Advertisement

- United Kingdom

- /

- Consumer Durables

- /

- LSE:TW.

Taylor Wimpey plc's (LON:TW.) Dismal Stock Performance Reflects Weak Fundamentals

It is hard to get excited after looking at Taylor Wimpey's (LON:TW.) recent performance, when its stock has declined 24% over the past three months. We decided to study the company's financials to determine if the downtrend will continue as the long-term performance of a company usually dictates market outcomes. Specifically, we decided to study Taylor Wimpey's ROE in this article.

Return on equity or ROE is an important factor to be considered by a shareholder because it tells them how effectively their capital is being reinvested. Simply put, it is used to assess the profitability of a company in relation to its equity capital.

Check out our latest analysis for Taylor Wimpey

How Is ROE Calculated?

The formula for ROE is:

Return on Equity = Net Profit (from continuing operations) ÷ Shareholders' Equity

So, based on the above formula, the ROE for Taylor Wimpey is:

5.6% = UK£246m ÷ UK£4.4b (Based on the trailing twelve months to June 2024).

The 'return' is the profit over the last twelve months. One way to conceptualize this is that for each £1 of shareholders' capital it has, the company made £0.06 in profit.

What Has ROE Got To Do With Earnings Growth?

We have already established that ROE serves as an efficient profit-generating gauge for a company's future earnings. Depending on how much of these profits the company reinvests or "retains", and how effectively it does so, we are then able to assess a company’s earnings growth potential. Generally speaking, other things being equal, firms with a high return on equity and profit retention, have a higher growth rate than firms that don’t share these attributes.

Taylor Wimpey's Earnings Growth And 5.6% ROE

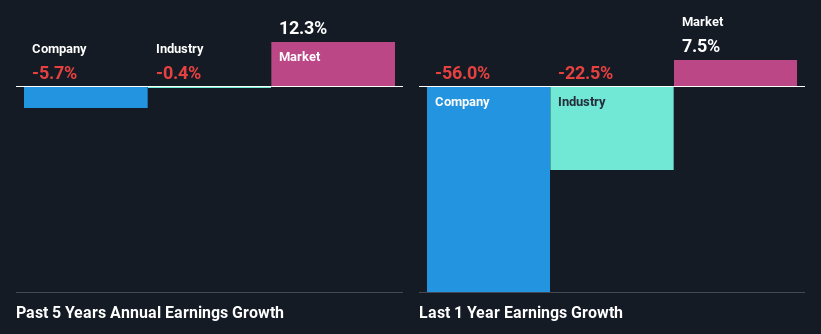

On the face of it, Taylor Wimpey's ROE is not much to talk about. However, its ROE is similar to the industry average of 6.0%, so we won't completely dismiss the company. But Taylor Wimpey saw a five year net income decline of 5.7% over the past five years. Bear in mind, the company does have a slightly low ROE. So that's what might be causing earnings growth to shrink.

Furthermore, even when compared to the industry, which has been shrinking its earnings at a rate of 0.4% over the last few years, we found that Taylor Wimpey's performance is pretty disappointing, as it suggests that the company has been shrunk its earnings at a rate faster than the industry.

Earnings growth is an important metric to consider when valuing a stock. The investor should try to establish if the expected growth or decline in earnings, whichever the case may be, is priced in. By doing so, they will have an idea if the stock is headed into clear blue waters or if swampy waters await. Has the market priced in the future outlook for TW.? You can find out in our latest intrinsic value infographic research report.

Is Taylor Wimpey Efficiently Re-investing Its Profits?

Taylor Wimpey's declining earnings is not surprising given how the company is spending most of its profits in paying dividends, judging by its three-year median payout ratio of 60% (or a retention ratio of 40%). With only very little left to reinvest into the business, growth in earnings is far from likely. Our risks dashboard should have the 3 risks we have identified for Taylor Wimpey.

Moreover, Taylor Wimpey has been paying dividends for at least ten years or more suggesting that management must have perceived that the shareholders prefer dividends over earnings growth. Our latest analyst data shows that the future payout ratio of the company is expected to rise to 83% over the next three years. However, Taylor Wimpey's future ROE is expected to rise to 8.9% despite the expected increase in the company's payout ratio. We infer that there could be other factors that could be driving the anticipated growth in the company's ROE.

Conclusion

In total, we would have a hard think before deciding on any investment action concerning Taylor Wimpey. As a result of its low ROE and lack of much reinvestment into the business, the company has seen a disappointing earnings growth rate. Having said that, looking at current analyst estimates, we found that the company's earnings growth rate is expected to see a huge improvement. To know more about the latest analysts predictions for the company, check out this visualization of analyst forecasts for the company.

Valuation is complex, but we're here to simplify it.

Discover if Taylor Wimpey might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About LSE:TW.

Taylor Wimpey

Operates as a homebuilder company in the United Kingdom and Spain.

Flawless balance sheet and good value.

Similar Companies

Market Insights

Advertisement

Community Narratives

WhiteCap Is Positioned To Profit Regardless Of Trump's Policy

Fair Value CA$22.60|61.6% undervalued

ST

Equity Analyst and Writer

Microsoft's Evolution Will Drive Revenue to New Heights Fueled by AI

Fair Value US$360.00|28.6% overvalued

BR

Community Contributor

A CASE FOR USD$2.50 (CAD$3.44) BY 2028 (A 5-10 BAGGER)

Fair Value CA$3.44|87.5% undervalued

AG

Community Contributor