Stock Analysis

- United Kingdom

- /

- Banks

- /

- LSE:TBCG

High Insider Ownership Marks These 3 UK Growth Companies

Reviewed by Simply Wall St

As the United Kingdom braces for a pivotal general election, financial markets remain cautiously optimistic, with the FTSE 100 showing modest gains. In this context of political and economic anticipation, companies with high insider ownership may offer an interesting perspective on commitment and confidence in their growth trajectories amidst fluctuating market conditions.

Top 10 Growth Companies With High Insider Ownership In The United Kingdom

| Name | Insider Ownership | Earnings Growth |

| Gulf Keystone Petroleum (LSE:GKP) | 10.8% | 47.6% |

| Plant Health Care (AIM:PHC) | 30.7% | 121.3% |

| Petrofac (LSE:PFC) | 16.6% | 124.5% |

| Integrated Diagnostics Holdings (LSE:IDHC) | 26.7% | 23.5% |

| LSL Property Services (LSE:LSL) | 10.8% | 33.3% |

| Velocity Composites (AIM:VEL) | 27.8% | 143.4% |

| Belluscura (AIM:BELL) | 39.1% | 124.1% |

| Judges Scientific (AIM:JDG) | 11.5% | 25.3% |

| Afentra (AIM:AET) | 37.2% | 64.4% |

| Mothercare (AIM:MTC) | 15.1% | 41.2% |

We're going to check out a few of the best picks from our screener tool.

Foresight Group Holdings (LSE:FSG)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Foresight Group Holdings Limited is an infrastructure and private equity manager operating across the United Kingdom, Italy, Luxembourg, Ireland, Spain, and Australia with a market capitalization of approximately £597.44 million.

Operations: The company generates revenue through three primary segments: Infrastructure (£84.17 million), Private Equity (£47.35 million), and Foresight Capital Management (£9.80 million).

Insider Ownership: 31.8%

Foresight Group Holdings, a UK-based company, showcases robust growth with its earnings expected to rise by 31.6% annually, outpacing the UK market's 12.5%. Similarly, its revenue growth forecast at 10.4% annually also exceeds the market's 3.5%. However, its dividend coverage is weak as earnings do not adequately cover the 4.49% dividend yield. The firm maintains high insider ownership with no significant insider trading reported recently, underscoring stability and confidence from management despite a modest buyback program completed for £0.97 million.

- Click here and access our complete growth analysis report to understand the dynamics of Foresight Group Holdings.

- According our valuation report, there's an indication that Foresight Group Holdings' share price might be on the cheaper side.

Playtech (LSE:PTEC)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Playtech plc is a technology company that offers gambling software, services, content, and platform technologies across the globe, with a market capitalization of approximately £1.46 billion.

Operations: Playtech's revenue is primarily derived from its Gaming B2B and Gaming B2C segments, which generated €684.10 million and €946.60 million respectively, along with smaller contributions from B2C - HAPPYBET and Sun Bingo totaling €91.60 million.

Insider Ownership: 13.5%

Playtech, a UK-based growth company with high insider ownership, is trading at 57.4% below its estimated fair value, presenting a good relative value in its sector. Analysts expect Playtech's earnings to grow by 20.62% annually over the next three years, outperforming the UK market forecast of 12.5%. Recently, Playtech announced a strategic partnership with MGM Resorts to deliver live casino content, enhancing its product offerings and market reach. However, its Return on Equity is anticipated to remain low at 8.9%, which could be a concern for potential growth sustainability.

- Unlock comprehensive insights into our analysis of Playtech stock in this growth report.

- Our expertly prepared valuation report Playtech implies its share price may be lower than expected.

