- United Kingdom

- /

- Specialty Stores

- /

- LSE:PETS

3 Undervalued Small Caps On UK Exchange With Insider Action

Reviewed by Simply Wall St

The United Kingdom market has recently faced challenges, with the FTSE 100 and FTSE 250 indices experiencing declines due to weak trade data from China, highlighting concerns about global economic recovery. As these broader market conditions unfold, investors may find opportunities in small-cap stocks that demonstrate resilience and potential for growth despite external pressures. In this context, identifying companies with solid fundamentals and insider activity can be particularly appealing for those navigating the current economic landscape.

Top 10 Undervalued Small Caps With Insider Buying In The United Kingdom

| Name | PE | PS | Discount to Fair Value | Value Rating |

|---|---|---|---|---|

| Headlam Group | NA | 0.2x | 26.19% | ★★★★★☆ |

| Sabre Insurance Group | 11.1x | 1.4x | 14.17% | ★★★★☆☆ |

| Marlowe | NA | 0.7x | 47.81% | ★★★★☆☆ |

| J D Wetherspoon | 15.5x | 0.4x | 18.39% | ★★★★☆☆ |

| Optima Health | NA | 1.2x | 40.00% | ★★★★☆☆ |

| iomart Group | 29.6x | 0.8x | 24.11% | ★★★☆☆☆ |

| Reach | 6.8x | 0.5x | -133.72% | ★★★☆☆☆ |

| Great Portland Estates | NA | 8.0x | -17.53% | ★★★☆☆☆ |

| Genus | 141.9x | 1.7x | 26.73% | ★★★☆☆☆ |

| THG | NA | 0.4x | -1054.57% | ★★★☆☆☆ |

We'll examine a selection from our screener results.

