- United Kingdom

- /

- Consumer Durables

- /

- AIM:CHH

Take Care Before Diving Into The Deep End On Churchill China plc (LON:CHH)

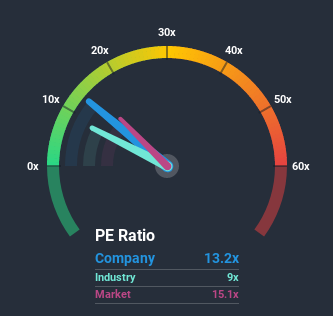

With a median price-to-earnings (or "P/E") ratio of close to 15x in the United Kingdom, you could be forgiven for feeling indifferent about Churchill China plc's (LON:CHH) P/E ratio of 13.2x. Although, it's not wise to simply ignore the P/E without explanation as investors may be disregarding a distinct opportunity or a costly mistake.

The earnings growth achieved at Churchill China over the last year would be more than acceptable for most companies. One possibility is that the P/E is moderate because investors think this respectable earnings growth might not be enough to outperform the broader market in the near future. If you like the company, you'd be hoping this isn't the case so that you could potentially pick up some stock while it's not quite in favour.

Check out our latest analysis for Churchill China

Does Churchill China Have A Relatively High Or Low P/E For Its Industry?

An inspection of the typical P/E's throughout Churchill China's industry may help to explain its fairly average P/E ratio. The image below shows that the Consumer Durables industry as a whole has a P/E ratio lower than the market. So we'd say there is little merit in the premise that the company's ratio being shaped by its industry at this time. In the context of the Consumer Durables industry's current setting, most of its constituents' P/E's would be expected to be toned down. Nonetheless, the greatest force on the company's P/E will be its own earnings growth expectations.

How Is Churchill China's Growth Trending?

The only time you'd be comfortable seeing a P/E like Churchill China's is when the company's growth is tracking the market closely.

Taking a look back first, we see that the company grew earnings per share by an impressive 26% last year. The latest three year period has also seen an excellent 71% overall rise in EPS, aided by its short-term performance. So we can start by confirming that the company has done a great job of growing earnings over that time.

In contrast to the company, the rest of the market is expected to decline by 14% over the next year, which puts the company's recent medium-term positive growth rates in a good light for now.

With this information, we find it odd that Churchill China is trading at a fairly similar P/E to the market. It looks like most investors are not convinced the company can maintain its recent positive growth rate in the face of a shrinking broader market.

The Key Takeaway

While the price-to-earnings ratio shouldn't be the defining factor in whether you buy a stock or not, it's quite a capable barometer of earnings expectations.

Our examination of Churchill China revealed its growing earnings over the medium-term aren't contributing to its P/E as much as we would have predicted, given the market is set to shrink. There could be some unobserved threats to earnings preventing the P/E ratio from matching this positive performance. Perhaps there is some hesitation about the company's ability to stay its recent course and swim against the current of the broader market turmoil. It appears some are indeed anticipating earnings instability, because this relative performance should normally provide a boost to the share price.

You should always think about risks. Case in point, we've spotted 2 warning signs for Churchill China you should be aware of, and 1 of them is significant.

If you're unsure about the strength of Churchill China's business, why not explore our interactive list of stocks with solid business fundamentals for some other companies you may have missed.

If you decide to trade Churchill China, use the lowest-cost* platform that is rated #1 Overall by Barron’s, Interactive Brokers. Trade stocks, options, futures, forex, bonds and funds on 135 markets, all from a single integrated account.Promoted

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com.

About AIM:CHH

Churchill China

Manufactures and sells ceramic and related products in the United Kingdom, rest of Europe, the United States, and internationally.

Flawless balance sheet, good value and pays a dividend.

Market Insights

Community Narratives