- United Kingdom

- /

- Consumer Durables

- /

- AIM:CHH

Churchill China plc's (LON:CHH) Stock Has Fared Decently: Is the Market Following Strong Financials?

Churchill China's (LON:CHH) stock up by 8.0% over the past three months. Since the market usually pay for a company’s long-term financial health, we decided to study the company’s fundamentals to see if they could be influencing the market. In this article, we decided to focus on Churchill China's ROE.

Return on equity or ROE is a key measure used to assess how efficiently a company's management is utilizing the company's capital. Simply put, it is used to assess the profitability of a company in relation to its equity capital.

View our latest analysis for Churchill China

How Do You Calculate Return On Equity?

The formula for return on equity is:

Return on Equity = Net Profit (from continuing operations) ÷ Shareholders' Equity

So, based on the above formula, the ROE for Churchill China is:

13% = UK£5.4m ÷ UK£41m (Based on the trailing twelve months to June 2020).

The 'return' refers to a company's earnings over the last year. One way to conceptualize this is that for each £1 of shareholders' capital it has, the company made £0.13 in profit.

What Has ROE Got To Do With Earnings Growth?

So far, we've learned that ROE is a measure of a company's profitability. Based on how much of its profits the company chooses to reinvest or "retain", we are then able to evaluate a company's future ability to generate profits. Generally speaking, other things being equal, firms with a high return on equity and profit retention, have a higher growth rate than firms that don’t share these attributes.

Churchill China's Earnings Growth And 13% ROE

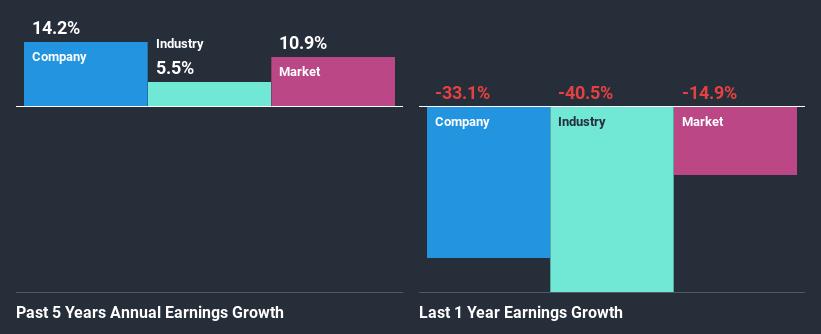

To start with, Churchill China's ROE looks acceptable. Further, the company's ROE compares quite favorably to the industry average of 6.4%. This probably laid the ground for Churchill China's moderate 14% net income growth seen over the past five years.

As a next step, we compared Churchill China's net income growth with the industry, and pleasingly, we found that the growth seen by the company is higher than the average industry growth of 5.5%.

Earnings growth is a huge factor in stock valuation. The investor should try to establish if the expected growth or decline in earnings, whichever the case may be, is priced in. Doing so will help them establish if the stock's future looks promising or ominous. Is Churchill China fairly valued compared to other companies? These 3 valuation measures might help you decide.

Is Churchill China Making Efficient Use Of Its Profits?

While the company did pay out a portion of its dividend in the past, it currently doesn't pay a dividend. We infer that the company has been reinvesting all of its profits to grow its business.

Upon studying the latest analysts' consensus data, we found that the company is expected to keep paying out approximately 47% of its profits over the next three years. As a result, Churchill China's ROE is not expected to change by much either, which we inferred from the analyst estimate of 13% for future ROE.

Summary

On the whole, we feel that Churchill China's performance has been quite good. Specifically, we like that the company is reinvesting a huge chunk of its profits at a high rate of return. This of course has caused the company to see substantial growth in its earnings. Having said that, looking at the current analyst estimates, we found that the company's earnings are expected to gain momentum. To know more about the latest analysts predictions for the company, check out this visualization of analyst forecasts for the company.

If you’re looking to trade Churchill China, open an account with the lowest-cost* platform trusted by professionals, Interactive Brokers. Their clients from over 200 countries and territories trade stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About AIM:CHH

Churchill China

Manufactures and sells ceramic and related products in the United Kingdom, rest of Europe, the United States, and internationally.

Flawless balance sheet, good value and pays a dividend.

Market Insights

Community Narratives