- United Kingdom

- /

- Metals and Mining

- /

- LSE:HOC

UK Growth Companies With High Insider Ownership September 2024

Reviewed by Simply Wall St

The United Kingdom's stock market has recently experienced turbulence, with the FTSE 100 closing lower amid weak trade data from China and global economic uncertainties. Despite these challenges, growth companies with high insider ownership can offer a sense of stability and potential for long-term success, as insiders often have a vested interest in the company's performance.

Top 10 Growth Companies With High Insider Ownership In The United Kingdom

| Name | Insider Ownership | Earnings Growth |

| Energean (LSE:ENOG) | 10.6% | 30.4% |

| Integrated Diagnostics Holdings (LSE:IDHC) | 27.6% | 23.7% |

| Helios Underwriting (AIM:HUW) | 23.9% | 16.1% |

| Facilities by ADF (AIM:ADF) | 22.7% | 144.7% |

| Judges Scientific (AIM:JDG) | 11.9% | 21.2% |

| Enteq Technologies (AIM:NTQ) | 19.5% | 53.8% |

| B90 Holdings (AIM:B90) | 24.4% | 166.8% |

| Mortgage Advice Bureau (Holdings) (AIM:MAB1) | 19.8% | 29.0% |

| Gulf Keystone Petroleum (LSE:GKP) | 12.1% | 80.6% |

| Belluscura (AIM:BELL) | 36.3% | 133.9% |

Let's take a closer look at a couple of our picks from the screened companies.

Henry Boot (LSE:BOOT)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Henry Boot PLC is a UK-based company involved in property investment and development, land promotion, and construction activities with a market cap of £301.99 million.

Operations: Henry Boot PLC's revenue segments include £87.90 million from construction, £28.37 million from land promotion, and £170.56 million from property investment and development.

Insider Ownership: 31.2%

Earnings Growth Forecast: 25.5% p.a.

Henry Boot, a growth company with high insider ownership in the UK, is forecast to grow earnings by 25.48% annually over the next three years, outpacing the UK market's expected growth of 14.3%. Despite recent half-year earnings showing a drop in sales and net income compared to last year, Henry Boot maintains strong revenue growth prospects at 10.7% per year and continues its progressive dividend policy with a recent increase. The company's property development arm recently completed significant projects and secured planning permissions for future expansions, underscoring its robust development pipeline.

- Click here to discover the nuances of Henry Boot with our detailed analytical future growth report.

- The analysis detailed in our Henry Boot valuation report hints at an inflated share price compared to its estimated value.

Evoke (LSE:EVOK)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Evoke plc, with a market cap of £293.29 million, offers online betting and gaming products and solutions in the United Kingdom, Ireland, Italy, Spain, and internationally through its subsidiaries.

Operations: The company's revenue segments are comprised of Retail (£514 million), UK&I Online (£661.20 million), and International (£516.10 million).

Insider Ownership: 20.5%

Earnings Growth Forecast: 104.9% p.a.

Evoke, trading at 87.8% below its estimated fair value, has seen substantial insider buying in the past three months, indicating confidence from within. Despite a highly volatile share price recently and net losses reported for H1 2024, Evoke's revenue is forecast to grow faster than the UK market at 5.3% annually. The company expects profitability within three years with significant improvement anticipated in H2 2024 due to successful product launches and strategic promotions.

- Dive into the specifics of Evoke here with our thorough growth forecast report.

- According our valuation report, there's an indication that Evoke's share price might be on the cheaper side.

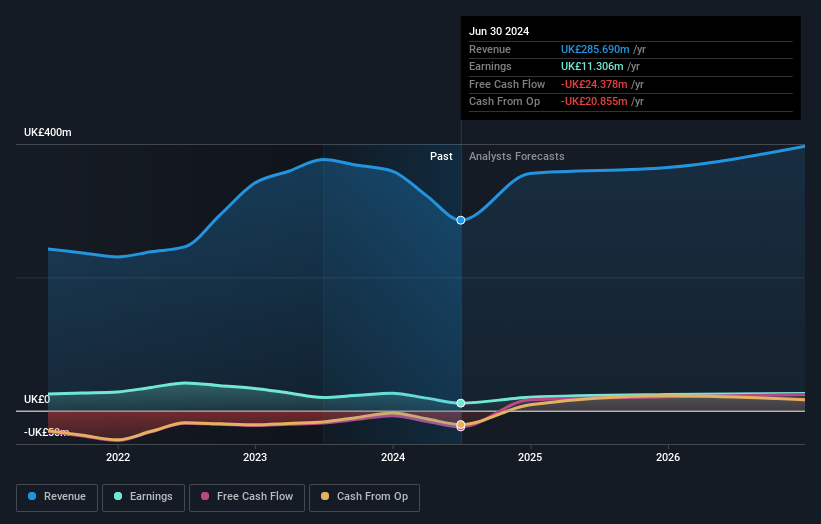

Hochschild Mining (LSE:HOC)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Hochschild Mining plc is a precious metals company involved in the exploration, mining, processing, and sale of gold and silver deposits across Peru, Argentina, the United States, Canada, Brazil, and Chile with a market cap of £1.02 billion.

Operations: Hochschild Mining's revenue segments include $266.70 million from San Jose and $451.91 million from Inmaculada, with a segment adjustment of $79.60 million.

Insider Ownership: 38.4%

Earnings Growth Forecast: 44.6% p.a.

Hochschild Mining, trading at 43.9% below its estimated fair value, has seen no substantial insider trading in the past three months. The company became profitable this year with H1 2024 net income of US$39.52 million compared to a loss last year. Earnings are forecast to grow significantly at 44.6% annually, outpacing the UK market's growth rate, although revenue growth is slower at 5.9%. However, high debt levels and low future return on equity (15.1%) remain concerns.

- Get an in-depth perspective on Hochschild Mining's performance by reading our analyst estimates report here.

- Our comprehensive valuation report raises the possibility that Hochschild Mining is priced higher than what may be justified by its financials.

Taking Advantage

- Embark on your investment journey to our 68 Fast Growing UK Companies With High Insider Ownership selection here.

- Are any of these part of your asset mix? Tap into the analytical power of Simply Wall St's portfolio to get a 360-degree view on how they're shaping up.

- Streamline your investment strategy with Simply Wall St's app for free and benefit from extensive research on stocks across all corners of the world.

Want To Explore Some Alternatives?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

Valuation is complex, but we're here to simplify it.

Discover if Hochschild Mining might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About LSE:HOC

Hochschild Mining

A precious metals company, engages in the exploration, mining, processing, and sale of gold and silver deposits in Peru, Argentina, the United States, Canada, Brazil, and Chile.

Reasonable growth potential and fair value.