- United Kingdom

- /

- Consumer Durables

- /

- LSE:VID

Returns On Capital At Vitec Group (LON:VTC) Paint A Concerning Picture

If you're looking for a multi-bagger, there's a few things to keep an eye out for. In a perfect world, we'd like to see a company investing more capital into its business and ideally the returns earned from that capital are also increasing. Ultimately, this demonstrates that it's a business that is reinvesting profits at increasing rates of return. However, after investigating Vitec Group (LON:VTC), we don't think it's current trends fit the mold of a multi-bagger.

What is Return On Capital Employed (ROCE)?

Just to clarify if you're unsure, ROCE is a metric for evaluating how much pre-tax income (in percentage terms) a company earns on the capital invested in its business. The formula for this calculation on Vitec Group is:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

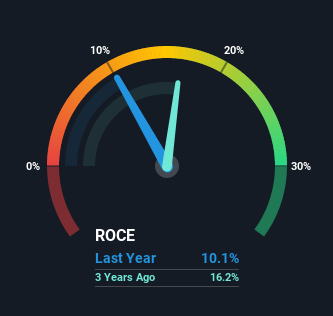

0.10 = UK£30m ÷ (UK£383m - UK£89m) (Based on the trailing twelve months to June 2021).

Thus, Vitec Group has an ROCE of 10%. That's a pretty standard return and it's in line with the industry average of 10%.

See our latest analysis for Vitec Group

In the above chart we have measured Vitec Group's prior ROCE against its prior performance, but the future is arguably more important. If you'd like to see what analysts are forecasting going forward, you should check out our free report for Vitec Group.

What Does the ROCE Trend For Vitec Group Tell Us?

When we looked at the ROCE trend at Vitec Group, we didn't gain much confidence. Over the last five years, returns on capital have decreased to 10% from 13% five years ago. However, given capital employed and revenue have both increased it appears that the business is currently pursuing growth, at the consequence of short term returns. If these investments prove successful, this can bode very well for long term stock performance.

Our Take On Vitec Group's ROCE

In summary, despite lower returns in the short term, we're encouraged to see that Vitec Group is reinvesting for growth and has higher sales as a result. Furthermore the stock has climbed 78% over the last five years, it would appear that investors are upbeat about the future. So while the underlying trends could already be accounted for by investors, we still think this stock is worth looking into further.

If you'd like to know about the risks facing Vitec Group, we've discovered 2 warning signs that you should be aware of.

If you want to search for solid companies with great earnings, check out this free list of companies with good balance sheets and impressive returns on equity.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About LSE:VID

Videndum

Designs, manufactures, and distributes products and services that enable end users to capture and share content for the broadcast, cinematic, video, photographic, and smartphone applications worldwide.

Undervalued with reasonable growth potential.