Advertisement

The harsh reality for Whitbread plc (LON:WTB) shareholders is that its auditors, Deloitte & Touche LLP, expressed doubts about its ability to continue as a going concern, in its reported results to February 2021. Thus we can say that, based on the results to that date, the company should raise capital or otherwise raise cash, without much delay.

Since the company probably needs cash fairly quickly, it may be in a position where it has to accept whatever terms it can get. So current risks on the balance sheet could have a big impact on how shareholders fare from here. The big consideration is whether it can repay its debt, since in the worst case scenario, creditors could force the company to bankruptcy.

View our latest analysis for Whitbread

How Much Debt Does Whitbread Carry?

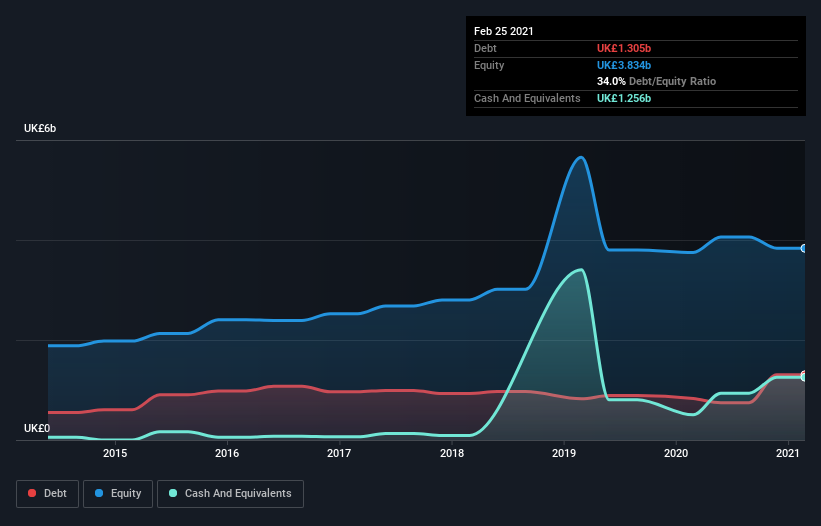

You can click the graphic below for the historical numbers, but it shows that as of February 2021 Whitbread had UK£1.30b of debt, an increase on UK£829.9m, over one year. However, it does have UK£1.26b in cash offsetting this, leading to net debt of about UK£48.9m.

How Strong Is Whitbread's Balance Sheet?

Zooming in on the latest balance sheet data, we can see that Whitbread had liabilities of UK£775.3m due within 12 months and liabilities of UK£4.19b due beyond that. Offsetting this, it had UK£1.26b in cash and UK£56.6m in receivables that were due within 12 months. So it has liabilities totalling UK£3.65b more than its cash and near-term receivables, combined.

While this might seem like a lot, it is not so bad since Whitbread has a market capitalization of UK£6.62b, and so it could probably strengthen its balance sheet by raising capital if it needed to. But we definitely want to keep our eyes open to indications that its debt is bringing too much risk. But either way, Whitbread has virtually no net debt, so it's fair to say it does not have a heavy debt load! There's no doubt that we learn most about debt from the balance sheet. But it is future earnings, more than anything, that will determine Whitbread's ability to maintain a healthy balance sheet going forward. So if you're focused on the future you can check out this free report showing analyst profit forecasts.

In the last year Whitbread had a loss before interest and tax, and actually shrunk its revenue by 71%, to UK£598m. To be frank that doesn't bode well.

Caveat Emptor

While Whitbread's falling revenue is about as heartwarming as a wet blanket, arguably its earnings before interest and tax (EBIT) loss is even less appealing. Indeed, it lost UK£622m at the EBIT level. Considering that alongside the liabilities mentioned above does not give us much confidence that company should be using so much debt. So we think its balance sheet is a little strained, though not beyond repair. However, it doesn't help that it burned through UK£619m of cash over the last year. So in short it's a really risky stock. We prefer to avoid a company after its auditor has expressed any uncertainty about its ability to continue as a going concern. That's because we find it more comfortable to invest in companies that always keep the balance sheet reasonably strong. When analysing debt levels, the balance sheet is the obvious place to start. However, not all investment risk resides within the balance sheet - far from it. Case in point: We've spotted 3 warning signs for Whitbread you should be aware of, and 1 of them shouldn't be ignored.

Of course, if you're the type of investor who prefers buying stocks without the burden of debt, then don't hesitate to discover our exclusive list of net cash growth stocks, today.

If you decide to trade Whitbread, use the lowest-cost* platform that is rated #1 Overall by Barron’s, Interactive Brokers. Trade stocks, options, futures, forex, bonds and funds on 135 markets, all from a single integrated account. Promoted

Valuation is complex, but we're here to simplify it.

Discover if Whitbread might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About LSE:WTB

Whitbread

Operates hotels and restaurants in the United Kingdom, Germany, and internationally.

Good value with adequate balance sheet and pays a dividend.

Similar Companies

Market Insights

Advertisement

Community Narratives

Nike's Direct-to-Consumer Focus Will Drive Future Growth

Fair Value US$87.90|22.7% undervalued

UN

Community Contributor

Novo Nordisk will dominate GLP-1 market with Ozempic and Wegovy growth

Fair Value US$89.59|14.2% undervalued

BE

Community Contributor

Rheinmetall could get 20-25% of EU-NATO 3%-GDP defence spending

Fair Value €7.57k|82.8% undervalued

NO

Community Contributor