Advertisement

- United Kingdom

- /

- Tobacco

- /

- LSE:BATS

This Is Why British American Tobacco p.l.c.'s (LON:BATS) CEO Compensation Looks Appropriate

Key Insights

- British American Tobacco's Annual General Meeting to take place on 16th of April

- Salary of UK£1.37m is part of CEO Tadeu Marroco's total remuneration

- Total compensation is similar to the industry average

- British American Tobacco's total shareholder return over the past three years was 23% while its EPS was down 23% over the past three years

Despite positive share price growth of 23% for British American Tobacco p.l.c. (LON:BATS) over the last few years, earnings growth has been disappointing, which suggests something is amiss. The upcoming AGM on 16th of April may be an opportunity for shareholders to bring up any concerns they may have for the board’s attention. They will be able to influence managerial decisions through the exercise of their voting power on resolutions, such as CEO remuneration and other matters, which may influence future company prospects. From what we gathered, we think shareholders should be wary of raising CEO compensation until the company shows some marked improvement.

Check out our latest analysis for British American Tobacco

How Does Total Compensation For Tadeu Marroco Compare With Other Companies In The Industry?

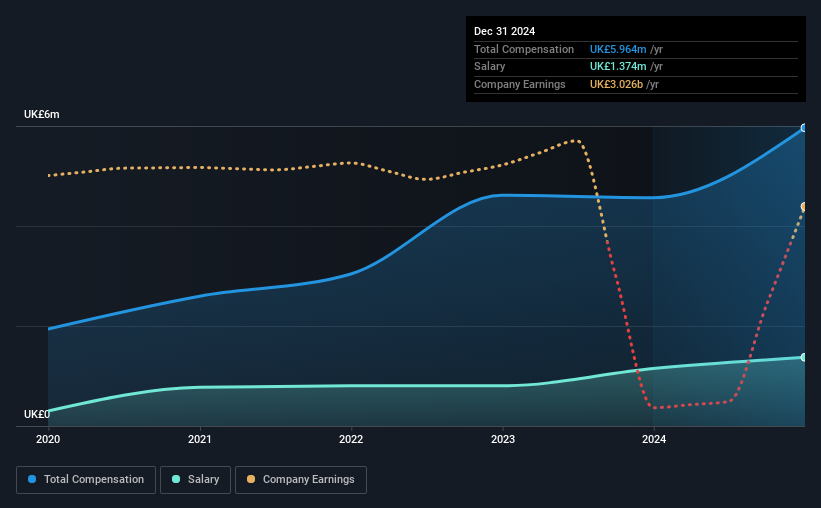

According to our data, British American Tobacco p.l.c. has a market capitalization of UK£69b, and paid its CEO total annual compensation worth UK£6.0m over the year to December 2024. That's a notable increase of 31% on last year. While this analysis focuses on total compensation, it's worth acknowledging that the salary portion is lower, valued at UK£1.4m.

In comparison with other companies in the the United Kingdom Tobacco industry with market capitalizations over UK£6.3b, the reported median total CEO compensation was UK£4.6m. So it looks like British American Tobacco compensates Tadeu Marroco in line with the median for the industry. What's more, Tadeu Marroco holds UK£5.7m worth of shares in the company in their own name, indicating that they have a lot of skin in the game.

| Component | 2024 | 2023 | Proportion (2024) |

| Salary | UK£1.4m | UK£1.1m | 23% |

| Other | UK£4.6m | UK£3.4m | 77% |

| Total Compensation | UK£6.0m | UK£4.6m | 100% |

Talking in terms of the industry, salary represented approximately 31% of total compensation out of all the companies we analyzed, while other remuneration made up 69% of the pie. British American Tobacco sets aside a smaller share of compensation for salary, in comparison to the overall industry. If total compensation is slanted towards non-salary benefits, it indicates that CEO pay is linked to company performance.

British American Tobacco p.l.c.'s Growth

Over the last three years, British American Tobacco p.l.c. has shrunk its earnings per share by 23% per year. In the last year, its revenue is down 5.2%.

The decline in EPS is a bit concerning. And the fact that revenue is down year on year arguably paints an ugly picture. These factors suggest that the business performance wouldn't really justify a high pay packet for the CEO. Looking ahead, you might want to check this free visual report on analyst forecasts for the company's future earnings. .

Has British American Tobacco p.l.c. Been A Good Investment?

British American Tobacco p.l.c. has generated a total shareholder return of 23% over three years, so most shareholders would be reasonably content. But they would probably prefer not to see CEO compensation far in excess of the median.

In Summary...

Shareholder returns, while positive, should be looked at along with earnings, which have not grown at all recently. This makes us think the share price momentum may slow in the future. In the upcoming AGM, shareholders will get the opportunity to discuss any concerns with the board, including those related to CEO remuneration and assess if the board's plan will likely improve performance in the future.

CEO compensation can have a massive impact on performance, but it's just one element. We've identified 4 warning signs for British American Tobacco that investors should be aware of in a dynamic business environment.

Switching gears from British American Tobacco, if you're hunting for a pristine balance sheet and premium returns, this free list of high return, low debt companies is a great place to look.

Valuation is complex, but we're here to simplify it.

Discover if British American Tobacco might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About LSE:BATS

British American Tobacco

Provides tobacco and nicotine products to consumers in the Americas, Europe, the Asia-Pacific, the Middle East, Africa, and the United States.

Second-rate dividend payer with low risk.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.7% overvalued

TI

Community Contributor

Recently Updated Narratives

CO

composite32 on Astor Enerji ·

Astor Enerji will surge with a fair value of $140.43 in the next 3 years

Fair Value:₺140.4335.5% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RE

RecMag on Proximus ·

Proximus: The State-Backed Backup Plan with 7% Gross Yield and 15% Currency Upside.

Fair Value:€17.1356.7% undervalued

29 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AG

Agricola on IMPACT Silver ·

A case for for IMPACT Silver Corp (TSXV:IPT) to reach USD $4.52 (CAD $6.16) in 2026 (23 bagger in 1 year) and USD $5.76 (CAD $7.89) by 2030

Fair Value:CA$7.8996.2% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

101 followersusers have followed this narrative

10 commentsusers have commented on this narrative

20 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.8% undervalued

137 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3929.3% undervalued

929 followersusers have followed this narrative

6 commentsusers have commented on this narrative

22 likesusers have liked this narrative