What Can We Learn About Rightmove's (LON:RMV) CEO Compensation?

Peter Brooks-Johnson became the CEO of Rightmove plc (LON:RMV) in 2017, and we think it's a good time to look at the executive's compensation against the backdrop of overall company performance. This analysis will also assess whether Rightmove pays its CEO appropriately, considering recent earnings growth and total shareholder returns.

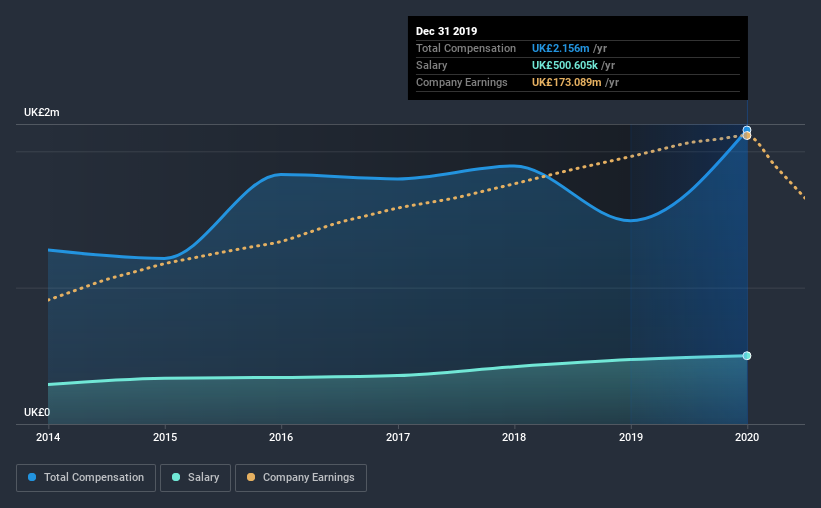

View our latest analysis for Rightmove

Comparing Rightmove plc's CEO Compensation With the industry

According to our data, Rightmove plc has a market capitalization of UK£5.4b, and paid its CEO total annual compensation worth UK£2.2m over the year to December 2019. We note that's an increase of 45% above last year. While this analysis focuses on total compensation, it's worth acknowledging that the salary portion is lower, valued at UK£501k.

On comparing similar companies from the same industry with market caps ranging from UK£3.0b to UK£9.0b, we found that the median CEO total compensation was UK£2.2m. From this we gather that Peter Brooks-Johnson is paid around the median for CEOs in the industry. Moreover, Peter Brooks-Johnson also holds UK£13m worth of Rightmove stock directly under their own name, which reveals to us that they have a significant personal stake in the company.

| Component | 2019 | 2018 | Proportion (2019) |

| Salary | UK£501k | UK£472k | 23% |

| Other | UK£1.7m | UK£1.0m | 77% |

| Total Compensation | UK£2.2m | UK£1.5m | 100% |

Talking in terms of the industry, salary represented approximately 60% of total compensation out of all the companies we analyzed, while other remuneration made up 40% of the pie. It's interesting to note that Rightmove allocates a smaller portion of compensation to salary in comparison to the broader industry. If non-salary compensation dominates total pay, it's an indicator that the executive's salary is tied to company performance.

Rightmove plc's Growth

Rightmove plc has seen its earnings per share (EPS) increase by 2.0% a year over the past three years. It saw its revenue drop 14% over the last year.

We would prefer it if there was revenue growth, but it is good to see a modest EPS growth at least. These two metrics are moving in different directions, so while it's hard to be confident judging performance, we think the stock is worth watching. Looking ahead, you might want to check this free visual report on analyst forecasts for the company's future earnings..

Has Rightmove plc Been A Good Investment?

We think that the total shareholder return of 60%, over three years, would leave most Rightmove plc shareholders smiling. As a result, some may believe the CEO should be paid more than is normal for companies of similar size.

To Conclude...

As we noted earlier, Rightmove pays its CEO in line with similar-sized companies belonging to the same industry. But the business isn't reporting great numbers in terms of EPS growth. At the same time, shareholder returns have remained strong over the same period. We would like to see EPS growth from the business, although we wouldn't say the CEO compensation is high.

Whatever your view on compensation, you might want to check if insiders are buying or selling Rightmove shares (free trial).

Of course, you might find a fantastic investment by looking at a different set of stocks. So take a peek at this free list of interesting companies.

If you decide to trade Rightmove, use the lowest-cost* platform that is rated #1 Overall by Barron’s, Interactive Brokers. Trade stocks, options, futures, forex, bonds and funds on 135 markets, all from a single integrated account. Promoted

The New Payments ETF Is Live on NASDAQ:

Money is moving to real-time rails, and a newly listed ETF now gives investors direct exposure. Fast settlement. Institutional custody. Simple access.

Explore how this launch could reshape portfolios

Sponsored ContentNew: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com.

About LSE:RMV

Rightmove

Operates digital property advertising and information portal in the United Kingdom and internationally.

Flawless balance sheet and fair value.

Similar Companies

Market Insights

Weekly Picks

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Recently Updated Narratives

Meta’s Bold Bet on AI Pays Off

ADP Stock: Solid Fundamentals, But AI Investments Test Its Margin Resilience

Visa Stock: The Toll Booth at the Center of Global Commerce

Popular Narratives

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

The AI Infrastructure Giant Grows Into Its Valuation

Trending Discussion