Advertisement

- United Kingdom

- /

- Entertainment

- /

- AIM:LBG

Exploring LBG Media And 2 Other Promising Small Cap Gems In The UK

Simply Wall St

Reviewed by Simply Wall St

As the United Kingdom's FTSE 100 and FTSE 250 indices experience downward pressure due to weak trade data from China, investors are increasingly scrutinizing small-cap stocks for potential opportunities amidst global economic uncertainties. In this environment, identifying promising small-cap companies like LBG Media requires a focus on resilience and growth potential in sectors less impacted by international trade fluctuations.

Top 10 Undiscovered Gems With Strong Fundamentals In The United Kingdom

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| M&G Credit Income Investment Trust | NA | 17.28% | 15.80% | ★★★★★★ |

| London Security | 0.22% | 10.13% | 7.75% | ★★★★★★ |

| Andrews Sykes Group | NA | 2.15% | 4.93% | ★★★★★★ |

| B.P. Marsh & Partners | NA | 29.42% | 31.34% | ★★★★★★ |

| Globaltrans Investment | 8.54% | 5.28% | 22.11% | ★★★★★★ |

| Impellam Group | 31.12% | -5.43% | -6.86% | ★★★★★★ |

| VH Global Sustainable Energy Opportunities | NA | 18.30% | 20.03% | ★★★★★★ |

| FW Thorpe | 5.89% | 11.97% | 12.07% | ★★★★★☆ |

| BBGI Global Infrastructure | 0.02% | 3.08% | 6.85% | ★★★★★☆ |

| Goodwin | 52.21% | 9.26% | 13.12% | ★★★★★☆ |

Here's a peek at a few of the choices from the screener.

