- United Kingdom

- /

- Software

- /

- LSE:PINE

Exploring Undiscovered Gems Including Bloomsbury Publishing And Two More Small Caps

Reviewed by Simply Wall St

In the last week, the United Kingdom market has remained flat, but over the past 12 months, it has experienced an 11% rise with earnings forecasted to grow by 14% annually. In this context of steady growth and potential for future gains, identifying undiscovered gems like Bloomsbury Publishing and other small-cap stocks can offer unique opportunities for investors seeking to capitalize on emerging prospects in a dynamic market environment.

Top 10 Undiscovered Gems With Strong Fundamentals In The United Kingdom

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| Andrews Sykes Group | NA | 2.15% | 4.93% | ★★★★★★ |

| B.P. Marsh & Partners | NA | 24.01% | 24.81% | ★★★★★★ |

| M&G Credit Income Investment Trust | NA | 17.28% | 15.80% | ★★★★★★ |

| London Security | 0.22% | 10.13% | 7.75% | ★★★★★★ |

| Globaltrans Investment | 15.40% | 2.68% | 16.51% | ★★★★★★ |

| Impellam Group | 31.12% | -5.43% | -6.86% | ★★★★★★ |

| Kodal Minerals | NA | nan | 72.74% | ★★★★★★ |

| VH Global Sustainable Energy Opportunities | NA | 18.30% | 20.03% | ★★★★★★ |

| BBGI Global Infrastructure | 0.02% | 3.08% | 6.85% | ★★★★★☆ |

| Goodwin | 52.21% | 9.26% | 13.12% | ★★★★★☆ |

Here we highlight a subset of our preferred stocks from the screener.

