Stock Analysis

- United Kingdom

- /

- Real Estate

- /

- LSE:HWG

Exploring Undervalued Small Caps With Insider Moves In The United Kingdom July 2024

Reviewed by Simply Wall St

Amidst a backdrop of declining performance in the UK's FTSE 100 and FTSE 250 indices, largely influenced by disappointing trade data from China, investors might find potential opportunities in undervalued small-cap stocks. These smaller companies could present unique advantages, especially when considering insider buying trends which often signal confidence in the company's prospects despite broader market uncertainties.

Top 10 Undervalued Small Caps With Insider Buying In The United Kingdom

| Name | PE | PS | Discount to Fair Value | Value Rating |

|---|---|---|---|---|

| Bytes Technology Group | 25.0x | 5.7x | 0.71% | ★★★★★☆ |

| Ultimate Products | 9.6x | 0.7x | 18.19% | ★★★★★☆ |

| GB Group | NA | 3.1x | 23.39% | ★★★★★☆ |

| THG | NA | 0.4x | 43.56% | ★★★★★☆ |

| Tracsis | 46.7x | 2.7x | 29.16% | ★★★★☆☆ |

| CVS Group | 21.2x | 1.2x | 41.04% | ★★★★☆☆ |

| Hochschild Mining | NA | 1.8x | 47.22% | ★★★★☆☆ |

| Norcros | 8.2x | 0.6x | -16.38% | ★★★☆☆☆ |

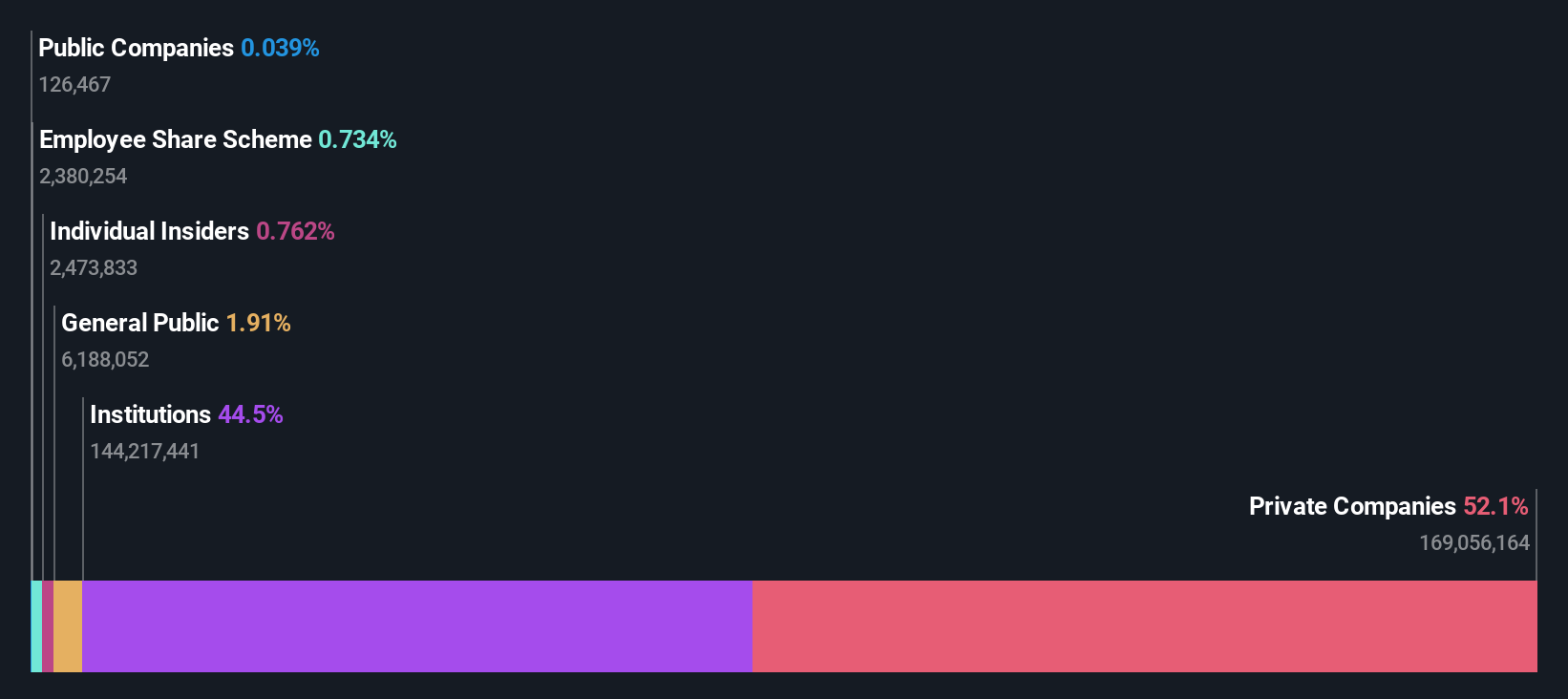

| Harworth Group | 14.9x | 7.8x | -632.24% | ★★★☆☆☆ |

| ASA International Group | 11.5x | 0.7x | 5.06% | ★★★☆☆☆ |

Let's review some notable picks from our screened stocks.

