Advertisement

- United Kingdom

- /

- Professional Services

- /

- AIM:NBB

Norman Broadbent Leads 3 Promising Penny Stocks On UK Exchange

Simply Wall St

Reviewed by Simply Wall St

The UK market has faced challenges recently, with the FTSE 100 and FTSE 250 indices experiencing declines due to weak trade data from China, highlighting global economic uncertainties. In such a climate, identifying promising investment opportunities requires a focus on financial strength and growth potential. Penny stocks, although an older term, still represent an intriguing area for investors seeking smaller companies that combine value and growth prospects.

Top 10 Penny Stocks In The United Kingdom

| Name | Share Price | Market Cap | Financial Health Rating |

| Polar Capital Holdings (AIM:POLR) | £5.00 | £481.98M | ★★★★★★ |

| Begbies Traynor Group (AIM:BEG) | £0.972 | £153.33M | ★★★★★★ |

| Foresight Group Holdings (LSE:FSG) | £3.68 | £420.17M | ★★★★★★ |

| ME Group International (LSE:MEGP) | £2.045 | £770.58M | ★★★★★★ |

| Stelrad Group (LSE:SRAD) | £1.415 | £180.2M | ★★★★★☆ |

| Secure Trust Bank (LSE:STB) | £3.58 | £68.28M | ★★★★☆☆ |

| Next 15 Group (AIM:NFG) | £3.505 | £348.59M | ★★★★☆☆ |

| Tristel (AIM:TSTL) | £3.90 | £186M | ★★★★★★ |

| Ultimate Products (LSE:ULTP) | £1.05 | £89.71M | ★★★★★★ |

| Helios Underwriting (AIM:HUW) | £2.02 | £144.11M | ★★★★★☆ |

Click here to see the full list of 445 stocks from our UK Penny Stocks screener.

Below we spotlight a couple of our favorites from our exclusive screener.

