- United Kingdom

- /

- Retail REITs

- /

- LSE:HMSO

Growth Investors: Industry Analysts Just Upgraded Their Hammerson plc (LON:HMSO) Revenue Forecasts By 24%

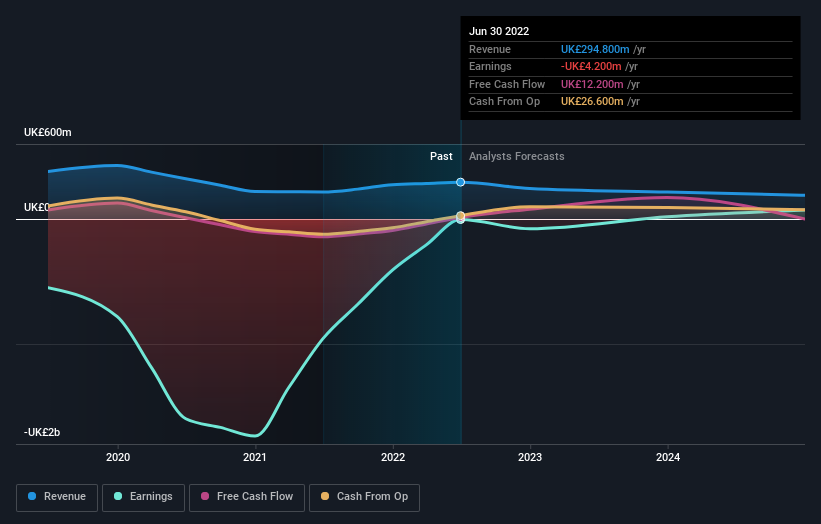

Celebrations may be in order for Hammerson plc (LON:HMSO) shareholders, with the analysts delivering a significant upgrade to their statutory estimates for the company. The analysts have sharply increased their revenue numbers, with a view that Hammerson will make substantially more sales than they'd previously expected.

Following the latest upgrade, the ten analysts covering Hammerson provided consensus estimates of UK£245m revenue in 2022, which would reflect a chunky 17% decline on its sales over the past 12 months. Before the latest update, the analysts were foreseeing UK£197m of revenue in 2022. It looks like there's been a clear increase in optimism around Hammerson, given the considerable lift to revenue forecasts.

Check out our latest analysis for Hammerson

Looking at the bigger picture now, one of the ways we can make sense of these forecasts is to see how they measure up against both past performance and industry growth estimates. One more thing stood out to us about these estimates, and it's the idea that Hammerson's decline is expected to accelerate, with revenues forecast to fall at an annualised rate of 31% to the end of 2022. This tops off a historical decline of 16% a year over the past five years. Compare this against analyst estimates for companies in the broader industry, which suggest that revenues (in aggregate) are expected to grow 6.5% annually. So while a broad number of companies are forecast to grow, unfortunately Hammerson is expected to see its sales affected worse than other companies in the industry.

The Bottom Line

The highlight for us was that analysts increased their revenue forecasts for Hammerson this year. They're also anticipating slower revenue growth than the wider market. Given that analysts appear to be expecting substantial improvement in the sales pipeline, now could be the right time to take another look at Hammerson.

Better yet, Hammerson is expected to break-even soon - within the next few years - according to analyst forecasts, which would be a momentous event for shareholders. You can learn more about these forecasts, for free on our platform here.

Another way to search for interesting companies that could be reaching an inflection point is to track whether management are buying or selling, with our free list of growing companies that insiders are buying.

Valuation is complex, but we're here to simplify it.

Discover if Hammerson might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About LSE:HMSO

Hammerson

Hammerson is a cities business. An owner, operator and developer of prime urban real estate, with a portfolio value of £4.7billion (as at 30 June 2023), in some of the fastest growing cities in the UK, Ireland and France.

Moderate growth potential and slightly overvalued.

Similar Companies

Market Insights

Community Narratives