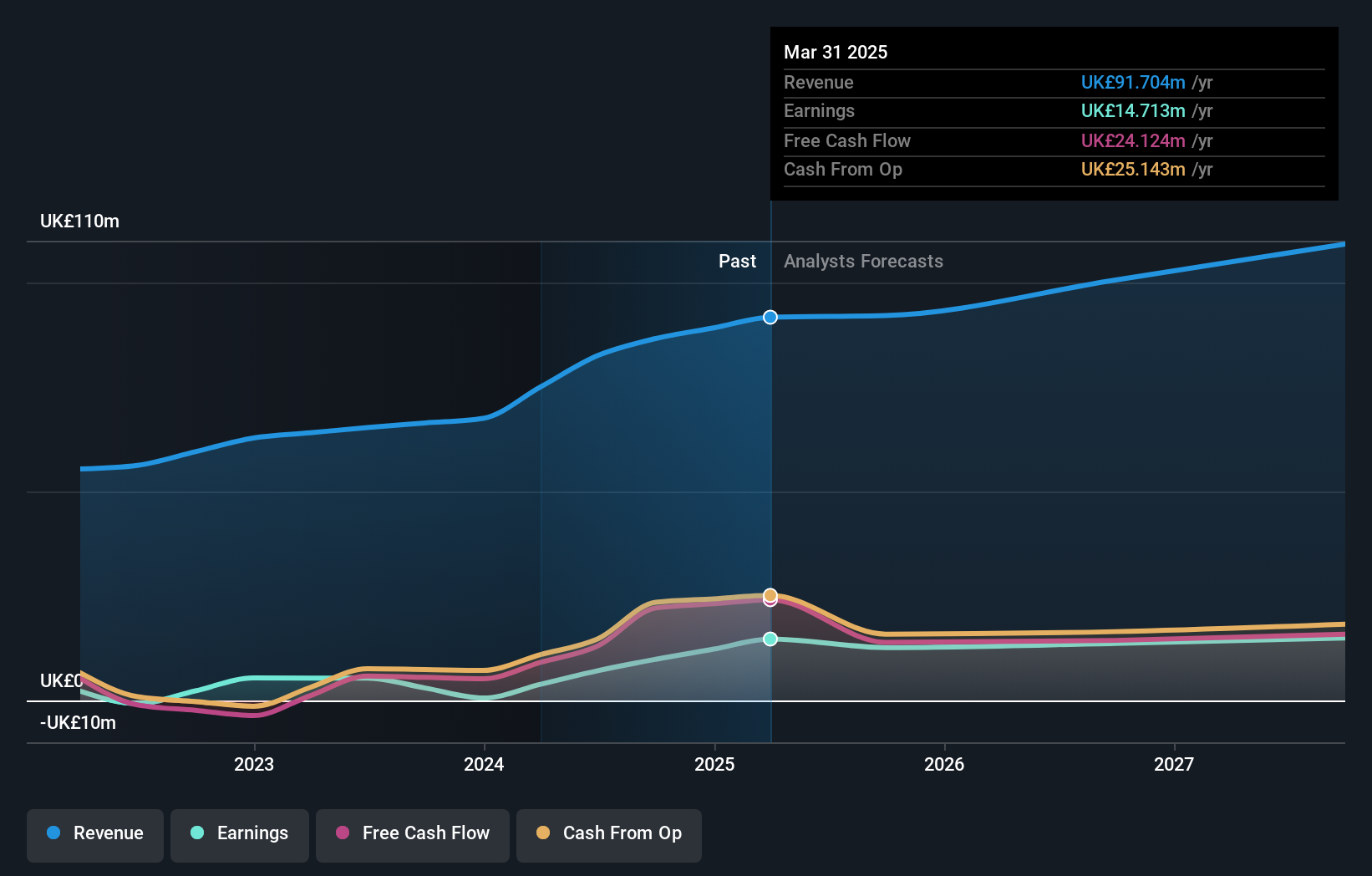

LBG Media (AIM:LBG)

Simply Wall St Value Rating: ★★★★★★

Overview: LBG Media plc is an online media publisher operating in the United Kingdom, Ireland, Australia, the United States, and internationally with a market cap of £278.08 million.

Operations: LBG Media generates revenue primarily from its online media publishing segment, which reported £82.54 million. The company's financial performance is reflected in its market capitalization of £278.08 million.