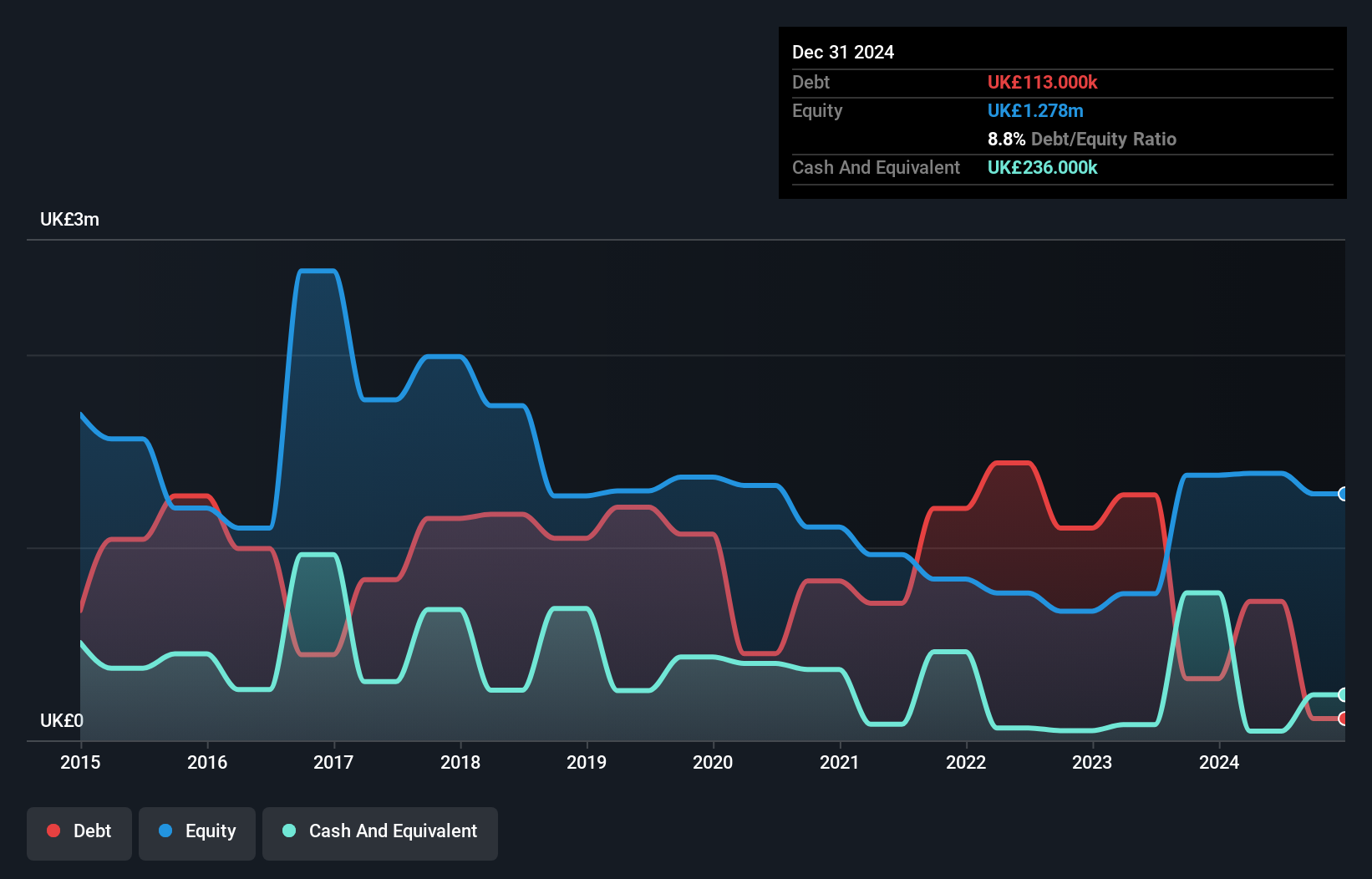

Norman Broadbent (AIM:NBB)

Simply Wall St Financial Health Rating: ★★★★☆☆

Overview: Norman Broadbent plc, with a market cap of £2.24 million, provides professional services in the United Kingdom and internationally through its subsidiaries.

Operations: The company generates revenue from two primary segments: £8.50 million from the United Kingdom and £2.80 million from the Rest of The World.

Market Cap: £2.24M

Norman Broadbent plc, with a market cap of £2.24 million, has recently become profitable and is actively seeking acquisition opportunities to drive growth and expand its international presence. The company generates significant revenue from both the UK (£8.50 million) and internationally (£2.80 million). Despite a high net debt to equity ratio of 48.5%, its debt is well-covered by operating cash flow (90.3%), and interest payments are well-covered by EBIT at 5.6 times coverage. The board and management teams are experienced, though the stock remains highly volatile compared to most UK stocks.

- Click here to discover the nuances of Norman Broadbent with our detailed analytical financial health report.

- Explore historical data to track Norman Broadbent's performance over time in our past results report.

ValiRx (AIM:VAL)

Simply Wall St Financial Health Rating: ★★★★★★

Overview: ValiRx plc is a biopharmaceutical company focused on developing oncology therapeutics and companion diagnostics in the United Kingdom, with a market cap of £1.16 million.

Operations: The company has not reported any revenue segments.

Market Cap: £1.16M

ValiRx plc, with a market cap of £1.16 million, is a pre-revenue biopharmaceutical company focused on oncology therapeutics. Despite being unprofitable, the company has managed to reduce its losses by 3.5% annually over the past five years and maintains more cash than total debt. Recent developments include raising £1.573 million through a follow-on equity offering and securing a contract potentially worth over £100,000 for cell-based assays with Amply Discovery Limited. While ValiRx's short-term assets exceed its liabilities, it faces high share price volatility and an inexperienced board with an average tenure of 0.8 years.

- Get an in-depth perspective on ValiRx's performance by reading our balance sheet health report here.

- Assess ValiRx's previous results with our detailed historical performance reports.

