- United Kingdom

- /

- Chemicals

- /

- LSE:ESNT

Don't Buy Essentra plc (LON:ESNT) For Its Next Dividend Without Doing These Checks

Regular readers will know that we love our dividends at Simply Wall St, which is why it's exciting to see Essentra plc (LON:ESNT) is about to trade ex-dividend in the next three days. The ex-dividend date occurs one day before the record date which is the day on which shareholders need to be on the company's books in order to receive a dividend. It is important to be aware of the ex-dividend date because any trade on the stock needs to have been settled on or before the record date. Therefore, if you purchase Essentra's shares on or after the 23rd of September, you won't be eligible to receive the dividend, when it is paid on the 29th of October.

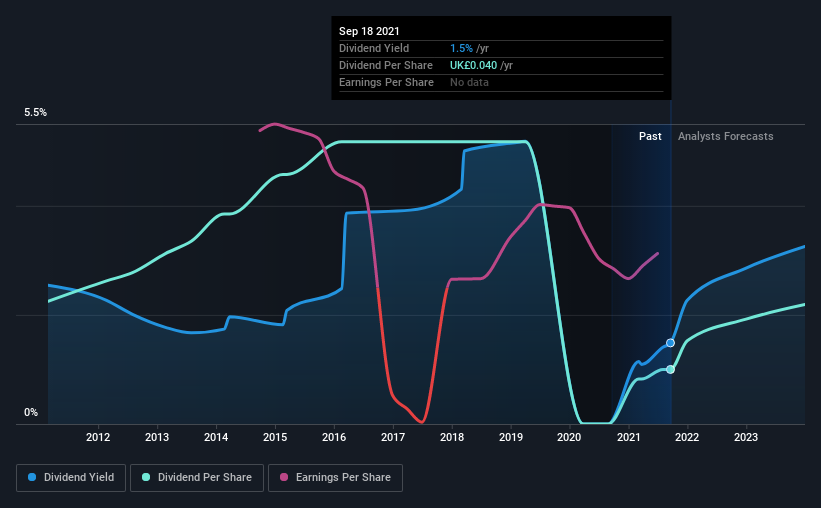

The company's next dividend payment will be UK£0.02 per share, and in the last 12 months, the company paid a total of UK£0.04 per share. Based on the last year's worth of payments, Essentra stock has a trailing yield of around 1.5% on the current share price of £2.69. We love seeing companies pay a dividend, but it's also important to be sure that laying the golden eggs isn't going to kill our golden goose! So we need to investigate whether Essentra can afford its dividend, and if the dividend could grow.

See our latest analysis for Essentra

Dividends are typically paid out of company income, so if a company pays out more than it earned, its dividend is usually at a higher risk of being cut. Its dividend payout ratio is 85% of profit, which means the company is paying out a majority of its earnings. The relatively limited profit reinvestment could slow the rate of future earnings growth. We'd be concerned if earnings began to decline. Yet cash flows are even more important than profits for assessing a dividend, so we need to see if the company generated enough cash to pay its distribution. It paid out 21% of its free cash flow as dividends last year, which is conservatively low.

It's encouraging to see that the dividend is covered by both profit and cash flow. This generally suggests the dividend is sustainable, as long as earnings don't drop precipitously.

Click here to see the company's payout ratio, plus analyst estimates of its future dividends.

Have Earnings And Dividends Been Growing?

When earnings decline, dividend companies become much harder to analyse and own safely. If earnings fall far enough, the company could be forced to cut its dividend. With that in mind, we're discomforted by Essentra's 22% per annum decline in earnings in the past five years. When earnings per share fall, the maximum amount of dividends that can be paid also falls.

Essentra also issued more than 5% of its market cap in new stock during the past year, which we feel is likely to hurt its dividend prospects in the long run. It's hard to grow dividends per share when a company keeps creating new shares.

Another key way to measure a company's dividend prospects is by measuring its historical rate of dividend growth. Essentra's dividend payments per share have declined at 7.8% per year on average over the past 10 years, which is uninspiring. It's never nice to see earnings and dividends falling, but at least management has cut the dividend rather than potentially risk the company's health in an attempt to maintain it.

Final Takeaway

From a dividend perspective, should investors buy or avoid Essentra? We're not enthused by the declining earnings per share, although at least the company's payout ratio is within a reasonable range, meaning it may not be at imminent risk of a dividend cut. Overall, it's hard to get excited about Essentra from a dividend perspective.

If you're not too concerned about Essentra's ability to pay dividends, you should still be mindful of some of the other risks that this business faces. To help with this, we've discovered 4 warning signs for Essentra that you should be aware of before investing in their shares.

We wouldn't recommend just buying the first dividend stock you see, though. Here's a list of interesting dividend stocks with a greater than 2% yield and an upcoming dividend.

If you’re looking to trade Essentra, open an account with the lowest-cost* platform trusted by professionals, Interactive Brokers. Their clients from over 200 countries and territories trade stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

Valuation is complex, but we're here to simplify it.

Discover if Essentra might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About LSE:ESNT

Essentra

Manufactures and distributes plastic injection and vinyl dip moulded, and metal components worldwide.

Excellent balance sheet and good value.

Similar Companies

Market Insights

Community Narratives