Advertisement

The board of Forterra plc (LON:FORT) has announced that it will pay a dividend of £0.019 per share on the 10th of October. Despite this raise, the dividend yield of 1.5% is only a modest boost to shareholder returns.

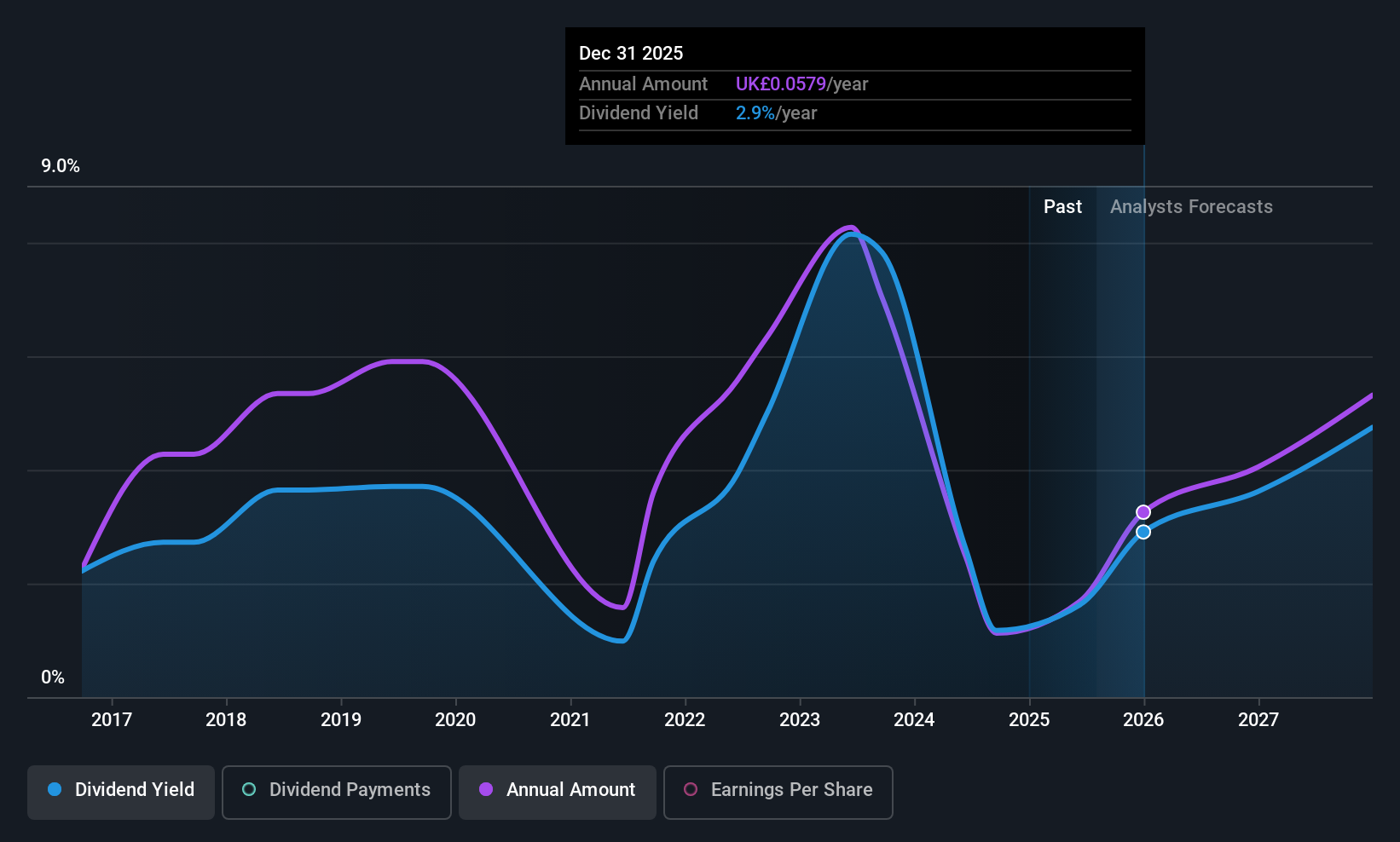

Forterra's Future Dividend Projections Appear Well Covered By Earnings

It would be nice for the yield to be higher, but we should also check if higher levels of dividend payment would be sustainable. Based on the last payment, Forterra was quite comfortably earning enough to cover the dividend. This indicates that a lot of the earnings are being reinvested into the business, with the aim of fueling growth.

The next year is set to see EPS grow by 178.9%. Assuming the dividend continues along recent trends, we think the payout ratio could be 19% by next year, which is in a pretty sustainable range.

See our latest analysis for Forterra

Forterra's Dividend Has Lacked Consistency

Even in its relatively short history, the company has reduced the dividend at least once. This makes us cautious about the consistency of the dividend over a full economic cycle. Since 2016, the annual payment back then was £0.04, compared to the most recent full-year payment of £0.03. Doing the maths, this is a decline of about 3.1% per year. Declining dividends isn't generally what we look for as they can indicate that the company is running into some challenges.

Forterra May Find It Hard To Grow The Dividend

With a relatively unstable dividend, it's even more important to see if earnings per share is growing. Although it's important to note that Forterra's earnings per share has basically not grown from where it was five years ago, which could erode the purchasing power of the dividend over time.

In Summary

In summary, while it's always good to see the dividend being raised, we don't think Forterra's payments are rock solid. In the past, the payments have been unstable, but over the short term the dividend could be reliable, with the company generating enough cash to cover it. We would be a touch cautious of relying on this stock primarily for the dividend income.

Companies possessing a stable dividend policy will likely enjoy greater investor interest than those suffering from a more inconsistent approach. At the same time, there are other factors our readers should be conscious of before pouring capital into a stock. Given that earnings are not growing, the dividend does not look nearly so attractive. See if the 11 analysts are forecasting a turnaround in our free collection of analyst estimates here. Is Forterra not quite the opportunity you were looking for? Why not check out our selection of top dividend stocks.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About LSE:FORT

Forterra

Engages in the manufacturing and sale of building products made from clay and concrete in the United Kingdom.

Flawless balance sheet with solid track record.

Similar Companies

Market Insights

Advertisement

Community Narratives

Finding The True Value Of A Logistics Powerhouse

Fair Value US$95.21|8.7% undervalued

NV

Community Contributor

Paradigm Biopharmaceuticals Will Lead Osteoarthritis Treatment with Zilosul's FDA Success

Fair Value AU$5.50|93.3% undervalued

AM

Community Contributor

Barrick Mining (ABX:CA): A Gold Hedge against a U.S. Shutdown

Fair Value CA$60.00|18.7% undervalued

GM

Community Contributor