Stock Analysis

- United Kingdom

- /

- Oil and Gas

- /

- LSE:GKP

UK Growth Companies With High Insider Ownership In June 2024

Reviewed by Simply Wall St

The United Kingdom market has shown robust growth, with a 7.4% increase over the past year and earnings expected to grow by 13% annually. In this context, companies with high insider ownership can be particularly compelling, as they often signal strong confidence in the company's future from those who know it best.

Top 10 Growth Companies With High Insider Ownership In The United Kingdom

| Name | Insider Ownership | Earnings Growth |

| Plant Health Care (AIM:PHC) | 26.4% | 121.3% |

| Petrofac (LSE:PFC) | 16.6% | 124.5% |

| Gulf Keystone Petroleum (LSE:GKP) | 10.8% | 47.6% |

| Integrated Diagnostics Holdings (LSE:IDHC) | 26.7% | 25.5% |

| Foresight Group Holdings (LSE:FSG) | 31.7% | 30.9% |

| Velocity Composites (AIM:VEL) | 28.5% | 143.4% |

| TEAM (AIM:TEAM) | 25.8% | 58.6% |

| B90 Holdings (AIM:B90) | 24.4% | 142.7% |

| Afentra (AIM:AET) | 38.3% | 64.4% |

| Mothercare (AIM:MTC) | 15.1% | 41.2% |

Below we spotlight a couple of our favorites from our exclusive screener.

