Advertisement

- United Kingdom

- /

- Oil and Gas

- /

- LSE:ITH

The Ithaca Energy plc (LON:ITH) Analysts Have Been Trimming Their Sales Forecasts

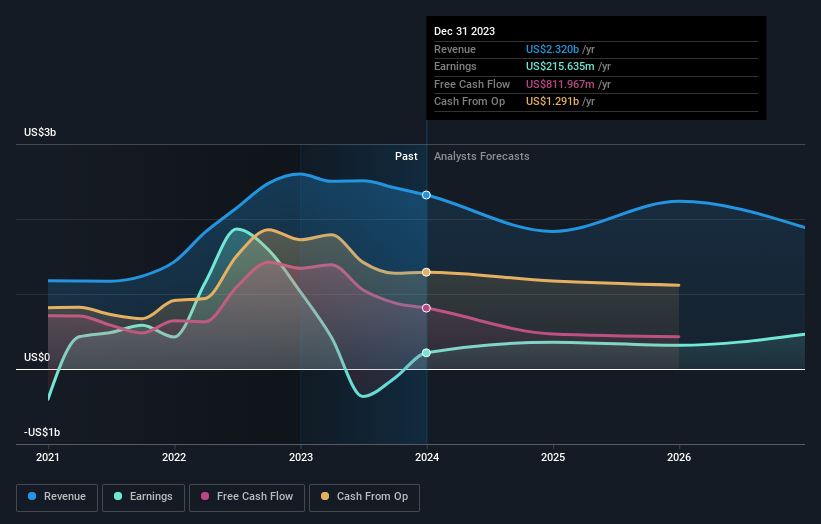

The latest analyst coverage could presage a bad day for Ithaca Energy plc (LON:ITH), with the analysts making across-the-board cuts to their statutory estimates that might leave shareholders a little shell-shocked. This report focused on revenue estimates, and it looks as though the consensus view of the business has become substantially more conservative.

After the downgrade, the consensus from Ithaca Energy's five analysts is for revenues of US$1.8b in 2024, which would reflect a disturbing 21% decline in sales compared to the last year of performance. Per-share earnings are expected to soar 64% to US$0.35. Prior to this update, the analysts had been forecasting revenues of US$2.1b and earnings per share (EPS) of US$0.42 in 2024. Indeed, we can see that the analysts are a lot more bearish about Ithaca Energy's prospects, administering a measurable cut to revenue estimates and slashing their EPS estimates to boot.

View our latest analysis for Ithaca Energy

Looking at the bigger picture now, one of the ways we can make sense of these forecasts is to see how they measure up against both past performance and industry growth estimates. We would highlight that sales are expected to reverse, with a forecast 21% annualised revenue decline to the end of 2024. That is a notable change from historical growth of 36% over the last five years. By contrast, our data suggests that other companies (with analyst coverage) in the industry are forecast to see their revenue decline 1.5% annually for the foreseeable future. The forecasts do look bearish for Ithaca Energy, since they're expecting it to shrink faster than the industry.

The Bottom Line

The biggest issue in the new estimates is that analysts have reduced their earnings per share estimates, suggesting business headwinds lay ahead for Ithaca Energy. Unfortunately they also downgraded their revenue estimates, and our aggregation of analyst estimates suggests that Ithaca Energy revenue is expected to perform worse than the wider market. Given the stark change in sentiment, we'd understand if investors became more cautious on Ithaca Energy after today.

With that said, the long-term trajectory of the company's earnings is a lot more important than next year. At Simply Wall St, we have a full range of analyst estimates for Ithaca Energy going out to 2026, and you can see them free on our platform here.

Of course, seeing company management invest large sums of money in a stock can be just as useful as knowing whether analysts are downgrading their estimates. So you may also wish to search this free list of stocks that insiders are buying.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About LSE:ITH

Ithaca Energy

Engages in the development and production of oil and gas in the North Sea.

Adequate balance sheet with moderate growth potential.

Similar Companies

Market Insights

Advertisement

Community Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|11.0% undervalued

BE

Community Contributor

Procter & Gamble: A Dividend Giant Facing Slowing Growth

Fair Value US$119.81|23.3% overvalued

AN

Community Contributor

Eli Lilly's Future Growth Driven by Tirzepatide and Favorable Market Conditions

Fair Value US$1.19k|13.8% undervalued

EA

Community Contributor