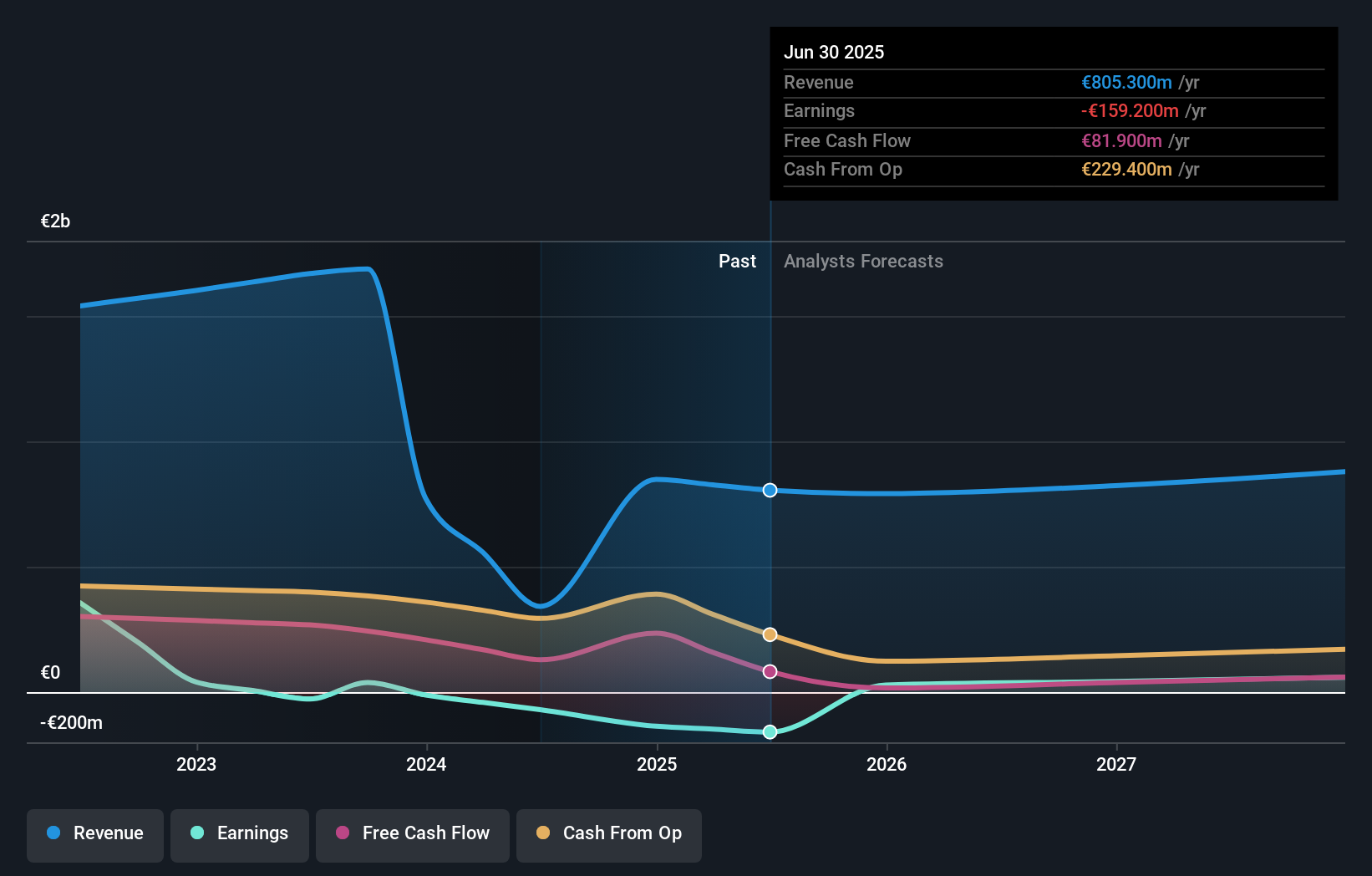

TBC Bank Group (LSE:TBCG)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: TBC Bank Group PLC operates primarily in Georgia, Azerbaijan, and Uzbekistan, offering a range of services including banking, leasing, insurance, brokerage, and card processing to both corporate and individual clients with a market capitalization of approximately £1.43 billion.

Operations: The company generates revenue through diverse financial services such as banking, leasing, insurance, brokerage, and card processing across Georgia, Azerbaijan, and Uzbekistan.

Insider Ownership: 18%

TBC Bank Group, a UK growth company with high insider ownership, demonstrates robust financial performance with a recent increase in net interest income to GEL 442.84 million and net income to GEL 292.81 million for Q1 2024. Despite its volatile share price and unstable dividend track record, the bank's earnings are projected to grow by 15.2% annually, outpacing the UK market's average of 12.5%. Additionally, TBCG has initiated a substantial share buyback program valued at GEL 75 million to reduce share capital and support shareholder value.

- Dive into the specifics of TBC Bank Group here with our thorough growth forecast report.

- Our valuation report here indicates TBC Bank Group may be undervalued.

Next Steps

- Delve into our full catalog of 65 Fast Growing UK Companies With High Insider Ownership here.

- Already own these companies? Link your portfolio to Simply Wall St and get alerts on any new warning signs to your stocks.

- Enhance your investing ability with the Simply Wall St app and enjoy free access to essential market intelligence spanning every continent.

Looking For Alternative Opportunities?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

Valuation is complex, but we're helping make it simple.

Find out whether TBC Bank Group is potentially over or undervalued by checking out our comprehensive analysis, which includes fair value estimates, risks and warnings, dividends, insider transactions and financial health.

View the Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About LSE:TBCG

TBC Bank Group

Through its subsidiaries, provides banking, leasing, insurance, brokerage, and card processing services to corporate and individual customers in Georgia, Azerbaijan, and Uzbekistan.

Undervalued with reasonable growth potential and pays a dividend.