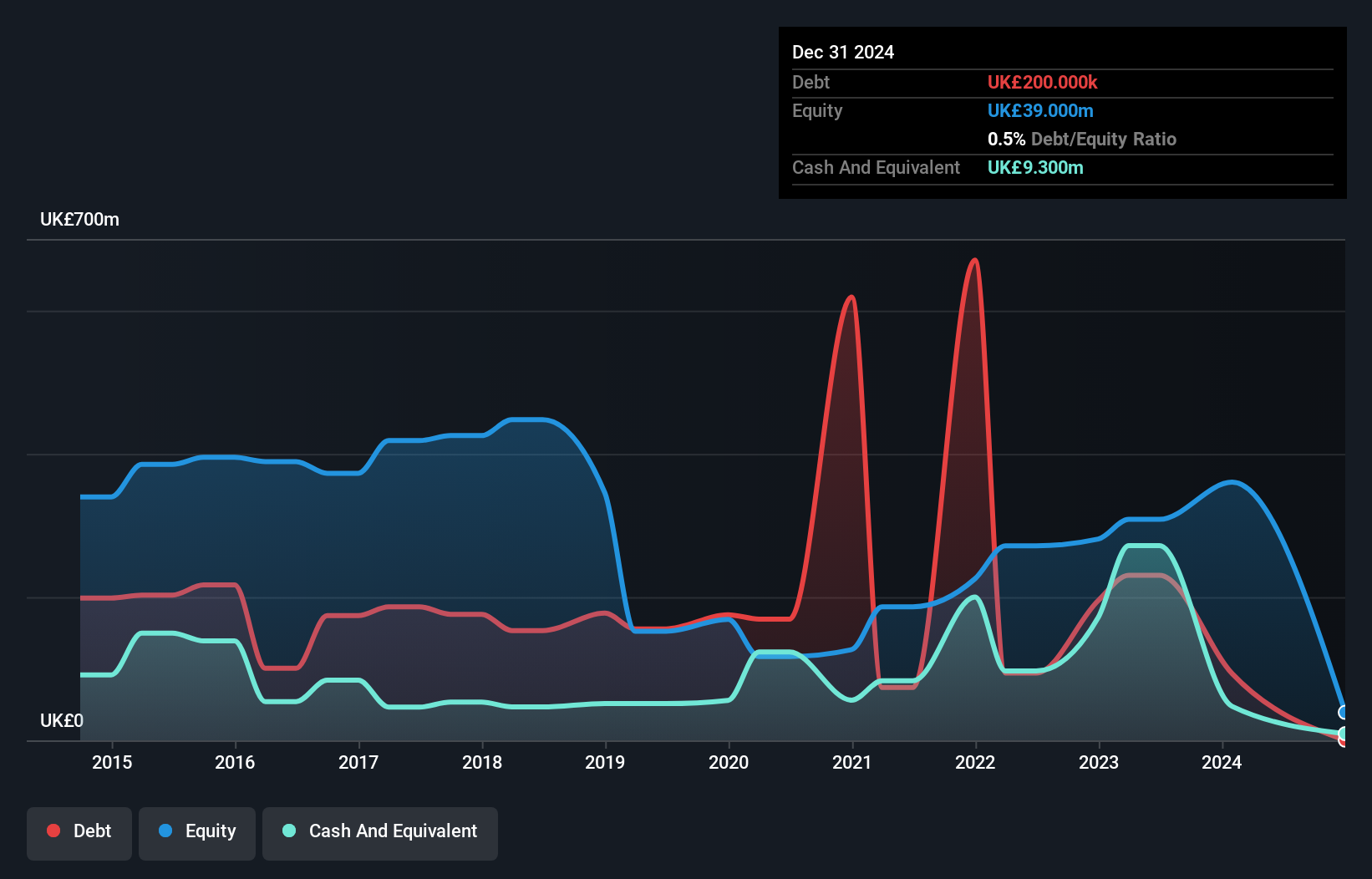

Bloomsbury Publishing (LSE:BMY)

Simply Wall St Value Rating: ★★★★★★

Overview: Bloomsbury Publishing Plc is a global publisher of academic, educational, and general fiction and non-fiction books catering to children, general readers, teachers, students, researchers, libraries, and professionals with a market cap of £553.57 million.

Operations: Bloomsbury Publishing derives its revenue primarily from four segments: Consumer - Adult Trade (£57.87 million), Consumer - Children's Trade (£191.33 million), Non-Consumer - Special Interest (£22.95 million), and Non-Consumer - Academic & Professional (£70.50 million).

Bloomsbury Publishing, a nimble player in the UK publishing scene, has been making waves with its recent addition to multiple FTSE indices. Over the past year, earnings surged by 60%, outpacing the media industry's 32% growth rate. The company trades at a substantial discount of about 51% below its estimated fair value and boasts high-quality earnings. With no debt on its books for five years and positive free cash flow standing at £31.78 million as of October 2024, Bloomsbury seems well-positioned despite recent notable insider selling activity over the last quarter.

- Delve into the full analysis health report here for a deeper understanding of Bloomsbury Publishing.

