- United Kingdom

- /

- Consumer Durables

- /

- LSE:BOOT

Discover 3 UK Exchange Stocks Priced Below Estimated Intrinsic Value

Reviewed by Simply Wall St

The UK stock market has been facing challenges, with the FTSE 100 index recently experiencing a dip due to weak trade data from China, highlighting concerns about global economic recovery. In this environment, identifying stocks priced below their estimated intrinsic value can offer potential opportunities for investors seeking to capitalize on undervaluation amidst broader market volatility.

Top 10 Undervalued Stocks Based On Cash Flows In The United Kingdom

| Name | Current Price | Fair Value (Est) | Discount (Est) |

| Fevertree Drinks (AIM:FEVR) | £6.605 | £13.12 | 49.7% |

| Gaming Realms (AIM:GMR) | £0.365 | £0.72 | 49.3% |

| Brickability Group (AIM:BRCK) | £0.628 | £1.25 | 49.6% |

| Zotefoams (LSE:ZTF) | £3.06 | £5.75 | 46.7% |

| GlobalData (AIM:DATA) | £2.02 | £3.75 | 46.1% |

| Tracsis (AIM:TRCS) | £5.04 | £9.71 | 48.1% |

| Duke Capital (AIM:DUKE) | £0.3075 | £0.58 | 47% |

| Vp (LSE:VP.) | £5.50 | £9.90 | 44.5% |

| Victrex (LSE:VCT) | £10.68 | £19.68 | 45.7% |

| Quartix Technologies (AIM:QTX) | £1.56 | £3.05 | 48.9% |

Let's dive into some prime choices out of the screener.

Young's Brewery (AIM:YNGA)

Overview: Young & Co.'s Brewery, P.L.C. operates and manages pubs and hotels in the United Kingdom with a market cap of £480.25 million.

Operations: Young & Co.'s Brewery, P.L.C. generates its revenue from the operation and management of pubs and hotels in the United Kingdom.

Estimated Discount To Fair Value: 17%

Young's Brewery is trading at £8.72, below its estimated fair value of £10.51, indicating potential undervaluation based on cash flows. Analysts agree on a 53.9% price rise despite diluted shares and low return on equity forecasts (5%). Earnings are expected to grow significantly at 28.7% annually, outpacing the UK market's 14.4%. Recent earnings show improved sales (£250 million) and net income (£20 million), supporting a dividend increase to 11.53 pence per share.

- Upon reviewing our latest growth report, Young's Brewery's projected financial performance appears quite optimistic.

- Delve into the full analysis health report here for a deeper understanding of Young's Brewery.