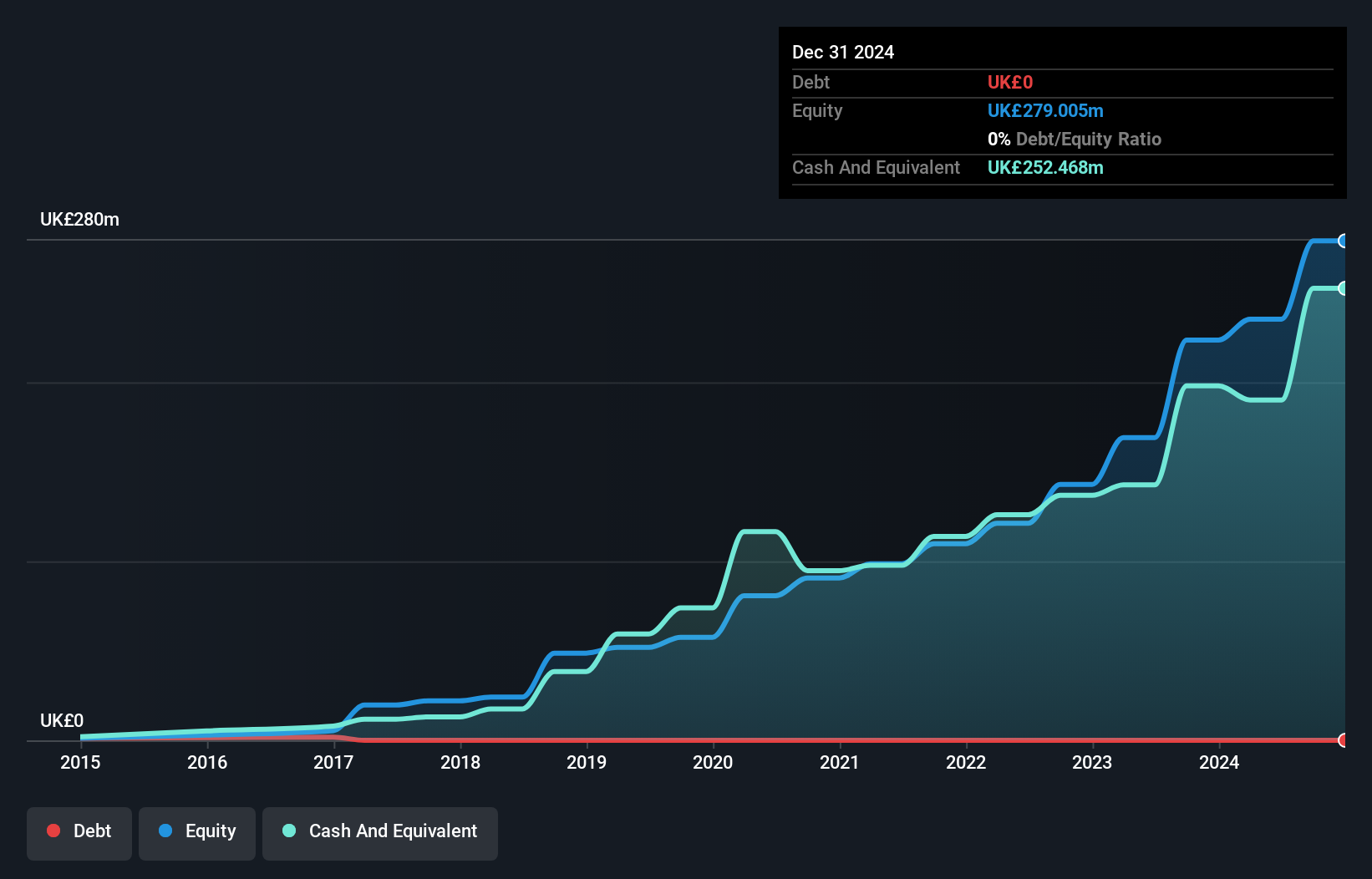

LBG Media, a nimble player in the UK market, has shown impressive earnings growth of 33% over the past year, outpacing its industry peers who saw a -24.9% change. Despite a one-off £3.5M loss impacting recent results, LBG remains debt-free and is trading at 27% below estimated fair value. For the half-year ending June 2024, sales jumped to £42.28M from £27.25M year-on-year, with net income swinging to £4.75M from a previous loss of £1.8M—demonstrating resilience and potential for future growth amidst industry challenges.

- Click to explore a detailed breakdown of our findings in LBG Media's health report.

Evaluate LBG Media's historical performance by accessing our past performance report.

Alpha Group International (LSE:ALPH)

Simply Wall St Value Rating: ★★★★★★

Overview: Alpha Group International plc offers foreign exchange risk management and alternative banking solutions across the United Kingdom, Europe, Canada, and internationally, with a market capitalization of £962.37 million.

Operations: The company generates revenue primarily from its Alpha Pay, Institutional, and Corporate segments, with Alpha Pay contributing £72.30 million and Institutional bringing in £67.47 million. The Corporate segment is further divided into Toronto (£3.72 million), Amsterdam (£9.57 million), and London excluding Amsterdam (£46.92 million).

Alpha Group International showcases a compelling blend of financial strength and strategic leadership changes. With a Price-To-Earnings ratio of 10.2x, it trades below the UK market average, indicating potential value. The company is debt-free and reported impressive earnings growth of 46.3% over the past year, outpacing its industry peers. Recent executive shifts include Clive Kahn stepping in as CEO from January 2025, following Morgan Tillbrook's tenure; both leaders are committed to significant shareholdings in Alpha. Additionally, Alpha's interim dividend increased to £0.042 per share for 2024, reflecting confidence in its robust earnings performance and future prospects.

