Advertisement

- United Kingdom

- /

- Insurance

- /

- LSE:SBRE

Sabre Insurance Group (LON:SBRE) Is Paying Out Less In Dividends Than Last Year

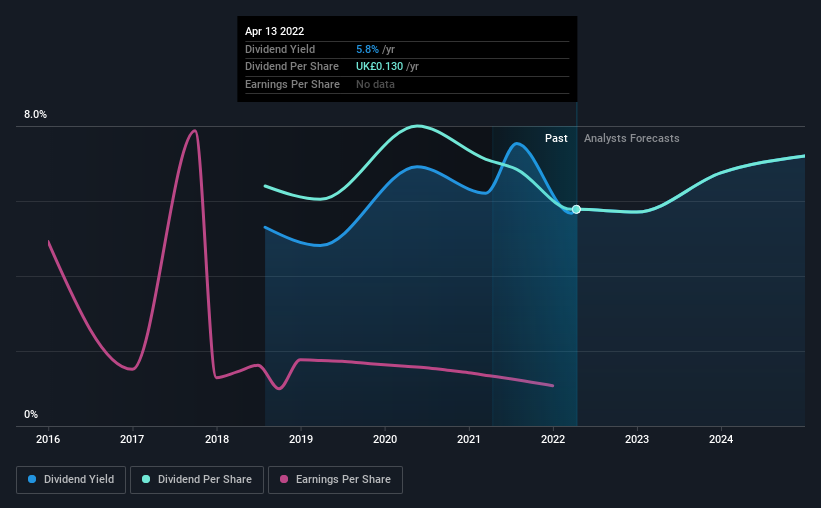

Sabre Insurance Group plc's (LON:SBRE) dividend is being reduced to UK£0.093 on the 1st of June. The dividend yield of 5.8% is still a nice boost to shareholder returns, despite the cut.

View our latest analysis for Sabre Insurance Group

Sabre Insurance Group's Earnings Easily Cover the Distributions

A big dividend yield for a few years doesn't mean much if it can't be sustained. Prior to this announcement, Sabre Insurance Group's dividend was only 69% of earnings, however it was paying out 97% of free cash flows. While the company may be more focused on returning cash to shareholders than growing the business at this time, we think that a cash payout ratio this high might expose the dividend to being cut if the business ran into some challenges.

The next year is set to see EPS grow by 17.7%. If the dividend continues along recent trends, we estimate the payout ratio will be 51%, which is in the range that makes us comfortable with the sustainability of the dividend.

Sabre Insurance Group's Dividend Has Lacked Consistency

Even in its short history, we have seen the dividend cut. The first annual payment during the last 4 years was UK£0.14 in 2018, and the most recent fiscal year payment was UK£0.13. This works out to be a decline of approximately 2.5% per year over that time. Generally, we don't like to see a dividend that has been declining over time as this can degrade shareholders' returns and indicate that the company may be running into problems.

Dividend Growth Is Doubtful

With a relatively unstable dividend, it's even more important to see if earnings per share is growing. It's not great to see that Sabre Insurance Group's earnings per share has fallen at approximately 6.6% per year over the past five years. A modest decline in earnings isn't great, and it makes it quite unlikely that the dividend will grow in the future unless that trend can be reversed. Earnings are forecast to grow over the next 12 months and if that happens we could still be a little bit cautious until it becomes a pattern.

The Dividend Could Prove To Be Unreliable

Overall, it's not great to see that the dividend has been cut, but this might be explained by the payments being a bit high previously. While Sabre Insurance Group is earning enough to cover the payments, the cash flows are lacking. We don't think Sabre Insurance Group is a great stock to add to your portfolio if income is your focus.

Companies possessing a stable dividend policy will likely enjoy greater investor interest than those suffering from a more inconsistent approach. Meanwhile, despite the importance of dividend payments, they are not the only factors our readers should know when assessing a company. Taking the debate a bit further, we've identified 1 warning sign for Sabre Insurance Group that investors need to be conscious of moving forward. Is Sabre Insurance Group not quite the opportunity you were looking for? Why not check out our selection of top dividend stocks.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About LSE:SBRE

Sabre Insurance Group

Through its subsidiaries, engages in writing of general insurance for motor vehicles in the United Kingdom.

Excellent balance sheet with proven track record.

Market Insights

Advertisement

Community Narratives

MicroStrategy: Volatile Gamble or Golden Opportunity?

Fair Value US$663.00|31.9% undervalued

BL

Community Contributor

Emerging Markets and Debt Reduction Will Propel Bath & Body Works Forward

Fair Value US$40.73|22.1% undervalued

ZW

Community Contributor

An amazing opportunity to potentially get a 100 bagger

Fair Value US$10.00|36.0% overvalued

DA

Community Contributor