Advertisement

- United Kingdom

- /

- Consumer Durables

- /

- LSE:BTRW

With Barratt Developments plc (LON:BDEV) It Looks Like You'll Get What You Pay For

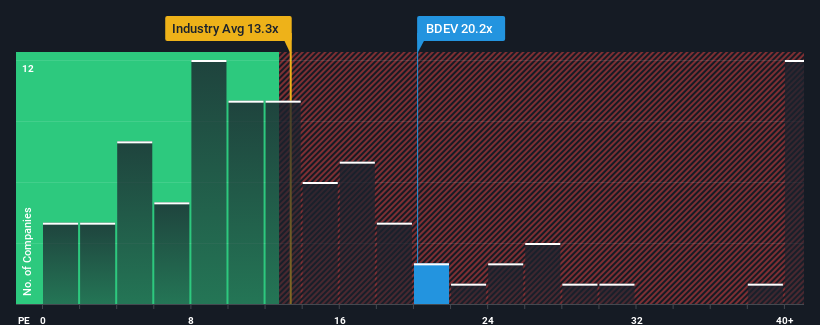

Barratt Developments plc's (LON:BDEV) price-to-earnings (or "P/E") ratio of 20.2x might make it look like a sell right now compared to the market in the United Kingdom, where around half of the companies have P/E ratios below 16x and even P/E's below 9x are quite common. However, the P/E might be high for a reason and it requires further investigation to determine if it's justified.

With earnings that are retreating more than the market's of late, Barratt Developments has been very sluggish. One possibility is that the P/E is high because investors think the company will turn things around completely and accelerate past most others in the market. You'd really hope so, otherwise you're paying a pretty hefty price for no particular reason.

View our latest analysis for Barratt Developments

Is There Enough Growth For Barratt Developments?

Barratt Developments' P/E ratio would be typical for a company that's expected to deliver solid growth, and importantly, perform better than the market.

Retrospectively, the last year delivered a frustrating 58% decrease to the company's bottom line. This means it has also seen a slide in earnings over the longer-term as EPS is down 44% in total over the last three years. Accordingly, shareholders would have felt downbeat about the medium-term rates of earnings growth.

Turning to the outlook, the next three years should generate growth of 22% each year as estimated by the analysts watching the company. With the market only predicted to deliver 14% per annum, the company is positioned for a stronger earnings result.

With this information, we can see why Barratt Developments is trading at such a high P/E compared to the market. It seems most investors are expecting this strong future growth and are willing to pay more for the stock.

The Bottom Line On Barratt Developments' P/E

We'd say the price-to-earnings ratio's power isn't primarily as a valuation instrument but rather to gauge current investor sentiment and future expectations.

We've established that Barratt Developments maintains its high P/E on the strength of its forecast growth being higher than the wider market, as expected. At this stage investors feel the potential for a deterioration in earnings isn't great enough to justify a lower P/E ratio. Unless these conditions change, they will continue to provide strong support to the share price.

Don't forget that there may be other risks. For instance, we've identified 3 warning signs for Barratt Developments (1 is significant) you should be aware of.

It's important to make sure you look for a great company, not just the first idea you come across. So take a peek at this free list of interesting companies with strong recent earnings growth (and a low P/E).

Valuation is complex, but we're here to simplify it.

Discover if Barratt Redrow might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About LSE:BTRW

Barratt Redrow

Engages in the housebuilding business in the United Kingdom.

Flawless balance sheet and fair value.

Similar Companies

Market Insights

Advertisement

Weekly Picks

CE

Ceazar on Sparc Al ·

When GPS fails: this small cap is fixing a $54B drone problem

Fair Value:CA$5.257.6% overvalued

9 followersusers have followed this narrative

0 commentsusers have commented on this narrative

2 likesusers have liked this narrative

SO

sorkdhkddlek on Marvell Technology ·

From AI Infrastructure Plumber to Full-Stack AI Factory Architect

Fair Value:US$14013.0% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

2 likesusers have liked this narrative

MI

MiningStockAnalyst on Aurelia Metals ·

Aurelia Metals Limited — Transitioning Into a Higher-Quality Mid-Tier Producer

Fair Value:AU$0.430.0% undervalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

1 likeusers have liked this narrative

CO

composite32 on TotalEnergies ·

Is This strategic transformation of TTE? Significant re-rating potential

Fair Value:€88.2913.0% undervalued

11 followersusers have followed this narrative

2 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Recently Updated Narratives

TH

TheInternationalInvestor on Hotel101 Global Holdings ·

Hotel101 Global: A Scalable Hospitality Platform Built to Compound

Fair Value:US$17.2362.2% undervalued

5 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

ST

StoxEurope on Sipef ·

Why I Invest in SIPEF?

Fair Value:€12117.8% undervalued

11 followersusers have followed this narrative

2 commentsusers have commented on this narrative

0 likesusers have liked this narrative

ES

Esteban on Tyler Technologies ·

Tyler Technologies 04-2026

Fair Value:US$157.05115.0% overvalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

KI

Kingman1152 on NVIDIA ·

NVIDIA will see a profit margin surge of 55% in the next 5 years

Fair Value:US$305.229.0% undervalued

67 followersusers have followed this narrative

2 commentsusers have commented on this narrative

23 likesusers have liked this narrative

AN

AnalystConsensusTarget on Microsoft ·

Analyst Commentary Highlights Microsoft AI Momentum and Upward Valuation Amid Growth and Competitive Risks

Fair Value:US$579.5726.7% undervalued

1391 followersusers have followed this narrative

2 commentsusers have commented on this narrative

11 likesusers have liked this narrative

TR

tripledub on Microsoft ·

Everyone's Terrified Microsoft Will Keep Spending. I'm Terrified They'll Stop.

Fair Value:US$3957.5% overvalued

53 followersusers have followed this narrative

3 commentsusers have commented on this narrative

43 likesusers have liked this narrative