- United Kingdom

- /

- Capital Markets

- /

- LSE:BAF

It's Down 31% But British & American Investment Trust PLC (LON:BAF) Could Be Riskier Than It Looks

British & American Investment Trust PLC (LON:BAF) shares have retraced a considerable 31% in the last month, reversing a fair amount of their solid recent performance. Longer-term shareholders would now have taken a real hit with the stock declining 2.1% in the last year.

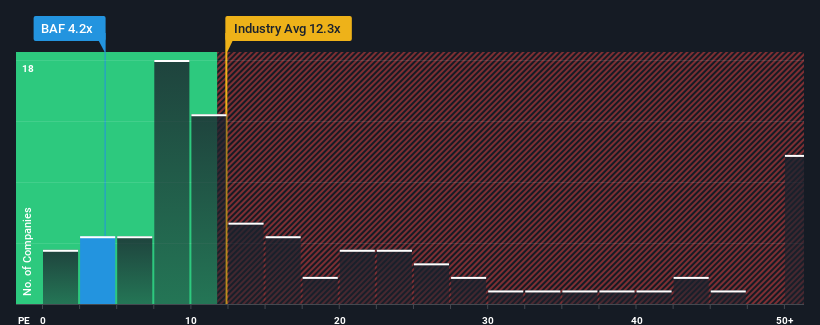

Following the heavy fall in price, given about half the companies in the United Kingdom have price-to-earnings ratios (or "P/E's") above 17x, you may consider British & American Investment Trust as a highly attractive investment with its 4.2x P/E ratio. However, the P/E might be quite low for a reason and it requires further investigation to determine if it's justified.

For example, consider that British & American Investment Trust's financial performance has been poor lately as its earnings have been in decline. One possibility is that the P/E is low because investors think the company won't do enough to avoid underperforming the broader market in the near future. If you like the company, you'd be hoping this isn't the case so that you could potentially pick up some stock while it's out of favour.

See our latest analysis for British & American Investment Trust

Is There Any Growth For British & American Investment Trust?

There's an inherent assumption that a company should far underperform the market for P/E ratios like British & American Investment Trust's to be considered reasonable.

Taking a look back first, the company's earnings per share growth last year wasn't something to get excited about as it posted a disappointing decline of 52%. Even so, admirably EPS has lifted 119% in aggregate from three years ago, notwithstanding the last 12 months. Accordingly, while they would have preferred to keep the run going, shareholders would probably welcome the medium-term rates of earnings growth.

Weighing that recent medium-term earnings trajectory against the broader market's one-year forecast for expansion of 20% shows it's noticeably more attractive on an annualised basis.

In light of this, it's peculiar that British & American Investment Trust's P/E sits below the majority of other companies. Apparently some shareholders believe the recent performance has exceeded its limits and have been accepting significantly lower selling prices.

The Final Word

British & American Investment Trust's P/E looks about as weak as its stock price lately. While the price-to-earnings ratio shouldn't be the defining factor in whether you buy a stock or not, it's quite a capable barometer of earnings expectations.

We've established that British & American Investment Trust currently trades on a much lower than expected P/E since its recent three-year growth is higher than the wider market forecast. When we see strong earnings with faster-than-market growth, we assume potential risks are what might be placing significant pressure on the P/E ratio. At least price risks look to be very low if recent medium-term earnings trends continue, but investors seem to think future earnings could see a lot of volatility.

Before you settle on your opinion, we've discovered 4 warning signs for British & American Investment Trust (1 can't be ignored!) that you should be aware of.

You might be able to find a better investment than British & American Investment Trust. If you want a selection of possible candidates, check out this free list of interesting companies that trade on a low P/E (but have proven they can grow earnings).

Valuation is complex, but we're here to simplify it.

Discover if British & American Investment Trust might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About LSE:BAF

British & American Investment Trust

British & American Investment Trust plc is a publically owned investment manager.

Good value with adequate balance sheet and pays a dividend.

Market Insights

Community Narratives