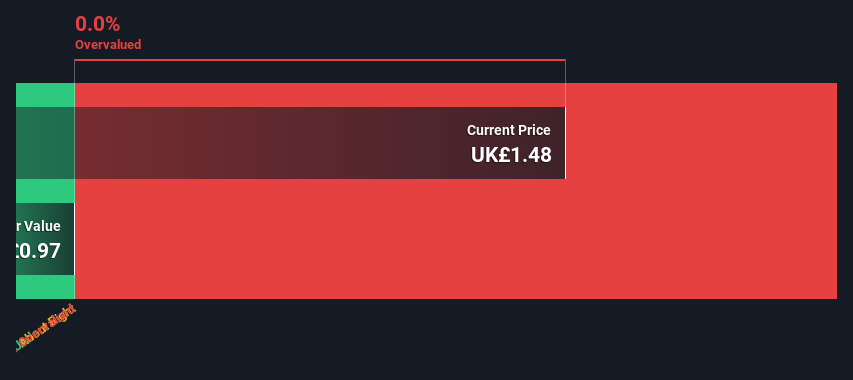

Harworth Group (LSE:HWG)

Simply Wall St Value Rating: ★★★☆☆☆

Overview: Harworth Group is a real estate development company specializing in the regeneration of land and property for sustainable development and investment, with a market capitalization of approximately £397 million.

Operations: Income Generation, Capital Growth from Other Property Activities, and Sales of Development Properties are the primary revenue streams for this entity, generating £23.41 million, £2.29 million, and £46.73 million respectively. The company's gross profit margin has shown variability over recent periods with a notable increase to 0.52% by the end of 2023 from earlier figures around 0.17%, reflecting changes in cost management or revenue mix.

PE: 14.9x

Recently, Harworth Group demonstrated insider confidence as Alastair Lyons acquired 50,000 shares, signaling strong belief in the company's prospects. This move aligns with strategic expansions like the development at Gascoigne Interchange in Leeds, poised to generate significant value with its rail-connected logistics hub. Despite relying solely on external borrowing—a riskier funding method—earnings are expected to climb annually by nearly 26%. This growth potential coupled with leadership enhancements and a commitment to dividend payouts underscores Harworth’s appeal amidst undervalued entities in the UK market.

- Get an in-depth perspective on Harworth Group's performance by reading our valuation report here.

Assess Harworth Group's past performance with our detailed historical performance reports.

Just Group (LSE:JUST)

Simply Wall St Value Rating: ★★★★★★

Overview: Just Group is a financial services company specializing in retirement products and services, with a market capitalization of approximately £0.60 billion.

Operations: The company's gross profit margin has shown significant variability over the observed periods, ranging from as low as 0.029% to a high of 54.28%. Notably, the latest data indicates a substantial increase in gross profit margin to 54.28%, with corresponding revenue of £3.14 billion and gross profit of £1.71 billion for the final reported period.

PE: 9.9x

Just Group, reflecting a strategic confidence boost, saw insiders recently purchasing shares, underscoring their belief in the company's prospects despite its reliance on external borrowing—a higher risk funding strategy. With earnings expected to rise nearly 10% annually, this financial entity also pleased shareholders by declaring a dividend of 1.50 pence per share at its latest AGM. These actions suggest a resilient trajectory for Just Group amidst the competitive landscape of undervalued entities in the UK market.

- Click here to discover the nuances of Just Group with our detailed analytical valuation report.

Understand Just Group's track record by examining our Past report.

Norcros (LSE:NXR)

Simply Wall St Value Rating: ★★★☆☆☆

Overview: Norcros is a company that specializes in building products, operating with a market capitalization of approximately £392.10 million.

Operations: Building Products generated £392.10 million in revenue, with a notable gross profit margin consistently at 100% over several periods, reflecting the absence of COGS (Cost of Goods Sold) in these calculations. The company's operating expenses have been substantial, impacting net income which showed variability across the observed periods.

PE: 8.2x

With a notable increase in net income from GBP 16.8 million to GBP 26.8 million year-over-year and a solid sales figure of GBP 392.1 million, Norcros has demonstrated financial resilience despite a slight revenue dip from the previous year's GBP 441 million. Recently, insider confidence was bolstered as they purchased shares, signaling trust in the company's future prospects amid forecasts of a modest earnings decline over the next three years. Adding to its appeal, Norcros maintains a consistent dividend payout with an upcoming final dividend set for early August, underpinned by strategic priorities focused on organic growth and operational excellence announced at their latest Capital Markets Event.

- Delve into the full analysis valuation report here for a deeper understanding of Norcros.

Gain insights into Norcros' past trends and performance with our Past report.

Make It Happen

- Delve into our full catalog of 25 Undervalued UK Small Caps With Insider Buying here.

- Have a stake in these businesses? Integrate your holdings into Simply Wall St's portfolio for notifications and detailed stock reports.

- Enhance your investing ability with the Simply Wall St app and enjoy free access to essential market intelligence spanning every continent.

Looking For Alternative Opportunities?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're helping make it simple.

Find out whether Harworth Group is potentially over or undervalued by checking out our comprehensive analysis, which includes fair value estimates, risks and warnings, dividends, insider transactions and financial health.

View the Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About LSE:HWG

Harworth Group

Operates as a land and property regeneration company in the North of England and the Midlands.

Reasonable growth potential with adequate balance sheet.