Advertisement

- United Kingdom

- /

- Insurance

- /

- LSE:BEZ

We Ran A Stock Scan For Earnings Growth And Beazley (LON:BEZ) Passed With Ease

It's common for many investors, especially those who are inexperienced, to buy shares in companies with a good story even if these companies are loss-making. But as Peter Lynch said in One Up On Wall Street, 'Long shots almost never pay off.' Loss making companies can act like a sponge for capital - so investors should be cautious that they're not throwing good money after bad.

Despite being in the age of tech-stock blue-sky investing, many investors still adopt a more traditional strategy; buying shares in profitable companies like Beazley (LON:BEZ). While this doesn't necessarily speak to whether it's undervalued, the profitability of the business is enough to warrant some appreciation - especially if its growing.

View our latest analysis for Beazley

How Fast Is Beazley Growing Its Earnings Per Share?

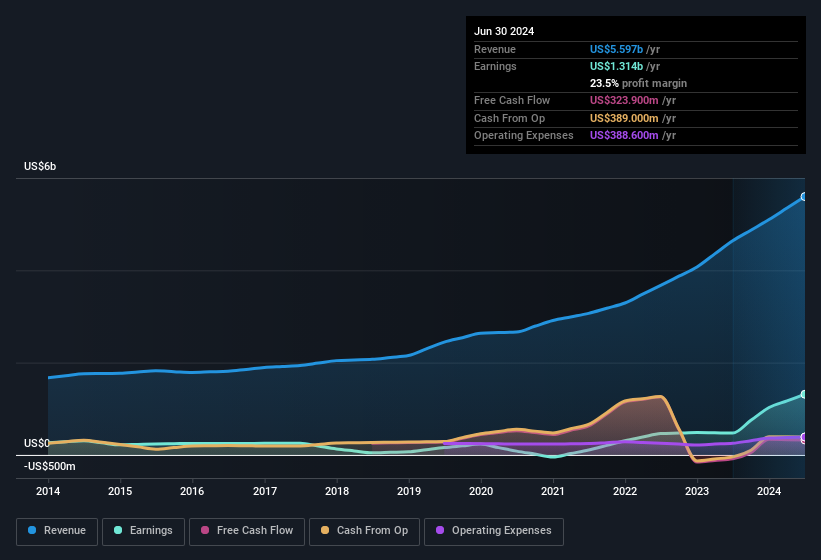

In the last three years Beazley's earnings per share took off; so much so that it's a bit disingenuous to use these figures to try and deduce long term estimates. As a result, we'll zoom in on growth over the last year, instead. Impressively, Beazley's EPS catapulted from US$0.74 to US$2.09, over the last year. It's not often a company can achieve year-on-year growth of 183%.

One way to double-check a company's growth is to look at how its revenue, and earnings before interest and tax (EBIT) margins are changing. It's noted that Beazley's revenue from operations was lower than its revenue in the last twelve months, so that could distort our analysis of its margins. The good news is that Beazley is growing revenues, and EBIT margins improved by 17.4 percentage points to 37%, over the last year. That's great to see, on both counts.

In the chart below, you can see how the company has grown earnings and revenue, over time. Click on the chart to see the exact numbers.

You don't drive with your eyes on the rear-view mirror, so you might be more interested in this free report showing analyst forecasts for Beazley's future profits.

Are Beazley Insiders Aligned With All Shareholders?

Insider interest in a company always sparks a bit of intrigue and many investors are on the lookout for companies where insiders are putting their money where their mouth is. That's because insider buying often indicates that those closest to the company have confidence that the share price will perform well. Of course, we can never be sure what insiders are thinking, we can only judge their actions.

The good news for Beazley shareholders is that no insiders reported selling shares in the last year. So it's definitely nice that Independent Non-Executive Director Anthony Reizenstein bought US$37k worth of shares at an average price of around US$7.36. It seems that at least one insider is prepared to show the market there is potential within Beazley.

The good news, alongside the insider buying, for Beazley bulls is that insiders (collectively) have a meaningful investment in the stock. To be specific, they have US$12m worth of shares. This considerable investment should help drive long-term value in the business. Even though that's only about 0.2% of the company, it's enough money to indicate alignment between the leaders of the business and ordinary shareholders.

Is Beazley Worth Keeping An Eye On?

Beazley's earnings have taken off in quite an impressive fashion. The icing on the cake is that insiders own a large chunk of the company and one has even been buying more shares. These factors seem to indicate the company's potential and that it has reached an inflection point. We'd suggest Beazley belongs near the top of your watchlist. Don't forget that there may still be risks. For instance, we've identified 1 warning sign for Beazley that you should be aware of.

Keen growth investors love to see insider activity. Thankfully, Beazley isn't the only one. You can see a a curated list of British companies which have exhibited consistent growth accompanied by high insider ownership.

Please note the insider transactions discussed in this article refer to reportable transactions in the relevant jurisdiction.

Valuation is complex, but we're here to simplify it.

Discover if Beazley might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About LSE:BEZ

Beazley

Provides risk insurance and reinsurance solutions in the United States, the United Kingdom, rest of Europe, and internationally.

Flawless balance sheet and undervalued.

Similar Companies

Market Insights

Advertisement

Community Narratives

BMW cruising ahead with new EVs and premium models to boost revenue 5%

Fair Value €135.07|44.6% undervalued

UN

Community Contributor

EU#2 - From Humble Beginnings to Global Powerhouse

Fair Value DKK 851.04|46.2% undervalued

TO

Community Contributor