Advertisement

- United Kingdom

- /

- Consumer Durables

- /

- AIM:CFX

Shareholders Will Probably Hold Off On Increasing Colefax Group PLC's (LON:CFX) CEO Compensation For The Time Being

Under the guidance of CEO David Green, Colefax Group PLC (LON:CFX) has performed reasonably well recently. In light of this performance, CEO compensation will probably not be the main focus for shareholders as they go into the AGM on 23 September 2021. However, some shareholders will still be cautious of paying the CEO excessively.

View our latest analysis for Colefax Group

Comparing Colefax Group PLC's CEO Compensation With the industry

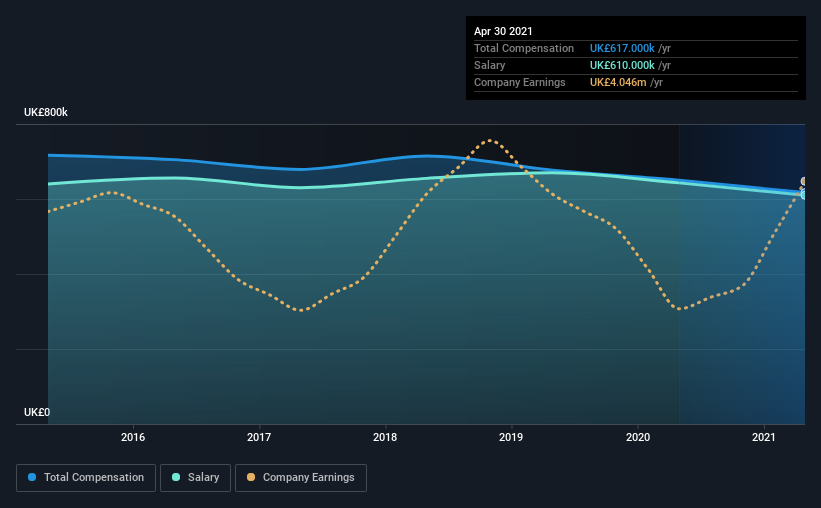

According to our data, Colefax Group PLC has a market capitalization of UK£57m, and paid its CEO total annual compensation worth UK£617k over the year to April 2021. That's slightly lower by 5.1% over the previous year. Notably, the salary which is UK£610.0k, represents most of the total compensation being paid.

On comparing similar-sized companies in the industry with market capitalizations below UK£145m, we found that the median total CEO compensation was UK£199k. Hence, we can conclude that David Green is remunerated higher than the industry median. Moreover, David Green also holds UK£12m worth of Colefax Group stock directly under their own name, which reveals to us that they have a significant personal stake in the company.

| Component | 2021 | 2020 | Proportion (2021) |

| Salary | UK£610k | UK£643k | 99% |

| Other | UK£7.0k | UK£7.0k | 1% |

| Total Compensation | UK£617k | UK£650k | 100% |

Talking in terms of the industry, salary represented approximately 69% of total compensation out of all the companies we analyzed, while other remuneration made up 31% of the pie. Colefax Group has gone down a largely traditional route, paying David Green a high salary, giving it preference over non-salary benefits. If salary dominates total compensation, it suggests that CEO compensation is leaning less towards the variable component, which is usually linked with performance.

Colefax Group PLC's Growth

Over the past three years, Colefax Group PLC has seen its earnings per share (EPS) grow by 5.9% per year. In the last year, its revenue changed by just 0.6%.

We would prefer it if there was revenue growth, but it is good to see a modest EPS growth at least. These two metrics are moving in different directions, so while it's hard to be confident judging performance, we think the stock is worth watching. Although we don't have analyst forecasts, you might want to assess this data-rich visualization of earnings, revenue and cash flow.

Has Colefax Group PLC Been A Good Investment?

With a total shareholder return of 19% over three years, Colefax Group PLC shareholders would, in general, be reasonably content. But they probably don't want to see the CEO paid more than is normal for companies around the same size.

In Summary...

Colefax Group pays its CEO a majority of compensation through a salary. Seeing that the company has put up a decent performance, only a few shareholders, if any at all, might have questions about the CEO pay in the upcoming AGM. However, any decision to raise CEO pay might be met with some objections from the shareholders given that the CEO is already paid higher than the industry average.

CEO compensation can have a massive impact on performance, but it's just one element. We've identified 2 warning signs for Colefax Group that investors should be aware of in a dynamic business environment.

Switching gears from Colefax Group, if you're hunting for a pristine balance sheet and premium returns, this free list of high return, low debt companies is a great place to look.

When trading Colefax Group or any other investment, use the platform considered by many to be the Professional's Gateway to the Worlds Market, Interactive Brokers. You get the lowest-cost* trading on stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About AIM:CFX

Colefax Group

Engages in the design, marketing, distribution, and retailing of furnishing fabrics, wallpapers, trimmings, upholstered furniture, and related products in the United Kingdom, the United States, Europe, and internationally.

Flawless balance sheet and good value.

Market Insights

Advertisement

Community Narratives

Finding The True Value Of A Logistics Powerhouse

Fair Value US$95.21|8.5% undervalued

NV

Community Contributor

Paradigm Biopharmaceuticals Will Lead Osteoarthritis Treatment with Zilosul's FDA Success

Fair Value AU$5.50|91.9% undervalued

AM

Community Contributor

Barrick Mining (ABX:CA): A Gold Hedge against a U.S. Shutdown

Fair Value CA$60.00|26.5% undervalued

GM

Community Contributor