Advertisement

Some say volatility, rather than debt, is the best way to think about risk as an investor, but Warren Buffett famously said that 'Volatility is far from synonymous with risk.' It's only natural to consider a company's balance sheet when you examine how risky it is, since debt is often involved when a business collapses. We can see that Versarien plc (LON:VRS) does use debt in its business. But the real question is whether this debt is making the company risky.

Why Does Debt Bring Risk?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. When we examine debt levels, we first consider both cash and debt levels, together.

Check out our latest analysis for Versarien

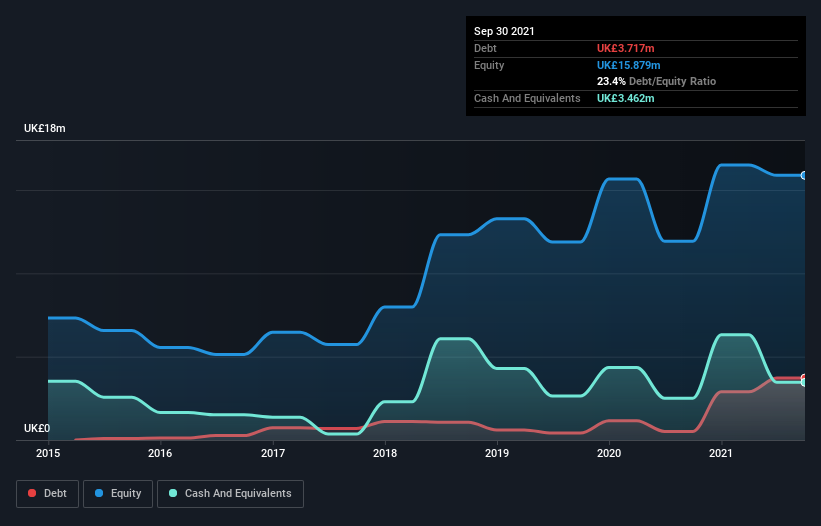

What Is Versarien's Debt?

You can click the graphic below for the historical numbers, but it shows that as of September 2021 Versarien had UK£3.72m of debt, an increase on UK£513.0k, over one year. However, it does have UK£3.46m in cash offsetting this, leading to net debt of about UK£255.0k.

How Healthy Is Versarien's Balance Sheet?

Zooming in on the latest balance sheet data, we can see that Versarien had liabilities of UK£3.95m due within 12 months and liabilities of UK£5.02m due beyond that. Offsetting these obligations, it had cash of UK£3.46m as well as receivables valued at UK£4.39m due within 12 months. So its liabilities outweigh the sum of its cash and (near-term) receivables by UK£1.11m.

Having regard to Versarien's size, it seems that its liquid assets are well balanced with its total liabilities. So while it's hard to imagine that the UK£57.3m company is struggling for cash, we still think it's worth monitoring its balance sheet. Carrying virtually no net debt, Versarien has a very light debt load indeed. The balance sheet is clearly the area to focus on when you are analysing debt. But it is Versarien's earnings that will influence how the balance sheet holds up in the future. So when considering debt, it's definitely worth looking at the earnings trend. Click here for an interactive snapshot.

In the last year Versarien wasn't profitable at an EBIT level, but managed to grow its revenue by 16%, to UK£7.7m. That rate of growth is a bit slow for our taste, but it takes all types to make a world.

Caveat Emptor

Importantly, Versarien had an earnings before interest and tax (EBIT) loss over the last year. Indeed, it lost a very considerable UK£6.2m at the EBIT level. Considering that alongside the liabilities mentioned above does not give us much confidence that company should be using so much debt. So we think its balance sheet is a little strained, though not beyond repair. Another cause for caution is that is bled UK£4.7m in negative free cash flow over the last twelve months. So suffice it to say we consider the stock very risky. When analysing debt levels, the balance sheet is the obvious place to start. But ultimately, every company can contain risks that exist outside of the balance sheet. For example Versarien has 4 warning signs (and 1 which is a bit unpleasant) we think you should know about.

At the end of the day, it's often better to focus on companies that are free from net debt. You can access our special list of such companies (all with a track record of profit growth). It's free.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About AIM:VRS

Versarien

Provides engineering solutions for various industry sectors in the United Kingdom, rest of Europe, North America, and internationally.

Medium-low risk and slightly overvalued.

Similar Companies

Market Insights

Advertisement

Community Narratives

A formidable player in AI and enterprise computing.

Fair Value US$210.00|3.0% undervalued

CO

Community Contributor

IREN's Bold Moves in Sustainable Bitcoin Mining & AI Data Centers

Fair Value US$72.52|20.4% undervalued

BL

Community Contributor

Cooling the Champions: The Aussie Tech Behind F1's Victories

Fair Value AU$12.40|36.8% undervalued

TR

Community Contributor