- United Kingdom

- /

- Capital Markets

- /

- LSE:RCP

RIT Capital Partners (LON:RCP) Will Pay A Larger Dividend Than Last Year At £0.19

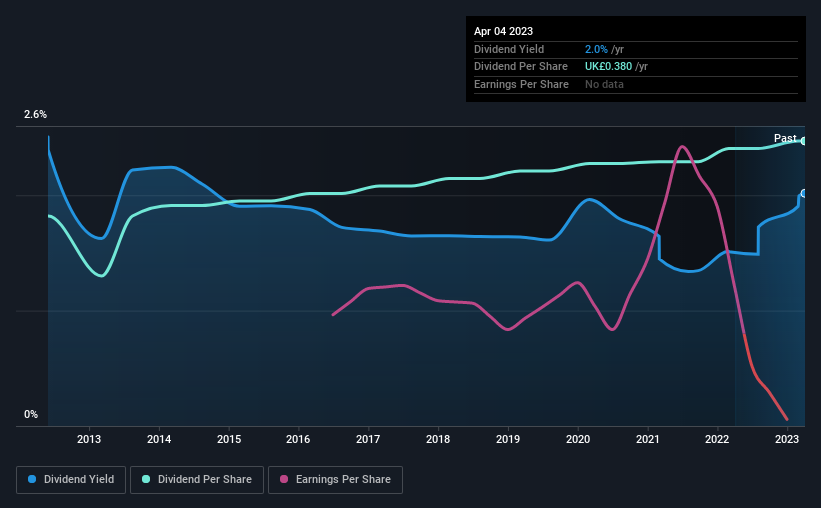

RIT Capital Partners plc's (LON:RCP) dividend will be increasing from last year's payment of the same period to £0.19 on 28th of April. Despite this raise, the dividend yield of 2.0% is only a modest boost to shareholder returns.

View our latest analysis for RIT Capital Partners

RIT Capital Partners Might Find It Hard To Continue The Dividend

If it is predictable over a long period, even low dividend yields can be attractive. RIT Capital Partners is unprofitable despite paying a dividend, and it is paying out 177% of its free cash flow. This makes us feel that the dividend will be hard to maintain.

Over the next year, EPS could expand by 1.2% if recent trends continue. While it is good to see income moving in the right direction, it still looks like the company won't achieve profitability. Unfortunately, for the dividend to continue at current levels the company definitely needs to get there sooner rather than later.

Dividend Volatility

While the company has been paying a dividend for a long time, it has cut the dividend at least once in the last 10 years. Since 2013, the dividend has gone from £0.28 total annually to £0.38. This means that it has been growing its distributions at 3.1% per annum over that time. The dividend has seen some fluctuations in the past, so even though the dividend was raised this year, we should remember that it has been cut in the past.

Dividend Growth May Be Hard To Achieve

With a relatively unstable dividend, it's even more important to evaluate if earnings per share is growing, which could point to a growing dividend in the future. However, RIT Capital Partners' EPS was effectively flat over the past five years, which could stop the company from paying more every year. With no profits, we don't think RIT Capital Partners has much potential to grow the dividend in the future.

The Dividend Could Prove To Be Unreliable

Overall, this is probably not a great income stock, even though the dividend is being raised at the moment. The track record isn't great, and the payments are a bit high to be considered sustainable. We would be a touch cautious of relying on this stock primarily for the dividend income.

Companies possessing a stable dividend policy will likely enjoy greater investor interest than those suffering from a more inconsistent approach. Meanwhile, despite the importance of dividend payments, they are not the only factors our readers should know when assessing a company. For example, we've picked out 1 warning sign for RIT Capital Partners that investors should know about before committing capital to this stock. Is RIT Capital Partners not quite the opportunity you were looking for? Why not check out our selection of top dividend stocks.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About LSE:RCP

Flawless balance sheet average dividend payer.

Similar Companies

Market Insights

Community Narratives