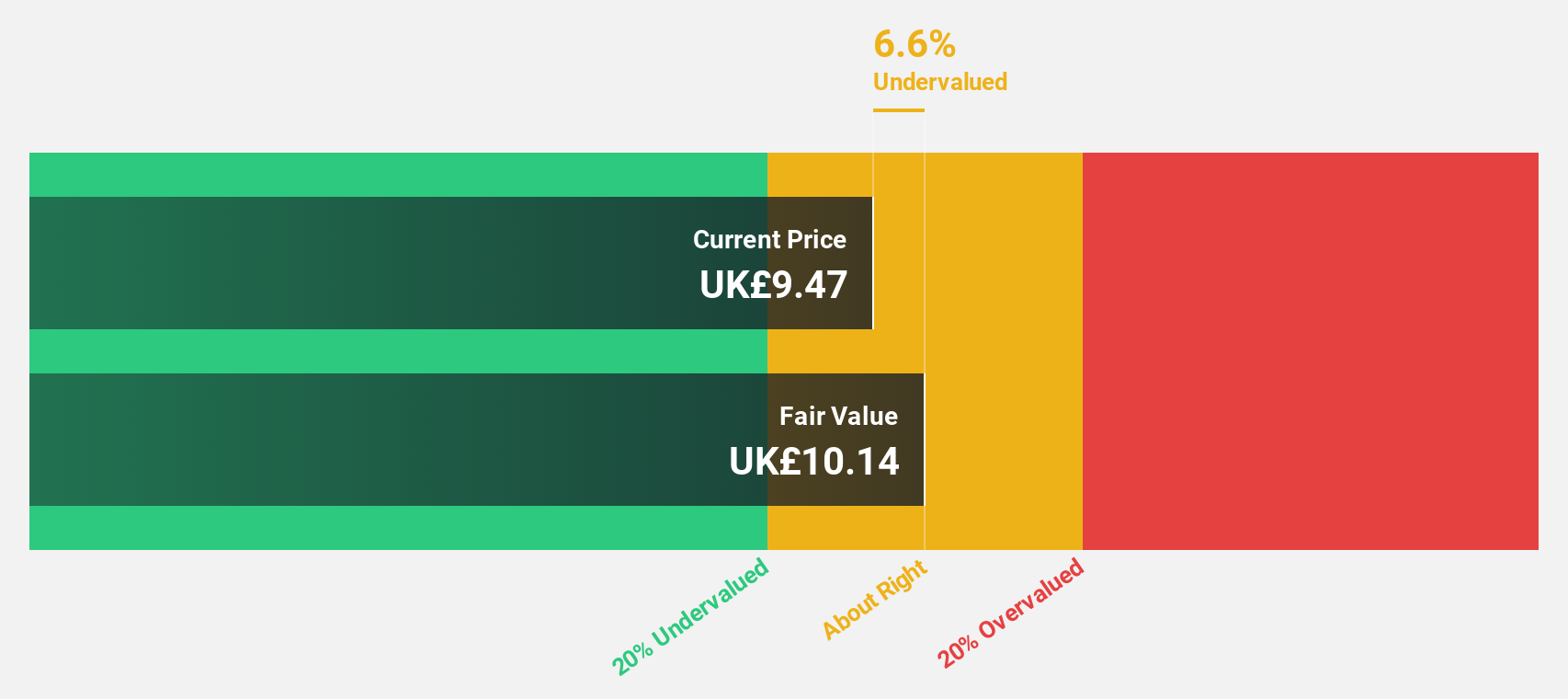

Henry Boot (LSE:BOOT)

Overview: Henry Boot PLC operates in the United Kingdom, focusing on property investment and development, land promotion, and construction activities, with a market cap of £300.69 million.

Operations: The company's revenue segments include £170.56 million from property investment and development, £28.37 million from land promotion, and £87.90 million from construction activities.

Estimated Discount To Fair Value: 24.1%

Henry Boot, trading at £2.25, is considered undervalued with a fair value estimate of £2.96, reflecting a 24.1% discount based on cash flow analysis. Earnings are projected to grow significantly at 25.48% annually, surpassing the UK market's growth rate of 14.4%. However, return on equity is forecasted to be low at 5.8%, and the dividend yield of 3.32% lacks adequate coverage by free cash flows despite promising revenue growth projections of 10.7%.

- Our expertly prepared growth report on Henry Boot implies its future financial outlook may be stronger than recent results.

- Unlock comprehensive insights into our analysis of Henry Boot stock in this financial health report.

