- United Kingdom

- /

- Insurance

- /

- AIM:HUW

We Wouldn't Be Too Quick To Buy Helios Underwriting plc (LON:HUW) Before It Goes Ex-Dividend

Readers hoping to buy Helios Underwriting plc (LON:HUW) for its dividend will need to make their move shortly, as the stock is about to trade ex-dividend. The ex-dividend date occurs one day before the record date which is the day on which shareholders need to be on the company's books in order to receive a dividend. The ex-dividend date is important because any transaction on a stock needs to have been settled before the record date in order to be eligible for a dividend. Therefore, if you purchase Helios Underwriting's shares on or after the 6th of June, you won't be eligible to receive the dividend, when it is paid on the 12th of July.

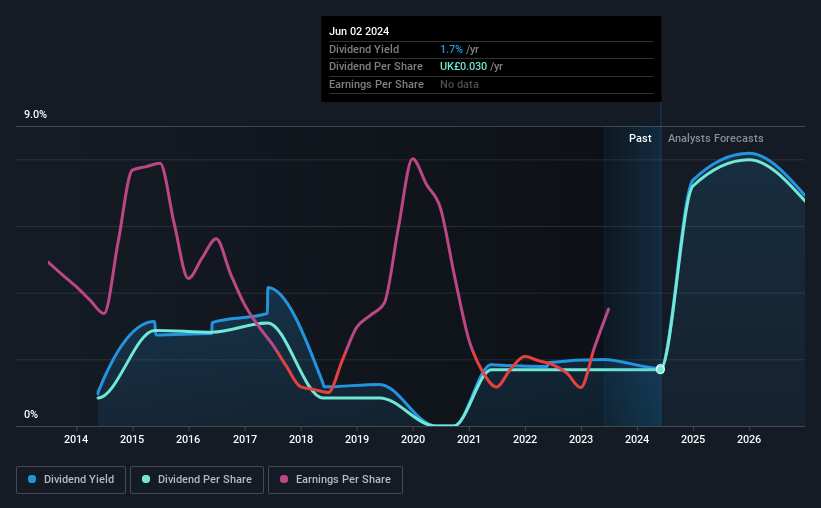

The company's next dividend payment will be UK£0.06 per share, and in the last 12 months, the company paid a total of UK£0.03 per share. Looking at the last 12 months of distributions, Helios Underwriting has a trailing yield of approximately 1.7% on its current stock price of UK£1.735. Dividends are an important source of income to many shareholders, but the health of the business is crucial to maintaining those dividends. That's why we should always check whether the dividend payments appear sustainable, and if the company is growing.

See our latest analysis for Helios Underwriting

Dividends are usually paid out of company profits, so if a company pays out more than it earned then its dividend is usually at greater risk of being cut. Helios Underwriting paid out 54% of its earnings to investors last year, a normal payout level for most businesses.

Companies that pay out less in dividends than they earn in profits generally have more sustainable dividends. The lower the payout ratio, the more wiggle room the business has before it could be forced to cut the dividend.

Click here to see how much of its profit Helios Underwriting paid out over the last 12 months.

Have Earnings And Dividends Been Growing?

Companies with falling earnings are riskier for dividend shareholders. If business enters a downturn and the dividend is cut, the company could see its value fall precipitously. With that in mind, we're discomforted by Helios Underwriting's 28% per annum decline in earnings in the past five years. When earnings per share fall, the maximum amount of dividends that can be paid also falls.

We'd also point out that Helios Underwriting issued a meaningful number of new shares in the past year. Trying to grow the dividend while issuing large amounts of new shares reminds us of the ancient Greek tale of Sisyphus - perpetually pushing a boulder uphill.

Another key way to measure a company's dividend prospects is by measuring its historical rate of dividend growth. In the past 10 years, Helios Underwriting has increased its dividend at approximately 7.2% a year on average. Growing the dividend payout ratio while earnings are declining can deliver nice returns for a while, but it's always worth checking for when the company can't increase the payout ratio any more - because then the music stops.

Final Takeaway

Is Helios Underwriting worth buying for its dividend? We're not overly enthused to see Helios Underwriting's earnings in retreat at the same time as the company is paying out more than half of its earnings as dividends to shareholders. All things considered, we're not optimistic about its dividend prospects, and would be inclined to leave it on the shelf for now.

Although, if you're still interested in Helios Underwriting and want to know more, you'll find it very useful to know what risks this stock faces. Our analysis shows 1 warning sign for Helios Underwriting and you should be aware of it before buying any shares.

If you're in the market for strong dividend payers, we recommend checking our selection of top dividend stocks.

Valuation is complex, but we're here to simplify it.

Discover if Helios Underwriting might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About AIM:HUW

Helios Underwriting

Provides a limited liability investment for its shareholders in the Lloyd’s insurance market in the United Kingdom.

Solid track record with excellent balance sheet.

Similar Companies

Market Insights

Community Narratives