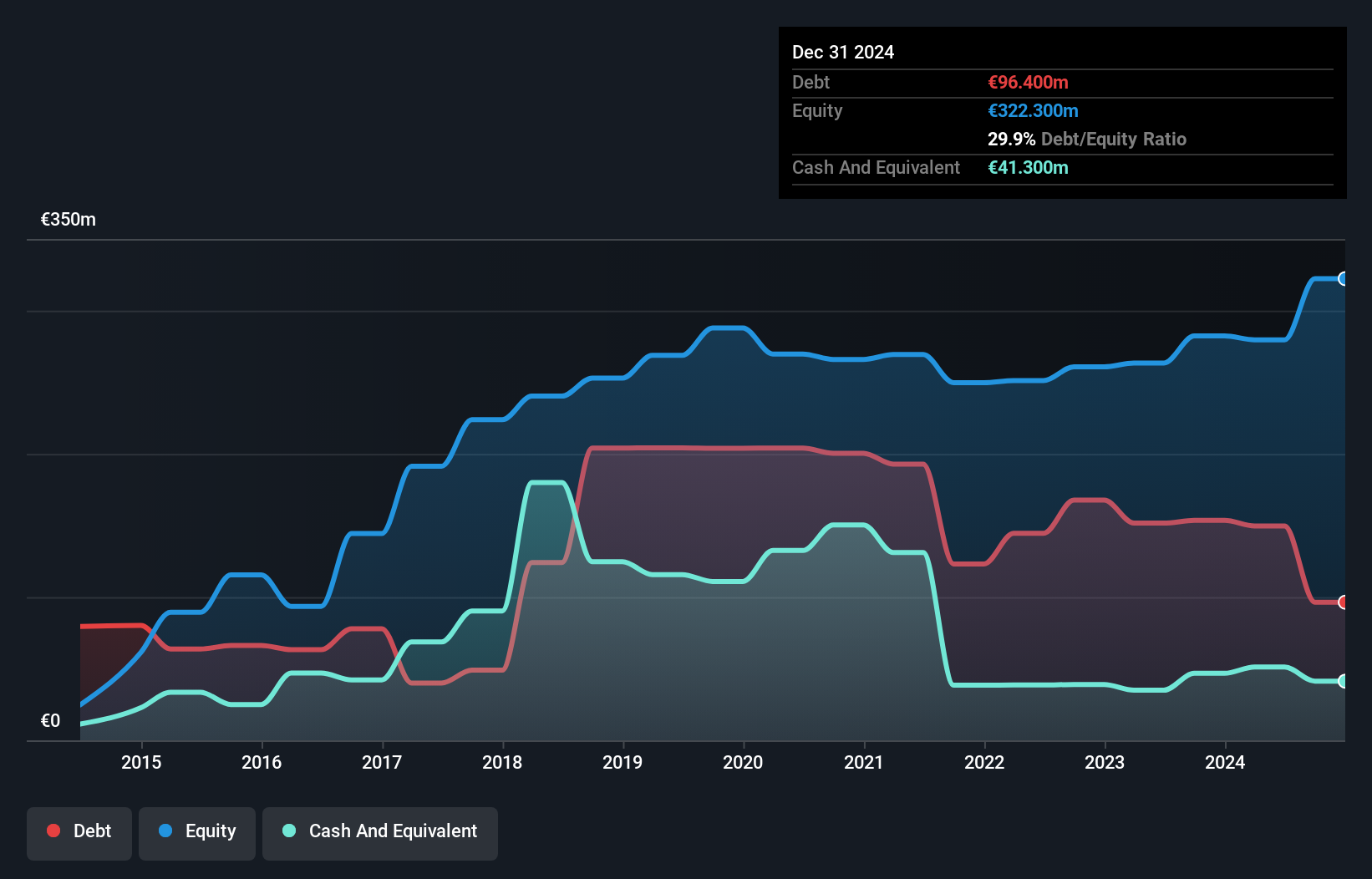

Irish Continental Group (LSE:ICGC)

Simply Wall St Value Rating: ★★★★☆☆

Overview: Irish Continental Group plc is a maritime transport company with a market cap of £748.84 million, providing ferry and container shipping services.

Operations: The company generates revenue primarily from its Ferries segment (€430.10 million) and Container and Terminal segment (€195.80 million).

Irish Continental Group, a notable player in the UK shipping industry, has shown resilience with earnings growth of 7.2% over the past year, outpacing the sector's -34%. The company's net debt to equity ratio stands at a satisfactory 35.2%, reflecting prudent financial management. Interest payments are well covered by EBIT at 10x coverage. Recent half-year results revealed sales of €285 million and net income of €13.7 million, slightly up from last year’s figures. Trading below estimated fair value by 13.7%, ICG appears undervalued with promising revenue growth forecasts of nearly 5% annually.

- Delve into the full analysis health report here for a deeper understanding of Irish Continental Group.

Learn about Irish Continental Group's historical performance.

Taking Advantage

- Gain an insight into the universe of 73 UK Undiscovered Gems With Strong Fundamentals by clicking here.

- Already own these companies? Bring clarity to your investment decisions by linking up your portfolio with Simply Wall St, where you can monitor all the vital signs of your stocks effortlessly.

- Simply Wall St is a revolutionary app designed for long-term stock investors, it's free and covers every market in the world.

Interested In Other Possibilities?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About AIM:LBG

LBG Media

Operates an online media publisher in the United Kingdom, Ireland, Australia, the United States, and internationally.

Flawless balance sheet with solid track record.

Market Insights

Advertisement

Community Narratives

The Future of Drug Testing? Fingerprint Tech Shows Serious Promise

Fair Value US$2.98|40.3% undervalued

JO

Community Contributor

Suncorp’s Next Chapter: Insurance-Only and Ready to Grow

Fair Value AU$22.83|7.9% undervalued

RO

Community Contributor

Thyssenkrupp Nucera Will Achieve Double-Digit Profits by 2030 Boosted by Hydrogen Growth

Fair Value €14.40|31.6% undervalued

CH

Community Contributor

Tesla’s Nvidia Moment – The AI & Robotics Inflection Point

Fair Value US$359.72|12.3% undervalued

BL

Community Contributor