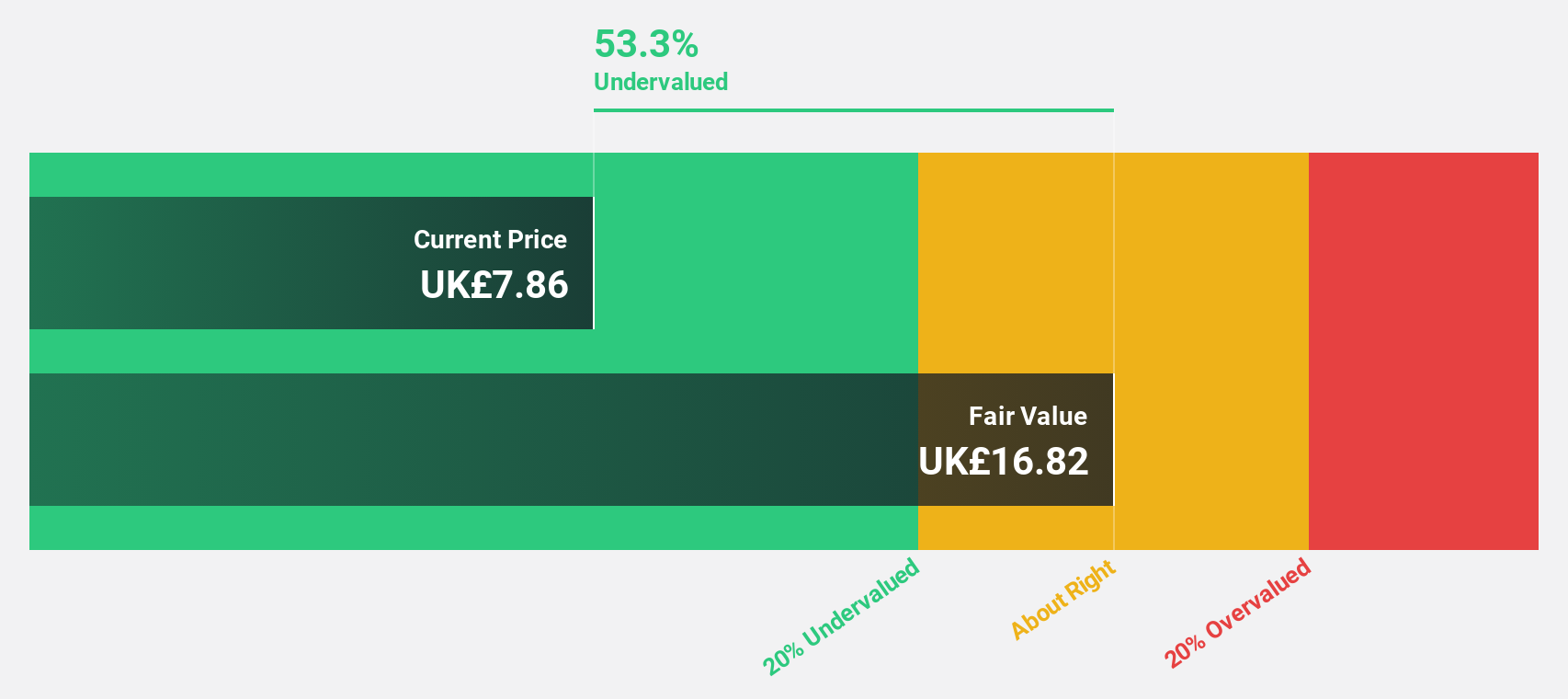

Victrex (LSE:VCT)

Overview: Victrex plc, with a market cap of £928.98 million, operates globally through its subsidiaries in the manufacture and sale of polymer solutions.

Operations: The company's revenue segments include £53 million from Medical and £240.60 million from Sustainable Solutions.

Estimated Discount To Fair Value: 45.7%

Victrex trades at £10.68, significantly below its estimated fair value of £19.68, suggesting undervaluation based on cash flows. Despite a drop in sales to £291 million and net income to £17.2 million for 2024, earnings are forecasted to grow significantly at 29.34% annually, outpacing the UK market's growth rate of 14.4%. However, profit margins have decreased from last year and the dividend yield of 5.58% is not well covered by earnings or free cash flows.

- Our comprehensive growth report raises the possibility that Victrex is poised for substantial financial growth.

- Click here and access our complete balance sheet health report to understand the dynamics of Victrex.

Turning Ideas Into Actions

- Gain an insight into the universe of 56 Undervalued UK Stocks Based On Cash Flows by clicking here.

- Have you diversified into these companies? Leverage the power of Simply Wall St's portfolio to keep a close eye on market movements affecting your investments.

- Join a community of smart investors by using Simply Wall St. It's free and delivers expert-level analysis on worldwide markets.

Want To Explore Some Alternatives?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

The New Payments ETF Is Live on NASDAQ:

Money is moving to real-time rails, and a newly listed ETF now gives investors direct exposure. Fast settlement. Institutional custody. Simple access.

Explore how this launch could reshape portfolios

Sponsored ContentValuation is complex, but we're here to simplify it.

Discover if Henry Boot might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About LSE:BOOT

Henry Boot

Engages in the property investment and development, land promotion, and construction activities in the United Kingdom.

Excellent balance sheet average dividend payer.

Similar Companies

Market Insights

Weekly Picks

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Recently Updated Narratives

An amazing opportunity to potentially get a 100 bagger

Amazon: Why the World’s Biggest Platform Still Runs on Invisible Economics

Sunrun Stock: When the Energy Transition Collides With the Cost of Capital

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)