Advertisement

- United Kingdom

- /

- Consumer Durables

- /

- LSE:BTRW

Returns At Barratt Developments (LON:BDEV) Appear To Be Weighed Down

If you're looking for a multi-bagger, there's a few things to keep an eye out for. Typically, we'll want to notice a trend of growing return on capital employed (ROCE) and alongside that, an expanding base of capital employed. Basically this means that a company has profitable initiatives that it can continue to reinvest in, which is a trait of a compounding machine. So, when we ran our eye over Barratt Developments' (LON:BDEV) trend of ROCE, we liked what we saw.

Return On Capital Employed (ROCE): What Is It?

For those who don't know, ROCE is a measure of a company's yearly pre-tax profit (its return), relative to the capital employed in the business. Analysts use this formula to calculate it for Barratt Developments:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

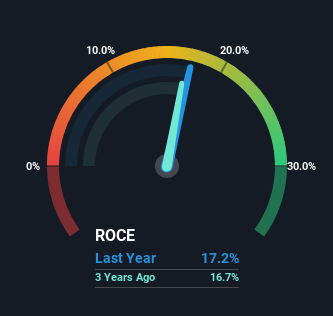

0.17 = UK£1.1b ÷ (UK£8.0b - UK£1.5b) (Based on the trailing twelve months to December 2022).

So, Barratt Developments has an ROCE of 17%. On its own, that's a standard return, however it's much better than the 12% generated by the Consumer Durables industry.

View our latest analysis for Barratt Developments

Above you can see how the current ROCE for Barratt Developments compares to its prior returns on capital, but there's only so much you can tell from the past. If you'd like to see what analysts are forecasting going forward, you should check out our free report for Barratt Developments.

How Are Returns Trending?

While the returns on capital are good, they haven't moved much. The company has consistently earned 17% for the last five years, and the capital employed within the business has risen 25% in that time. 17% is a pretty standard return, and it provides some comfort knowing that Barratt Developments has consistently earned this amount. Stable returns in this ballpark can be unexciting, but if they can be maintained over the long run, they often provide nice rewards to shareholders.

The Bottom Line

In the end, Barratt Developments has proven its ability to adequately reinvest capital at good rates of return. However, over the last five years, the stock has only delivered a 13% return to shareholders who held over that period. So because of the trends we're seeing, we'd recommend looking further into this stock to see if it has the makings of a multi-bagger.

Since virtually every company faces some risks, it's worth knowing what they are, and we've spotted 4 warning signs for Barratt Developments (of which 1 shouldn't be ignored!) that you should know about.

While Barratt Developments may not currently earn the highest returns, we've compiled a list of companies that currently earn more than 25% return on equity. Check out this free list here.

Valuation is complex, but we're here to simplify it.

Discover if Barratt Redrow might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About LSE:BTRW

Barratt Redrow

Engages in the housebuilding business in the United Kingdom.

Flawless balance sheet with reasonable growth potential.

Similar Companies

Market Insights

Advertisement

Weekly Picks

JO

Jolt_Communications on ZenaTech ·

ZenaTech: A big bet on the rise of AI drones and drones-as-a-service

Fair Value:US$6.8569.9% undervalued

25 followersusers have followed this narrative

0 commentsusers have commented on this narrative

1 likeusers have liked this narrative

TR

tripledub on Intuit ·

A Wonderful Business at a Not-So-Wonderful Price

Fair Value:US$50016.7% undervalued

19 followersusers have followed this narrative

0 commentsusers have commented on this narrative

17 likesusers have liked this narrative

FA

FA_Trader on A1 A.K. Koh Group Berhad ·

A1 A.K. Koh Group Berhad: A simple local food story that could ride on Visit Malaysia 2026

Fair Value:RM 0.3343.9% undervalued

7 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

KA

kaladorm on American Integrity Insurance Group ·

Priced for worse weather, but undervalued even for a high hurricane season

Fair Value:US$37.1949.9% undervalued

10 followersusers have followed this narrative

0 commentsusers have commented on this narrative

3 likesusers have liked this narrative

Recently Updated Narratives

VE

Vestra on Carnival Corporation & ·

CCL: Navigating the Waves of Record Demand and Fuel Headwinds

Fair Value:US$3734.6% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

VE

Vestra on Unity Software ·

U: The Great Pivot Toward AI-Powered Monetization

Fair Value:US$8176.0% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

VE

Vestra on MDxHealth ·

MDXH: Navigating the "Valley of Integration" Toward Diagnostic Dominance

Fair Value:US$5.1252.3% undervalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

YA

Yang_ on SoFi Technologies ·

SoFi Technologies: The Apex Aggregator and the Infrastructure of the Modern Financial System

Fair Value:US$22.9833.7% undervalued

49 followersusers have followed this narrative

0 commentsusers have commented on this narrative

36 likesusers have liked this narrative

PD

pdixit1 on Vertiv Holdings Co ·

The Infrastructure AI Cannot Be Built Without

Fair Value:US$408.6438.6% undervalued

40 followersusers have followed this narrative

3 commentsusers have commented on this narrative

18 likesusers have liked this narrative

ZA

ZayaanS on Pro Medicus ·

Pro Medicus: The Market Is Confusing a Lumpy Quarter With a Broken Business

Fair Value:AU$196.7840.2% undervalued

33 followersusers have followed this narrative

7 commentsusers have commented on this narrative

21 likesusers have liked this narrative

Trending Discussion

DS

dsfaggafgafg on Micron Technology ·

This is truly one of the worst predictions of all time. Its forward PE is 3.9x.

0

|0