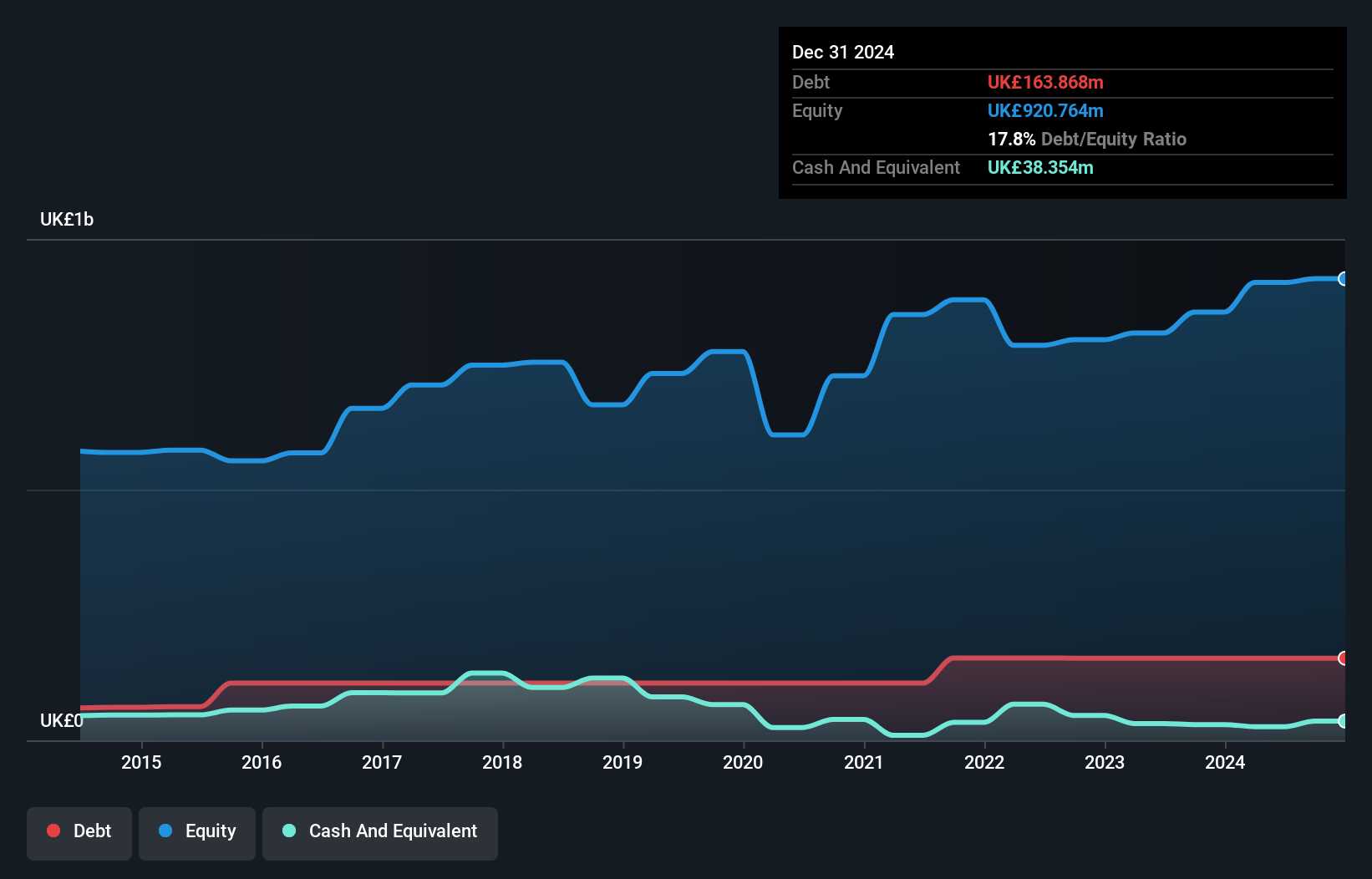

Law Debenture (LSE:LWDB)

Simply Wall St Value Rating: ★★★★☆☆

Overview: The Law Debenture Corporation p.l.c. is an investment trust that offers independent professional services globally to various entities, with a market cap of £1.16 billion.

Operations: Law Debenture generates revenue primarily from its investment portfolio (£35.62 million) and independent professional services (£61.55 million).

Law Debenture, a notable player in the UK market, showcases impressive financial health with high-quality earnings and a satisfactory net debt to equity ratio of 15%. The company's earnings growth over the past year soared by 340.1%, significantly outpacing the Capital Markets industry average of 11.9%. With its price-to-earnings ratio at 8.3x, it presents good value compared to the UK market's 16.3x. Recent performance highlights include a revenue jump to £111.97 million for H1 2024 from £44.02 million last year and net income reaching £82 million, reflecting robust operational strength and strategic positioning in its sector.

