This article will reflect on the compensation paid to Kevin Lyons-Tarr who has served as CEO of 4imprint Group plc (LON:FOUR) since 2015. This analysis will also assess whether 4imprint Group pays its CEO appropriately, considering recent earnings growth and total shareholder returns.

Check out our latest analysis for 4imprint Group

How Does Total Compensation For Kevin Lyons-Tarr Compare With Other Companies In The Industry?

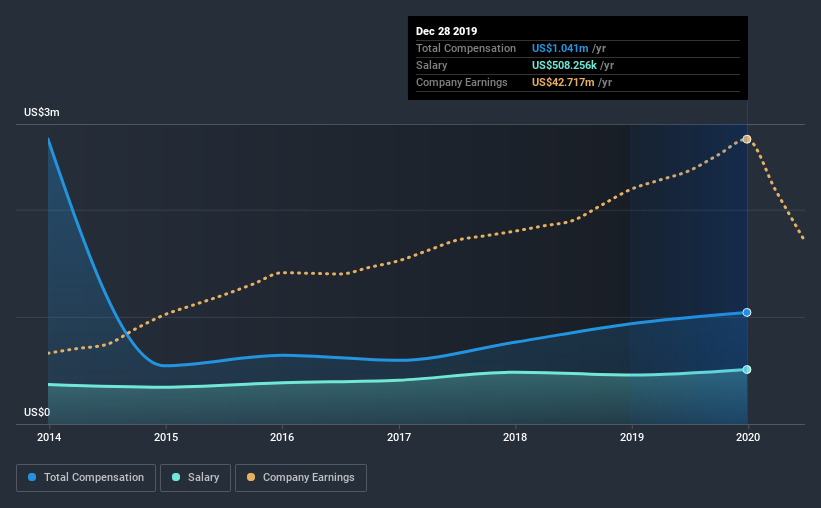

According to our data, 4imprint Group plc has a market capitalization of UK£722m, and paid its CEO total annual compensation worth UK£1.0m over the year to December 2019. That's a notable increase of 11% on last year. While we always look at total compensation first, our analysis shows that the salary component is less, at UK£508k.

On examining similar-sized companies in the industry with market capitalizations between UK£294m and UK£1.2b, we discovered that the median CEO total compensation of that group was UK£959k. So it looks like 4imprint Group compensates Kevin Lyons-Tarr in line with the median for the industry. Moreover, Kevin Lyons-Tarr also holds UK£6.8m worth of 4imprint Group stock directly under their own name, which reveals to us that they have a significant personal stake in the company.

| Component | 2019 | 2018 | Proportion (2019) |

| Salary | UK£508k | UK£457k | 49% |

| Other | UK£533k | UK£480k | 51% |

| Total Compensation | UK£1.0m | UK£936k | 100% |

Speaking on an industry level, nearly 45% of total compensation represents salary, while the remainder of 55% is other remuneration. 4imprint Group is largely mirroring the industry average when it comes to the share a salary enjoys in overall compensation. It's important to note that a slant towards non-salary compensation suggests that total pay is tied to the company's performance.

4imprint Group plc's Growth

Over the last three years, 4imprint Group plc has not seen its earnings per share change much, though they have deteriorated slightly. It saw its revenue drop 9.2% over the last year.

The lack of EPS growth is certainly unimpressive. And the impression is worse when you consider revenue is down year-on-year. So given this relatively weak performance, shareholders would probably not want to see high compensation for the CEO. Looking ahead, you might want to check this free visual report on analyst forecasts for the company's future earnings..

Has 4imprint Group plc Been A Good Investment?

Most shareholders would probably be pleased with 4imprint Group plc for providing a total return of 49% over three years. So they may not be at all concerned if the CEO were to be paid more than is normal for companies around the same size.

To Conclude...

As we noted earlier, 4imprint Group pays its CEO in line with similar-sized companies belonging to the same industry. This doesn't look good when you see that EPS growth over the last three years has been negative. But on the bright side, shareholder returns have moved northward during the same period. We wouldn't say CEO compensation is too high, but shareholders might think performance needs to be improved before paying any more.

It is always advisable to analyse CEO pay, along with performing a thorough analysis of the company's key performance areas. In our study, we found 2 warning signs for 4imprint Group you should be aware of, and 1 of them is a bit concerning.

Of course, you might find a fantastic investment by looking at a different set of stocks. So take a peek at this free list of interesting companies.

When trading 4imprint Group or any other investment, use the platform considered by many to be the Professional's Gateway to the Worlds Market, Interactive Brokers. You get the lowest-cost* trading on stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

If you're looking to trade 4imprint Group, open an account with the lowest-cost platform trusted by professionals, Interactive Brokers.

With clients in over 200 countries and territories, and access to 160 markets, IBKR lets you trade stocks, options, futures, forex, bonds and funds from a single integrated account.

Enjoy no hidden fees, no account minimums, and FX conversion rates as low as 0.03%, far better than what most brokers offer.

Sponsored ContentNew: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com.

About LSE:FOUR

4imprint Group

Operates as a direct marketer of promotional products in North America, the United Kingdom, and Ireland.

Flawless balance sheet, undervalued and pays a dividend.

Similar Companies

Market Insights

Community Narratives