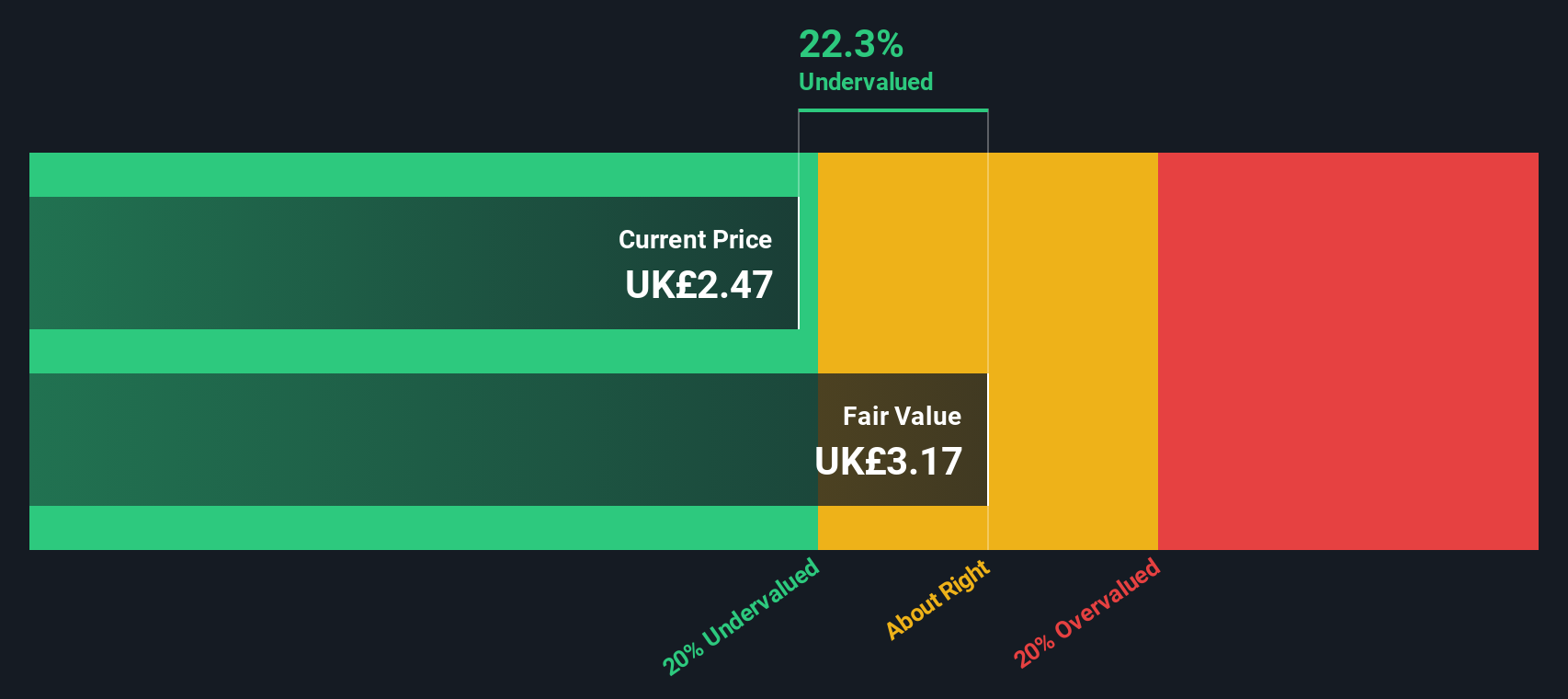

Pets at Home Group (LSE:PETS)

Simply Wall St Value Rating: ★★★★★★

Overview: Pets at Home Group operates as a leading UK-based pet care business, encompassing retail and veterinary services, with a market cap of approximately £1.52 billion.

Operations: PETS generates revenue primarily from its Retail and Vet Group segments, with the Retail segment contributing significantly more. The company's gross profit margin has shown a declining trend, reaching 46.80% in late 2024. Operating expenses are mainly driven by sales and marketing costs, which have consistently been a substantial part of the total expenses over multiple periods.

PE: 11.6x

Pets at Home Group, with its recent earnings call on November 27, 2024, highlighted a promising half-year performance. Sales reached £789 million, up from £774 million the previous year, while net income jumped to £37.6 million from £25.3 million. Insider confidence is evident with share purchases in the past months. Despite relying solely on external borrowing for funding, the company projects an annual earnings growth of 11%. An interim dividend increase to 4.7 pence per share signals potential shareholder value enhancement amidst its small-cap positioning in the UK market.

- Delve into the full analysis valuation report here for a deeper understanding of Pets at Home Group.