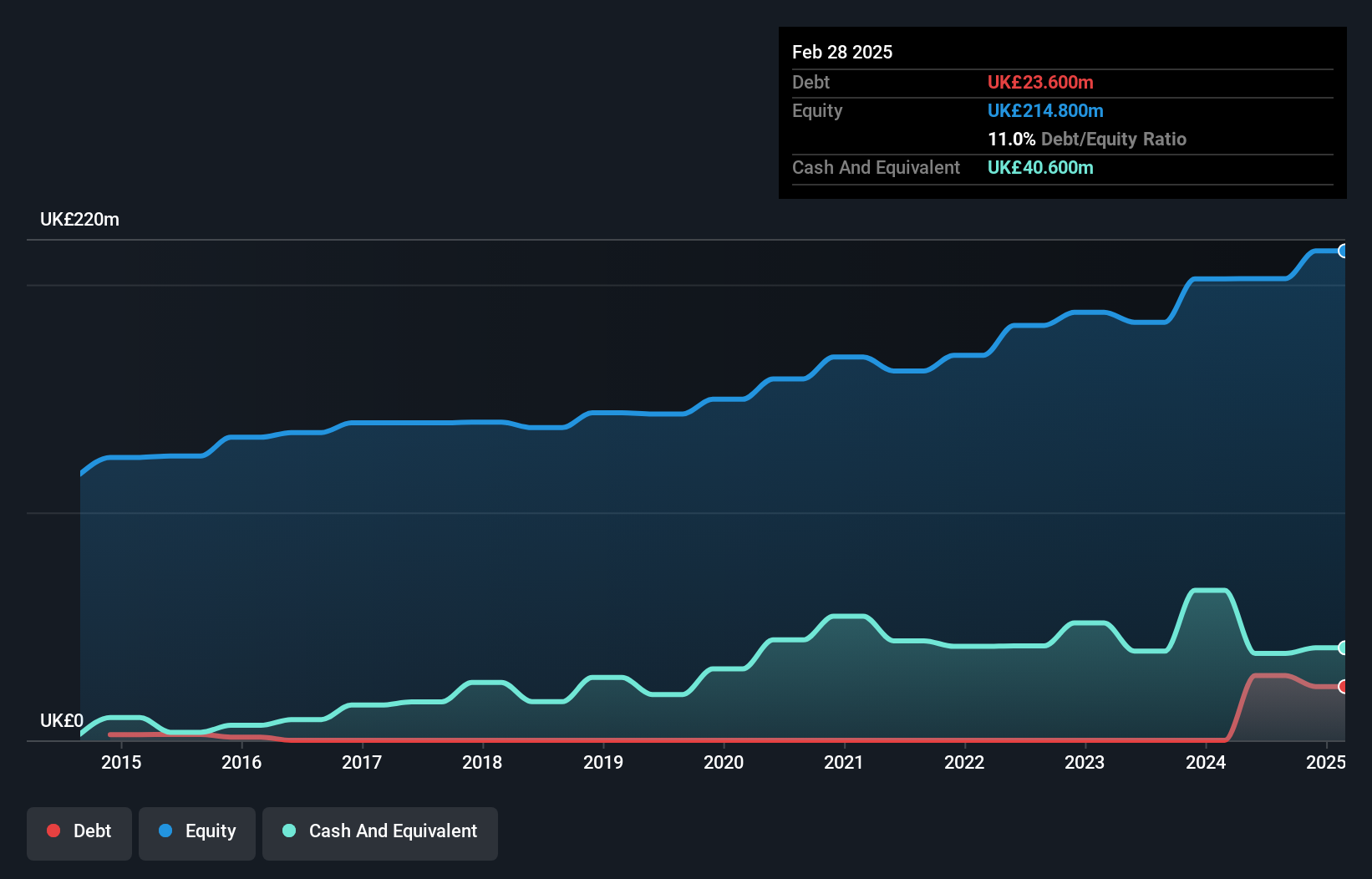

Pinewood Technologies Group (LSE:PINE)

Simply Wall St Value Rating: ★★★★★★

Overview: Pinewood Technologies Group PLC is a cloud-based dealer management software provider serving the automotive industry in the UK and internationally, with a market cap of £276.76 million.

Operations: Pinewood Technologies Group generates revenue primarily from its software segment, which accounted for £22.62 million. The company's market cap is valued at £276.76 million.

Pinewood Technologies Group, a smaller player in the UK tech scene, recently secured a significant 5-year contract with Marshall Motor Group to integrate its systems across 120 dealerships. Despite reporting half-year sales of £16.1 million, up from £11 million last year, net income dropped to £5 million from £26.9 million due to shareholder dilution and negative earnings growth of -81.6%. The company's debt-to-equity ratio has improved significantly over five years from 65.6% to 25.9%, indicating better financial health, while its net debt-to-equity ratio remains satisfactory at 12.7%.

Next Steps

- Access the full spectrum of 81 UK Undiscovered Gems With Strong Fundamentals by clicking on this link.

- Are any of these part of your asset mix? Tap into the analytical power of Simply Wall St's portfolio to get a 360-degree view on how they're shaping up.

- Simply Wall St is a revolutionary app designed for long-term stock investors, it's free and covers every market in the world.

Contemplating Other Strategies?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About LSE:PINE

Pinewood Technologies Group

Operates as a cloud-based dealer management software provider that offers software solutions to the automotive industry in the United Kingdom and internationally.

Flawless balance sheet with high growth potential.

Market Insights

Community Narratives