Advertisement

- United Kingdom

- /

- Food

- /

- LSE:CARR

Carr's Group plc (LON:CARR) Stock Rockets 26% But Many Are Still Ignoring The Company

Carr's Group plc (LON:CARR) shares have had a really impressive month, gaining 26% after a shaky period beforehand. Unfortunately, despite the strong performance over the last month, the full year gain of 2.5% isn't as attractive.

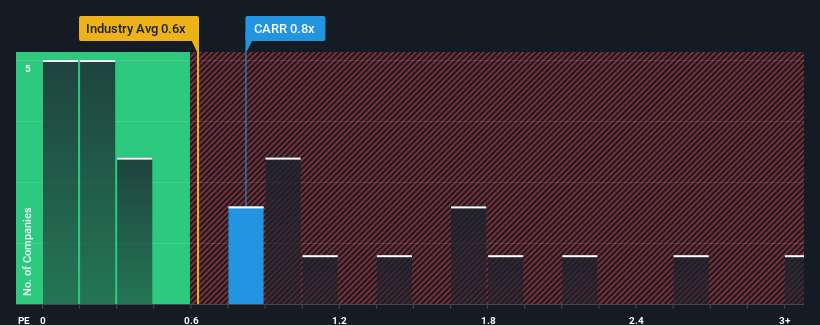

Even after such a large jump in price, there still wouldn't be many who think Carr's Group's price-to-sales (or "P/S") ratio of 0.8x is worth a mention when the median P/S in the United Kingdom's Food industry is similar at about 0.6x. Although, it's not wise to simply ignore the P/S without explanation as investors may be disregarding a distinct opportunity or a costly mistake.

View our latest analysis for Carr's Group

What Does Carr's Group's Recent Performance Look Like?

With revenue growth that's superior to most other companies of late, Carr's Group has been doing relatively well. Perhaps the market is expecting this level of performance to taper off, keeping the P/S from soaring. If you like the company, you'd be hoping this isn't the case so that you could potentially pick up some stock while it's not quite in favour.

Keen to find out how analysts think Carr's Group's future stacks up against the industry? In that case, our free report is a great place to start.Is There Some Revenue Growth Forecasted For Carr's Group?

There's an inherent assumption that a company should be matching the industry for P/S ratios like Carr's Group's to be considered reasonable.

Taking a look back first, we see that the company grew revenue by an impressive 16% last year. However, this wasn't enough as the latest three year period has seen the company endure a nasty 64% drop in revenue in aggregate. So unfortunately, we have to acknowledge that the company has not done a great job of growing revenues over that time.

Turning to the outlook, the next year should generate growth of 6.5% as estimated by the three analysts watching the company. Meanwhile, the rest of the industry is forecast to only expand by 4.3%, which is noticeably less attractive.

With this in consideration, we find it intriguing that Carr's Group's P/S is closely matching its industry peers. Apparently some shareholders are skeptical of the forecasts and have been accepting lower selling prices.

The Bottom Line On Carr's Group's P/S

Its shares have lifted substantially and now Carr's Group's P/S is back within range of the industry median. We'd say the price-to-sales ratio's power isn't primarily as a valuation instrument but rather to gauge current investor sentiment and future expectations.

Despite enticing revenue growth figures that outpace the industry, Carr's Group's P/S isn't quite what we'd expect. When we see a strong revenue outlook, with growth outpacing the industry, we can only assume potential uncertainty around these figures are what might be placing slight pressure on the P/S ratio. At least the risk of a price drop looks to be subdued, but investors seem to think future revenue could see some volatility.

And what about other risks? Every company has them, and we've spotted 2 warning signs for Carr's Group (of which 1 is a bit unpleasant!) you should know about.

If these risks are making you reconsider your opinion on Carr's Group, explore our interactive list of high quality stocks to get an idea of what else is out there.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About LSE:CARR

Fevara

Engages in the agriculture business in the United Kingdom and internationally.

Excellent balance sheet and fair value.

Market Insights

Advertisement

Community Narratives

The Next Phase of Energy Storage: How NeoVolta Is Tackling America’s Power Crunch

Fair Value US$7.50|30.4% undervalued

MA

Community Contributor

Why EnSilica is Worth Possibly 13x its Current Price

Fair Value UK£5.00|89.5% undervalued

DO

Community Contributor

M&A Activity, Industry Diversification & A Defense Contract Monopoly Will Push BWXT For Healthy Long-Term Growth

Fair Value US$220.00|13.0% undervalued

CL

Community Contributor

A case for Cassiar Gold Corp (TSXV: GLDC) to reach CAD$8-10 before 2030 (X30-37)

Fair Value CA$10.00|96.5% undervalued

AG

Community Contributor