Advertisement

- United Kingdom

- /

- Consumer Durables

- /

- LSE:BTRW

Barratt Developments plc's (LON:BDEV) Stock Going Strong But Fundamentals Look Weak: What Implications Could This Have On The Stock?

Most readers would already be aware that Barratt Developments' (LON:BDEV) stock increased significantly by 23% over the past month. However, we decided to pay close attention to its weak financials as we are doubtful that the current momentum will keep up, given the scenario. Specifically, we decided to study Barratt Developments' ROE in this article.

Return on Equity or ROE is a test of how effectively a company is growing its value and managing investors’ money. In short, ROE shows the profit each dollar generates with respect to its shareholder investments.

Check out our latest analysis for Barratt Developments

How Do You Calculate Return On Equity?

Return on equity can be calculated by using the formula:

Return on Equity = Net Profit (from continuing operations) ÷ Shareholders' Equity

So, based on the above formula, the ROE for Barratt Developments is:

9.5% = UK£530m ÷ UK£5.6b (Based on the trailing twelve months to June 2023).

The 'return' is the income the business earned over the last year. One way to conceptualize this is that for each £1 of shareholders' capital it has, the company made £0.09 in profit.

Why Is ROE Important For Earnings Growth?

So far, we've learned that ROE is a measure of a company's profitability. We now need to evaluate how much profit the company reinvests or "retains" for future growth which then gives us an idea about the growth potential of the company. Assuming everything else remains unchanged, the higher the ROE and profit retention, the higher the growth rate of a company compared to companies that don't necessarily bear these characteristics.

Barratt Developments' Earnings Growth And 9.5% ROE

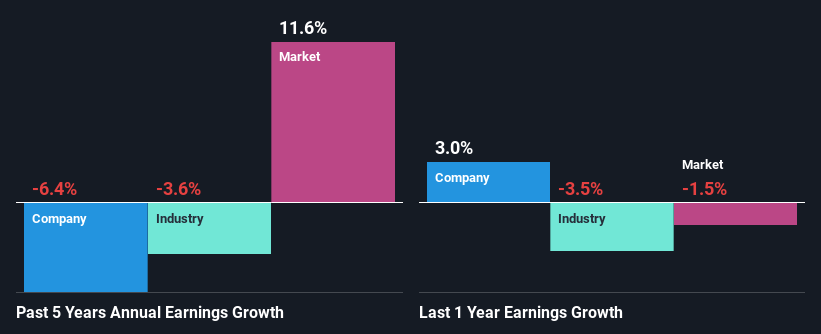

On the face of it, Barratt Developments' ROE is not much to talk about. However, its ROE is similar to the industry average of 10%, so we won't completely dismiss the company. But then again, Barratt Developments' five year net income shrunk at a rate of 6.4%. Bear in mind, the company does have a slightly low ROE. Therefore, the decline in earnings could also be the result of this.

Next, when we compared with the industry, which has shrunk its earnings at a rate of 3.6% in the same 5-year period, we still found Barratt Developments' performance to be quite bleak, because the company has been shrinking its earnings faster than the industry.

Earnings growth is an important metric to consider when valuing a stock. The investor should try to establish if the expected growth or decline in earnings, whichever the case may be, is priced in. Doing so will help them establish if the stock's future looks promising or ominous. Is Barratt Developments fairly valued compared to other companies? These 3 valuation measures might help you decide.

Is Barratt Developments Making Efficient Use Of Its Profits?

Barratt Developments has a high three-year median payout ratio of 56% (that is, it is retaining 44% of its profits). This suggests that the company is paying most of its profits as dividends to its shareholders. This goes some way in explaining why its earnings have been shrinking. The business is only left with a small pool of capital to reinvest - A vicious cycle that doesn't benefit the company in the long-run. To know the 2 risks we have identified for Barratt Developments visit our risks dashboard for free.

Additionally, Barratt Developments has paid dividends over a period of at least ten years, which means that the company's management is determined to pay dividends even if it means little to no earnings growth. Our latest analyst data shows that the future payout ratio of the company over the next three years is expected to be approximately 60%. Still, forecasts suggest that Barratt Developments' future ROE will drop to 7.4% even though the the company's payout ratio is not expected to change by much.

Summary

In total, we would have a hard think before deciding on any investment action concerning Barratt Developments. The company has seen a lack of earnings growth as a result of retaining very little profits and whatever little it does retain, is being reinvested at a very low rate of return. Having said that, we studied the latest analyst forecasts, and found that analysts are expecting the company's earnings growth to improve slightly. Sure enough, this could bring some relief to shareholders. To know more about the latest analysts predictions for the company, check out this visualization of analyst forecasts for the company.

Valuation is complex, but we're here to simplify it.

Discover if Barratt Redrow might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About LSE:BTRW

Barratt Redrow

Engages in the housebuilding business in the United Kingdom.

Flawless balance sheet and fair value.

Similar Companies

Market Insights

Advertisement

Weekly Picks

LO

Lou_Basenese on Cue Biopharma ·

Cue Biopharma (NASDAQ: CUE): The Scientist Behind Xolair Just Gave Cue a Next-Generation Shot at the Same Multi-Billion-Dollar Market

Fair Value:US$7061.6% undervalued

8 followersusers have followed this narrative

0 commentsusers have commented on this narrative

3 likesusers have liked this narrative

HE

HedgeY on AST SpaceMobile ·

AST SpaceMobile: The Boldest Direct-to-Cell Bet in Public Markets

Fair Value:US$17036.6% undervalued

32 followersusers have followed this narrative

0 commentsusers have commented on this narrative

10 likesusers have liked this narrative

FU

FundamentalFlow on Onto Innovation ·

Onto Innovation: The Advanced Packaging Chokepoint 51.3% undervalued intrinsic discount

Fair Value:US$38026.3% undervalued

23 followersusers have followed this narrative

0 commentsusers have commented on this narrative

6 likesusers have liked this narrative

MA

martinarauz on Nu Holdings ·

Investment Analysis (May 2026)

Fair Value:US$22.7448.8% undervalued

52 followersusers have followed this narrative

0 commentsusers have commented on this narrative

14 likesusers have liked this narrative

Recently Updated Narratives

KA

kapirey on Zijin Mining Group ·

Zijin Mining is a scaled, globally diversified mining platform

Fair Value:HK$60.1444.6% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

KA

kapirey on Yangzijiang Shipbuilding (Holdings) ·

Yangzijiang Shipbuilding Aims for a 30% Profit Margin Boost

Fair Value:S$5.4636.6% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

PA

pablo_ on Kodiak AI ·

Kodiak AI: The Tech Already Works — The Race Is Against Cash Burn

Fair Value:US$15.7956.4% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

GO

GoldenSands on QuantumScape ·

QuantumScape: A Mispriced Deep‑Tech Inflection Point With Multi‑Billion‑Dollar Optionality

Fair Value:US$8589.7% undervalued

124 followersusers have followed this narrative

3 commentsusers have commented on this narrative

36 likesusers have liked this narrative

CL

Clive_Thompson on Take-Two Interactive Software ·

Take-Two Interactive: The Calm Before the Storm NASDAQ: TTWO Last Price: $242.41 Date: May 15, 2026

Fair Value:US$276.9722.1% undervalued

56 followersusers have followed this narrative

0 commentsusers have commented on this narrative

14 likesusers have liked this narrative

NI

niteco on Honeywell International ·

Honeywell - The Demand-Side of the AI Infrastructure

Fair Value:US$320.1930.3% undervalued

46 followersusers have followed this narrative

0 commentsusers have commented on this narrative

19 likesusers have liked this narrative