- United Kingdom

- /

- Retail REITs

- /

- LSE:HMSO

Analysts Have Just Cut Their Hammerson plc (LON:HMSO) Revenue Estimates By 17%

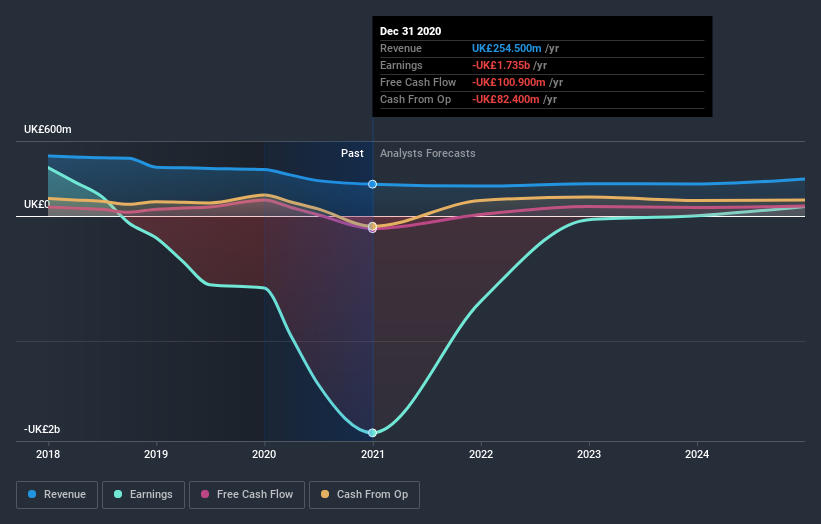

The latest analyst coverage could presage a bad day for Hammerson plc (LON:HMSO), with the analysts making across-the-board cuts to their statutory estimates that might leave shareholders a little shell-shocked. This report focused on revenue estimates, and it looks as though the consensus view of the business has become substantially more conservative.

Following the downgrade, the consensus from eight analysts covering Hammerson is for revenues of UK£226m in 2021, implying an uncomfortable 11% decline in sales compared to the last 12 months. Prior to the latest estimates, the analysts were forecasting revenues of UK£273m in 2021. It looks like forecasts have become a fair bit less optimistic on Hammerson, given the substantial drop in revenue estimates.

View our latest analysis for Hammerson

The consensus price target rose 8.8% to UK£0.28, with the analysts clearly more optimistic about Hammerson's prospects following this update. That's not the only conclusion we can draw from this data however, as some investors also like to consider the spread in estimates when evaluating analyst price targets. Currently, the most bullish analyst values Hammerson at UK£0.90 per share, while the most bearish prices it at UK£0.10. So we wouldn't be assigning too much credibility to analyst price targets in this case, because there are clearly some widely differing views on what kind of performance this business can generate. With this in mind, we wouldn't rely too heavily on the consensus price target, as it is just an average and analysts clearly have some deeply divergent views on the business.

These estimates are interesting, but it can be useful to paint some more broad strokes when seeing how forecasts compare, both to the Hammerson's past performance and to peers in the same industry. Over the past five years, revenues have declined around 7.3% annually. Worse, forecasts are essentially predicting the decline to accelerate, with the estimate for an annualised 11% decline in revenue until the end of 2021. By contrast, our data suggests that other companies (with analyst coverage) in a similar industry are forecast to see their revenue grow 4.0% per year. So while a broad number of companies are forecast to grow, unfortunately Hammerson is expected to see its sales affected worse than other companies in the industry.

The Bottom Line

The most important thing to take away is that analysts cut their revenue estimates for this year. They also expect company revenue to perform worse than the wider market. There was also an increase in the price target, suggesting that there is more optimism baked into the forecasts than there was previously. Often, one downgrade can set off a daisy-chain of cuts, especially if an industry is in decline. So we wouldn't be surprised if the market became a lot more cautious on Hammerson after today.

After a downgrade like this, it's pretty clear that previous forecasts were too optimistic. What's more, we've spotted several possible issues with Hammerson's business, like major dilution from new stock issuance in the past year. Learn more, and discover the 1 other risk we've identified, for free on our platform here.

Another way to search for interesting companies that could be reaching an inflection point is to track whether management are buying or selling, with our free list of growing companies that insiders are buying.

If you’re looking to trade Hammerson, open an account with the lowest-cost* platform trusted by professionals, Interactive Brokers. Their clients from over 200 countries and territories trade stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

Valuation is complex, but we're here to simplify it.

Discover if Hammerson might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About LSE:HMSO

Hammerson

Hammerson is a cities business. An owner, operator and developer of prime urban real estate, with a portfolio value of £4.7billion (as at 30 June 2023), in some of the fastest growing cities in the UK, Ireland and France.

Reasonable growth potential and fair value.

Similar Companies

Market Insights

Community Narratives