Advertisement

- United Kingdom

- /

- Insurance

- /

- LSE:BEZ

How Does Beazley's (LON:BEZ) CEO Pay Compare With Company Performance?

This article will reflect on the compensation paid to David Horton who has served as CEO of Beazley plc (LON:BEZ) since 2008. This analysis will also look to assess whether the CEO is appropriately paid, considering recent earnings growth and investor returns for Beazley.

View our latest analysis for Beazley

Comparing Beazley plc's CEO Compensation With the industry

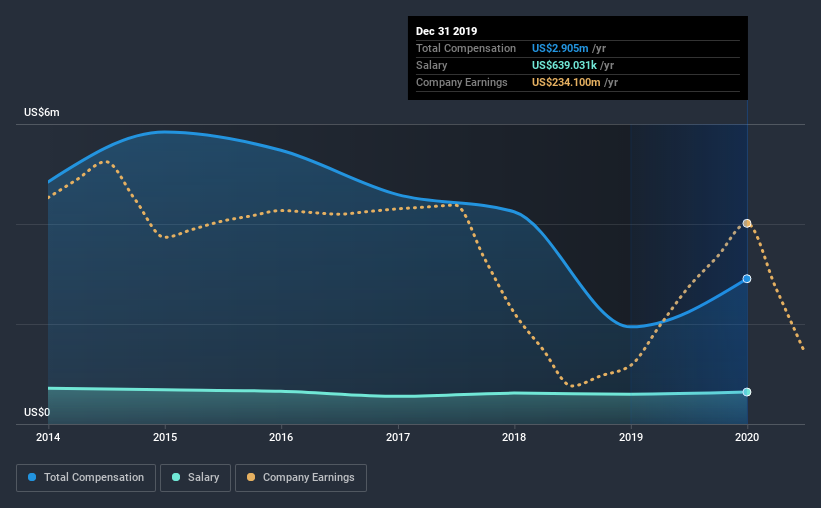

According to our data, Beazley plc has a market capitalization of UK£2.2b, and paid its CEO total annual compensation worth UK£2.9m over the year to December 2019. We note that's an increase of 49% above last year. While we always look at total compensation first, our analysis shows that the salary component is less, at UK£639k.

For comparison, other companies in the same industry with market capitalizations ranging between UK£1.5b and UK£4.7b had a median total CEO compensation of UK£1.9m. Hence, we can conclude that David Horton is remunerated higher than the industry median. Moreover, David Horton also holds UK£7.1m worth of Beazley stock directly under their own name, which reveals to us that they have a significant personal stake in the company.

| Component | 2019 | 2018 | Proportion (2019) |

| Salary | UK£639k | UK£597k | 22% |

| Other | UK£2.3m | UK£1.3m | 78% |

| Total Compensation | UK£2.9m | UK£1.9m | 100% |

On an industry level, roughly 37% of total compensation represents salary and 63% is other remuneration. It's interesting to note that Beazley allocates a smaller portion of compensation to salary in comparison to the broader industry. If non-salary compensation dominates total pay, it's an indicator that the executive's salary is tied to company performance.

A Look at Beazley plc's Growth Numbers

Beazley plc has reduced its earnings per share by 33% a year over the last three years. It achieved revenue growth of 8.9% over the last year.

The decline in EPS is a bit concerning. The fairly low revenue growth fails to impress given that the EPS is down. These factors suggest that the business performance wouldn't really justify a high pay packet for the CEO. Moving away from current form for a second, it could be important to check this free visual depiction of what analysts expect for the future.

Has Beazley plc Been A Good Investment?

With a three year total loss of 19% for the shareholders, Beazley plc would certainly have some dissatisfied shareholders. So shareholders would probably want the company to be lessto generous with CEO compensation.

To Conclude...

As we touched on above, Beazley plc is currently paying its CEO higher than the median pay for CEOs of companies belonging to the same industry and with similar market capitalizations. This doesn't look good against shareholder returns, which have been negative for the past three years. To make matters worse, EPS growth has also been negative during this period. Overall, with such poor performance, shareholder's would probably have questions if the company decided to give the CEO a raise.

While it is important to pay attention to CEO remuneration, investors should also consider other elements of the business. That's why we did some digging and identified 2 warning signs for Beazley that you should be aware of before investing.

Arguably, business quality is much more important than CEO compensation levels. So check out this free list of interesting companies that have HIGH return on equity and low debt.

When trading Beazley or any other investment, use the platform considered by many to be the Professional's Gateway to the Worlds Market, Interactive Brokers. You get the lowest-cost* trading on stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

Valuation is complex, but we're here to simplify it.

Discover if Beazley might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com.

About LSE:BEZ

Beazley

Provides risk insurance and reinsurance solutions in the United States, the United Kingdom, rest of Europe, and internationally.

Very undervalued with flawless balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

100% Patient Improvement in trial puts this $16M Biotech on the radar

Fair Value US$5.30|65.7% undervalued

JO

Community Contributor

Exxon Mobil's 17.5% Upside Promises Industry-Leading Returns in Energy Transition

Fair Value US$132.00|14.9% undervalued

HE

Community Contributor

NHC Analysis: Quality at a Good Price. A Golden Opportunity?

Fair Value US$179.80|35.4% undervalued

DA

Community Contributor

Product Refresh And Global Expansion Will Empower Future Market Leadership

Fair Value US$202.60|21.0% undervalued

AN

Based on Analyst Price Targets