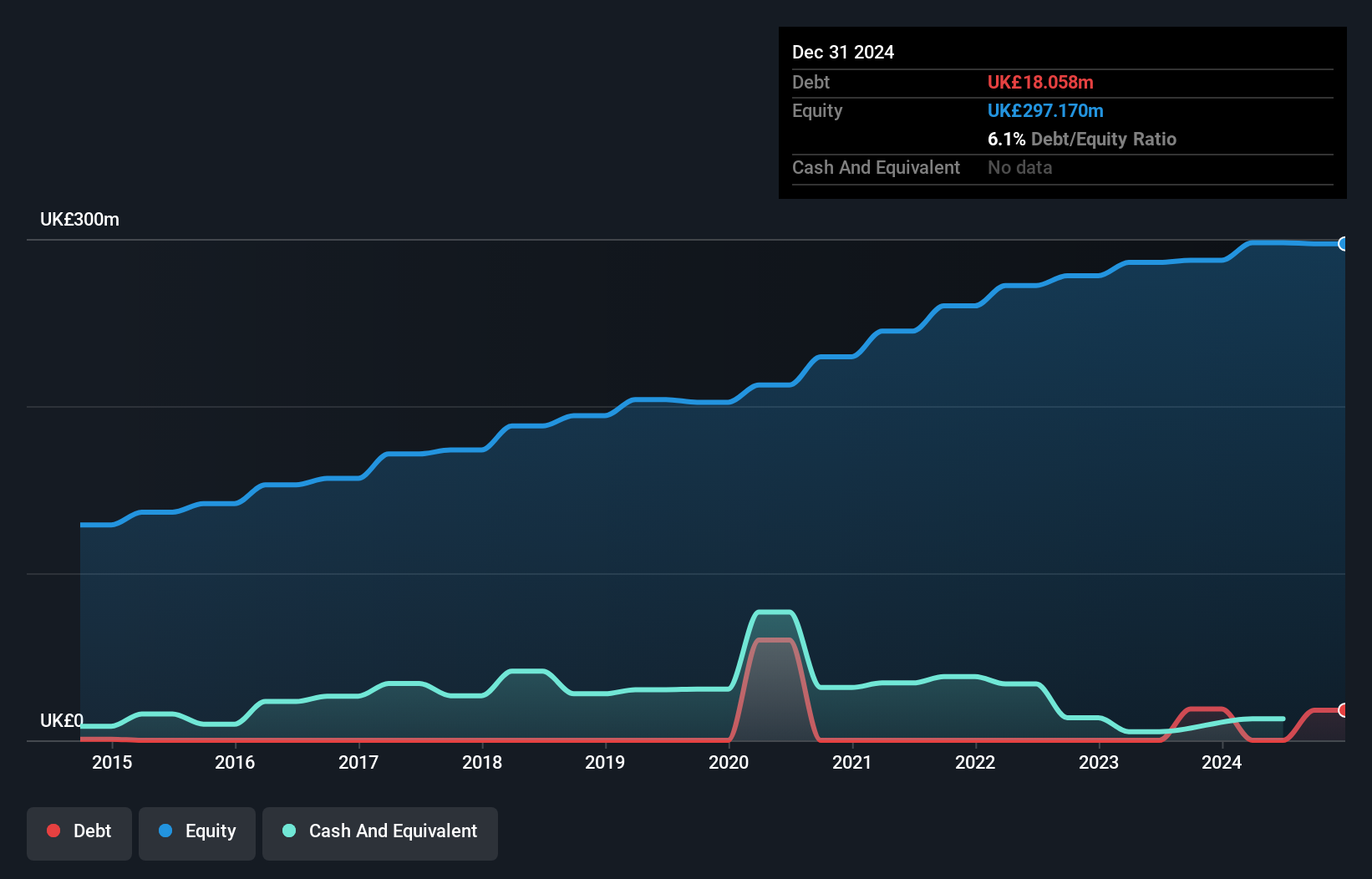

MJ Gleeson (LSE:GLE)

Simply Wall St Financial Health Rating: ★★★★★★

Overview: MJ Gleeson plc operates in the United Kingdom, focusing on house building and land promotion and sales, with a market cap of £281.08 million.

Operations: The company generates revenue through two primary segments: Gleeson Land, contributing £16.34 million, and Gleeson Homes, accounting for £329.01 million.

Market Cap: £281.08M

MJ Gleeson plc, with a market cap of £281.08 million, operates debt-free and demonstrates financial stability through its short-term assets (£368.2M) covering both short-term (£63.6M) and long-term liabilities (£16.7M). Despite recent negative earnings growth, the company maintains high-quality earnings and an experienced board with an average tenure of 5.3 years. The stock shows potential for price appreciation as analysts predict a 38.6% rise, though it faces challenges such as declining profit margins from 7.4% to 5.6% and an unstable dividend track record following a reduction to 7 pence per share in November 2024.

- Unlock comprehensive insights into our analysis of MJ Gleeson stock in this financial health report.

- Gain insights into MJ Gleeson's outlook and expected performance with our report on the company's earnings estimates.

Make It Happen

- Take a closer look at our UK Penny Stocks list of 445 companies by clicking here.

- Are these companies part of your investment strategy? Use Simply Wall St to consolidate your holdings into a portfolio and gain insights with our comprehensive analysis tools.

- Enhance your investing ability with the Simply Wall St app and enjoy free access to essential market intelligence spanning every continent.

Ready For A Different Approach?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Jump on the AI train with fast growing tech companies forging a new era of innovation.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Norman Broadbent might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About AIM:NBB

Norman Broadbent

Provides professional services in the United Kingdom and internationally.

High growth potential and good value.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.7% overvalued

TI

Community Contributor

Recently Updated Narratives

CO

composite32 on Astor Enerji ·

Astor Enerji will surge with a fair value of $140.43 in the next 3 years

Fair Value:₺140.4335.5% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RE

RecMag on Proximus ·

Proximus: The State-Backed Backup Plan with 7% Gross Yield and 15% Currency Upside.

Fair Value:€17.1356.7% undervalued

30 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AG

Agricola on IMPACT Silver ·

A case for for IMPACT Silver Corp (TSXV:IPT) to reach USD $4.52 (CAD $6.16) in 2026 (23 bagger in 1 year) and USD $5.76 (CAD $7.89) by 2030

Fair Value:CA$7.8996.2% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

101 followersusers have followed this narrative

10 commentsusers have commented on this narrative

20 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.8% undervalued

138 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3929.3% undervalued

930 followersusers have followed this narrative

6 commentsusers have commented on this narrative

23 likesusers have liked this narrative