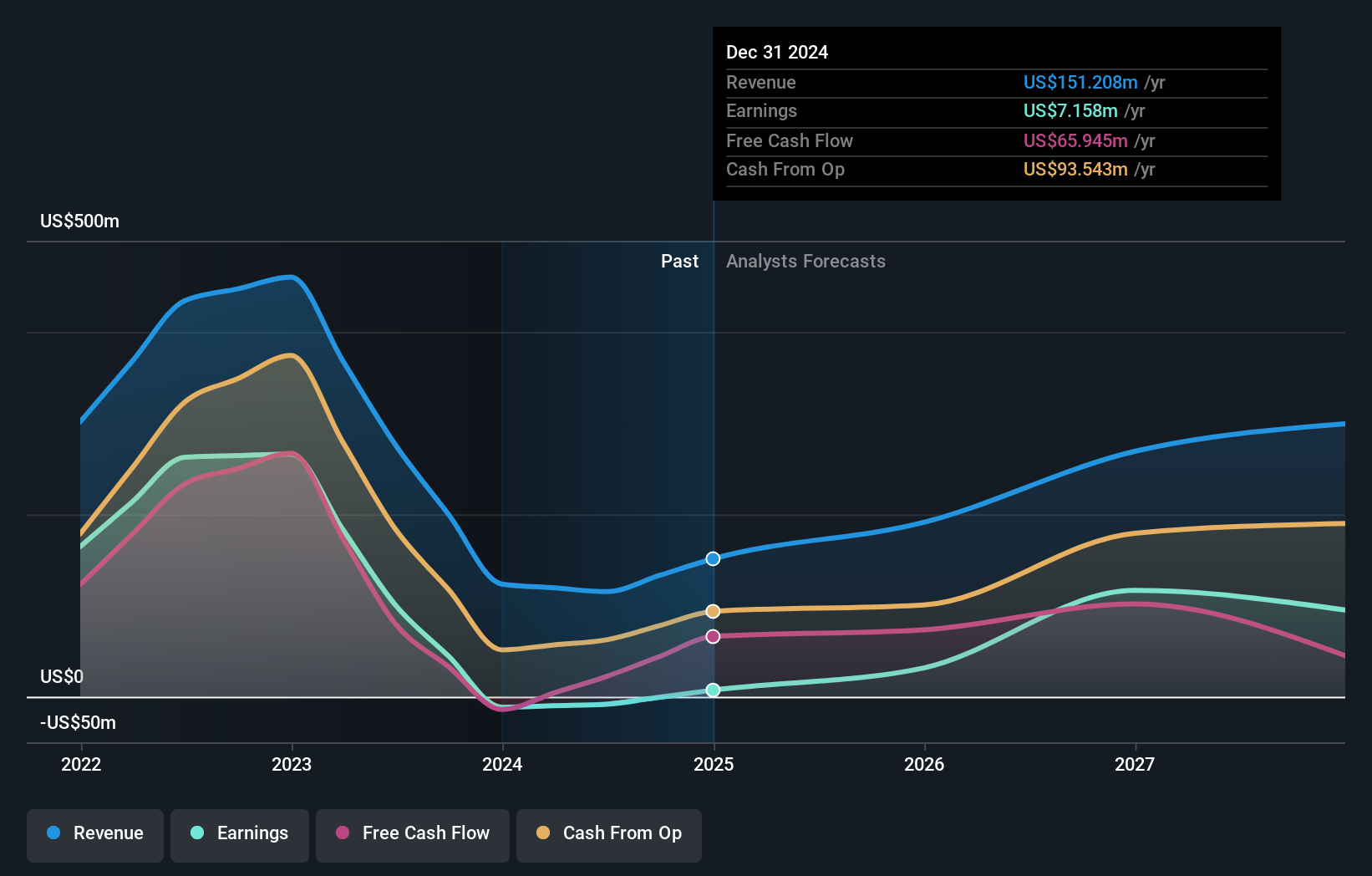

Gulf Keystone Petroleum (LSE:GKP)

Simply Wall St Growth Rating: ★★★★★★

Overview: Gulf Keystone Petroleum Limited is a company focused on the exploration, development, and production of oil and gas in the Kurdistan Region of Iraq, with a market capitalization of approximately £324.68 million.

Operations: The company generates its revenue primarily through the exploration and production of oil and gas, totaling $123.51 million.

Insider Ownership: 10.8%

Gulf Keystone Petroleum, a growth-oriented company with high insider ownership in the UK, is on track to become profitable within three years, showcasing potential above-average market growth. The firm's revenue is expected to increase by 25.1% annually, significantly outpacing the UK market forecast of 3.5%. Despite its highly volatile share price recently, Gulf Keystone has initiated a substantial share repurchase program valued at US$10 million, reinforcing shareholder value through strategic buybacks and treasury holdings.

- Dive into the specifics of Gulf Keystone Petroleum here with our thorough growth forecast report.

- Our valuation report unveils the possibility Gulf Keystone Petroleum's shares may be trading at a premium.

J D Wetherspoon (LSE:JDW)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: J D Wetherspoon plc, with a market capitalization of £0.90 billion, owns and operates a chain of pubs and hotels primarily in the United Kingdom and the Republic of Ireland.

Operations: The company generates its revenue primarily through its pubs, which brought in £2.00 billion.

Insider Ownership: 25.8%

J D Wetherspoon, a UK-based pub operator, shows promising growth with recent sales increasing by 3.3% quarterly and 6.5% year-to-date, outpacing similar periods last year. Insider activities reveal more buying than selling in the past three months, though not in large volumes. Despite lower profit margins compared to last year and interest payments not well covered by earnings, JDW expects significant earnings growth over the next three years, projected at 20% annually—higher than the UK market average.

- Delve into the full analysis future growth report here for a deeper understanding of J D Wetherspoon.

- Our expertly prepared valuation report J D Wetherspoon implies its share price may be too high.

TBC Bank Group (LSE:TBCG)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: TBC Bank Group PLC operates primarily in Georgia, Azerbaijan, and Uzbekistan, offering a range of financial services including banking, leasing, insurance, brokerage, and card processing to both corporate and individual clients with a market capitalization of approximately £1.37 billion.

Operations: The company generates revenue from various financial services such as banking, leasing, insurance, brokerage, and card processing across Georgia, Azerbaijan, and Uzbekistan.

Insider Ownership: 18%

TBC Bank Group, a prominent UK-based financial institution, has shown robust growth with its recent earnings report highlighting a significant increase in net interest income and net income. Despite the high volatility of its share price over the past three months, TBC Bank's revenue and earnings growth are forecasted to outpace the UK market. However, the bank faces challenges with a high level of bad loans at 2.1%. Recently, it announced a substantial GEL 75 million buyback program aimed at reducing share capital and supporting employee benefits.

- Click here to discover the nuances of TBC Bank Group with our detailed analytical future growth report.

- Insights from our recent valuation report point to the potential undervaluation of TBC Bank Group shares in the market.

Make It Happen

- Explore the 63 names from our Fast Growing UK Companies With High Insider Ownership screener here.

- Hold shares in these firms? Setup your portfolio in Simply Wall St to seamlessly track your investments and receive personalized updates on your portfolio's performance.

- Discover a world of investment opportunities with Simply Wall St's free app and access unparalleled stock analysis across all markets.

Interested In Other Possibilities?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

Valuation is complex, but we're helping make it simple.

Find out whether Gulf Keystone Petroleum is potentially over or undervalued by checking out our comprehensive analysis, which includes fair value estimates, risks and warnings, dividends, insider transactions and financial health.

View the Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About LSE:GKP

Gulf Keystone Petroleum

Engages in the exploration, development, and production of oil and gas in the Kurdistan Region of Iraq.

Exceptional growth potential with excellent balance sheet.