Advertisement

- United Kingdom

- /

- Consumer Finance

- /

- LSE:IPF

Earnings Update: Here's Why Analysts Just Lifted Their International Personal Finance plc (LON:IPF) Price Target To UK£1.39

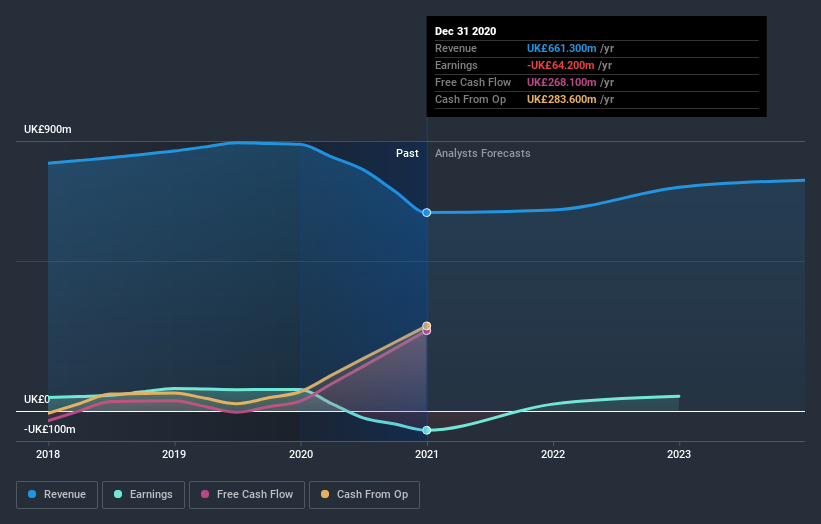

Shareholders will be ecstatic, with their stake up 27% over the past week following International Personal Finance plc's (LON:IPF) latest annual results. It was a moderately negative result overall - revenue fell 2.4% short of analyst estimates at UK£661m, and statutory losses were in line with analyst expectations, at UK£0.29 per share. This is an important time for investors, as they can track a company's performance in its report, look at what experts are forecasting for next year, and see if there has been any change to expectations for the business. So we collected the latest post-earnings statutory consensus estimates to see what could be in store for next year.

See our latest analysis for International Personal Finance

Following last week's earnings report, International Personal Finance's three analysts are forecasting 2021 revenues to be UK£669.7m, approximately in line with the last 12 months. International Personal Finance is also expected to turn profitable, with statutory earnings of UK£0.10 per share. Before this earnings report, the analysts had been forecasting revenues of UK£691.0m and earnings per share (EPS) of UK£0.19 in 2021. The analysts seem less optimistic after the recent results, reducing their sales forecasts and making a large cut to earnings per share numbers.

What's most unexpected is that the consensus price target rose 6.1% to UK£1.39, strongly implying the downgrade to forecasts is not expected to be more than a temporary blip. That's not the only conclusion we can draw from this data however, as some investors also like to consider the spread in estimates when evaluating analyst price targets. There are some variant perceptions on International Personal Finance, with the most bullish analyst valuing it at UK£1.65 and the most bearish at UK£1.10 per share. As you can see, analysts are not all in agreement on the stock's future, but the range of estimates is still reasonably narrow, which could suggest that the outcome is not totally unpredictable.

Looking at the bigger picture now, one of the ways we can make sense of these forecasts is to see how they measure up against both past performance and industry growth estimates. We would highlight that International Personal Finance's revenue growth is expected to slow, with the forecast 1.3% annualised growth rate until the end of 2021 being well below the historical 1.8% p.a. growth over the last five years. Compare this against other companies (with analyst forecasts) in the industry, which are in aggregate expected to see revenue growth of 21% annually. So it's pretty clear that, while revenue growth is expected to slow down, the wider industry is also expected to grow faster than International Personal Finance.

The Bottom Line

The biggest concern is that the analysts reduced their earnings per share estimates, suggesting business headwinds could lay ahead for International Personal Finance. Unfortunately, they also downgraded their revenue estimates, and our data indicates revenues are expected to perform worse than the wider industry. Even so, earnings per share are more important to the intrinsic value of the business. We note an upgrade to the price target, suggesting that the analysts believes the intrinsic value of the business is likely to improve over time.

With that in mind, we wouldn't be too quick to come to a conclusion on International Personal Finance. Long-term earnings power is much more important than next year's profits. At Simply Wall St, we have a full range of analyst estimates for International Personal Finance going out to 2023, and you can see them free on our platform here..

That said, it's still necessary to consider the ever-present spectre of investment risk. We've identified 1 warning sign with International Personal Finance , and understanding this should be part of your investment process.

If you decide to trade International Personal Finance, use the lowest-cost* platform that is rated #1 Overall by Barron’s, Interactive Brokers. Trade stocks, options, futures, forex, bonds and funds on 135 markets, all from a single integrated account. Promoted

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About LSE:IPF

International Personal Finance

Engages in financial services business in Europe and Mexico.

Good value with proven track record.

Market Insights

Advertisement

Community Narratives

The Next Phase of Energy Storage: How NeoVolta Is Tackling America’s Power Crunch

Fair Value US$7.50|35.1% undervalued

MA

Community Contributor

Why EnSilica is Worth Possibly 13x its Current Price

Fair Value UK£5.00|89.8% undervalued

DO

Community Contributor

M&A Activity, Industry Diversification & A Defense Contract Monopoly Will Push BWXT For Healthy Long-Term Growth

Fair Value US$220.00|15.2% undervalued

CL

Community Contributor

A case for Cassiar Gold Corp (TSXV: GLDC) to reach CAD$8-10 before 2030 (X30-37)

Fair Value CA$10.00|96.0% undervalued

AG

Community Contributor