leadership in Five Years

Fair Value SEK 438.80|40.8% undervalued

UN

Community Contributor