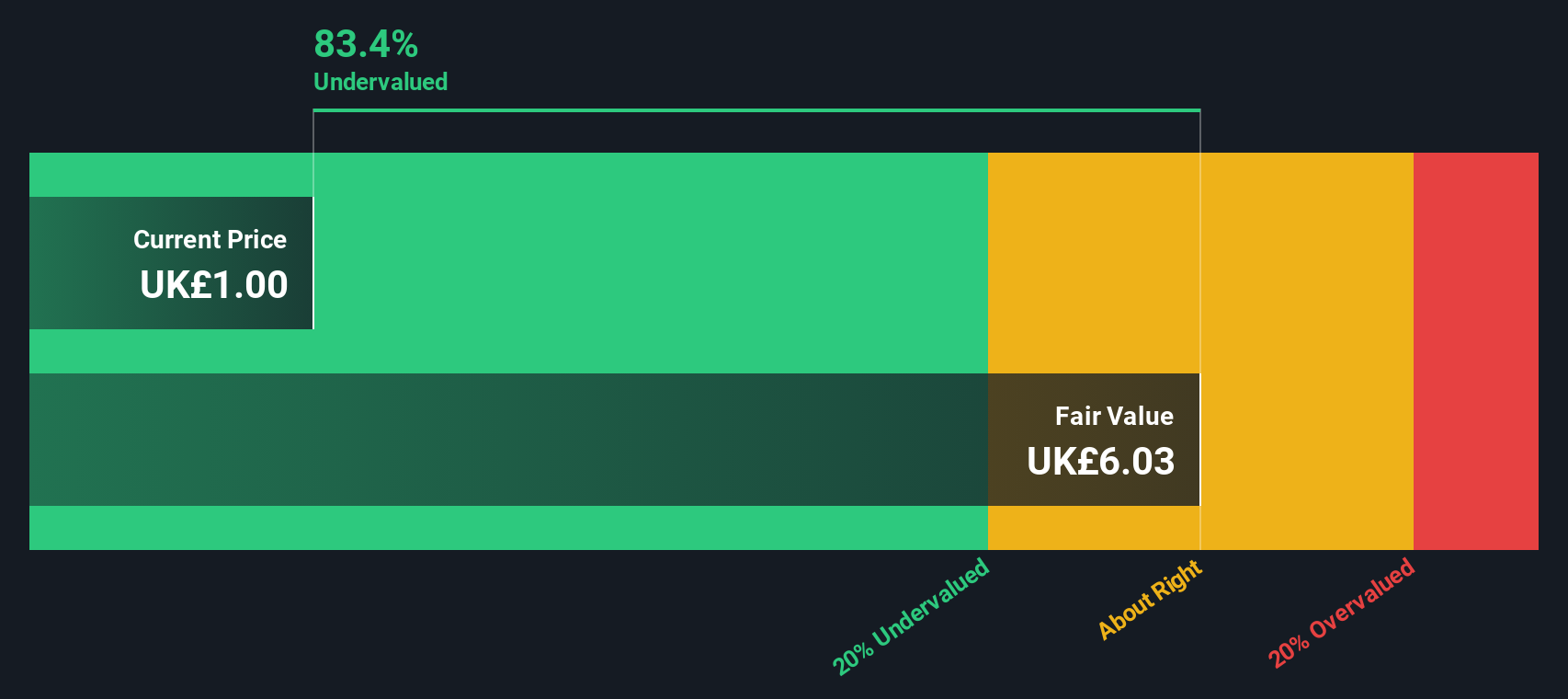

Reach (LSE:RCH)

Simply Wall St Value Rating: ★★★☆☆☆

Overview: Reach is a media company primarily engaged in publishing newspapers, with operations contributing to its market capitalization of approximately £0.23 billion.

Operations: Reach's revenue is primarily derived from its publishing segment, specifically newspapers. The company's gross profit margin has shown variability over the years, with a recent figure of 42.20%. Operating expenses are a significant part of the cost structure, including general and administrative expenses and sales and marketing costs.

PE: 6.8x

Reach, a small company in the UK, has recently reported a 2.5% drop in quarterly revenue and a 4.3% decline year-to-date as of September 2024. Despite these challenges, insider confidence is evident with recent share purchases throughout the year, signaling belief in its potential value. While reliant on external borrowing for funding, Reach's earnings are projected to grow annually by 17.79%, suggesting optimism for future performance amidst current hurdles.

- Unlock comprehensive insights into our analysis of Reach stock in this valuation report.

Gain insights into Reach's past trends and performance with our Past report.

Videndum (LSE:VID)

Simply Wall St Value Rating: ★★★★☆☆

Overview: Videndum operates in the media and entertainment industry, providing solutions across media, creative, and production segments with a market cap of £0.36 billion.

Operations: The company's revenue is primarily derived from Media Solutions (£144.70 million), Creative Solutions (£54.90 million), and Production Solutions (£98 million). Over recent periods, the gross profit margin has shown a decreasing trend, reaching 36.65% by mid-2024. Operating expenses are significant, with general and administrative costs frequently comprising a large portion of these expenses, impacting overall profitability.

PE: -9.3x

Videndum, a smaller UK-listed company, is navigating a challenging period with notable changes in its leadership team. Despite reporting a first-half net loss of £12.8 million for 2024 compared to the previous year's £46.5 million loss, the company has initiated a share repurchase program authorized to buy back up to 10% of its shares, signaling potential insider confidence in future prospects. However, Videndum's reliance on external borrowing highlights financial risk amidst volatile share prices and recent index exclusion from S&P Global BMI Index.

- Click here and access our complete valuation analysis report to understand the dynamics of Videndum.

Assess Videndum's past performance with our detailed historical performance reports.

Key Takeaways

- Explore the 28 names from our Undervalued UK Small Caps With Insider Buying screener here.

- Have you diversified into these companies? Leverage the power of Simply Wall St's portfolio to keep a close eye on market movements affecting your investments.

- Simply Wall St is your key to unlocking global market trends, a free user-friendly app for forward-thinking investors.

Curious About Other Options?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About LSE:PETS

Pets at Home Group

Engages in the specialist omnichannel retailing of pet food, pet related products, and pet accessories in the United Kingdom.

Very undervalued 6 star dividend payer.