- United Kingdom

- /

- Commercial Services

- /

- LSE:RPS

It Looks Like RPS Group plc's (LON:RPS) CEO May Expect Their Salary To Be Put Under The Microscope

Shareholders will probably not be too impressed with the underwhelming results at RPS Group plc (LON:RPS) recently. At the upcoming AGM on 28 April 2021, shareholders can hear from the board including their plans for turning around performance. This will be also be a chance where they can challenge the board on company direction and vote on resolutions such as executive remuneration. From our analysis, we think CEO compensation may need a review in light of the recent performance.

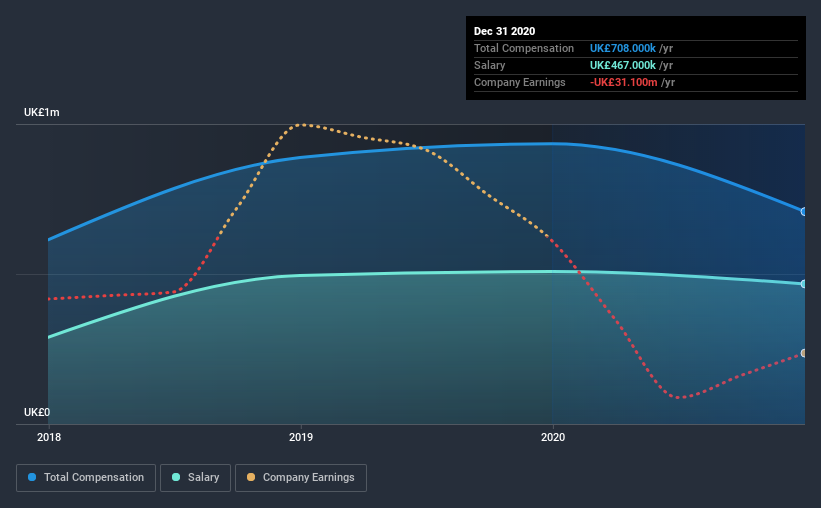

Check out our latest analysis for RPS Group

How Does Total Compensation For John Douglas Compare With Other Companies In The Industry?

According to our data, RPS Group plc has a market capitalization of UK£252m, and paid its CEO total annual compensation worth UK£708k over the year to December 2020. We note that's a decrease of 24% compared to last year. Notably, the salary which is UK£467.0k, represents most of the total compensation being paid.

On comparing similar companies from the same industry with market caps ranging from UK£143m to UK£574m, we found that the median CEO total compensation was UK£495k. Accordingly, our analysis reveals that RPS Group plc pays John Douglas north of the industry median. What's more, John Douglas holds UK£992k worth of shares in the company in their own name.

| Component | 2020 | 2019 | Proportion (2020) |

| Salary | UK£467k | UK£508k | 66% |

| Other | UK£241k | UK£426k | 34% |

| Total Compensation | UK£708k | UK£934k | 100% |

On an industry level, around 66% of total compensation represents salary and 34% is other remuneration. There isn't a significant difference between RPS Group and the broader market, in terms of salary allocation in the overall compensation package. If salary dominates total compensation, it suggests that CEO compensation is leaning less towards the variable component, which is usually linked with performance.

RPS Group plc's Growth

Over the last three years, RPS Group plc has shrunk its earnings per share by 47% per year. In the last year, its revenue is down 11%.

Overall this is not a very positive result for shareholders. And the impression is worse when you consider revenue is down year-on-year. It's hard to argue the company is firing on all cylinders, so shareholders might be averse to high CEO remuneration. Looking ahead, you might want to check this free visual report on analyst forecasts for the company's future earnings..

Has RPS Group plc Been A Good Investment?

The return of -60% over three years would not have pleased RPS Group plc shareholders. This suggests it would be unwise for the company to pay the CEO too generously.

In Summary...

Along with the business performing poorly, shareholders have suffered with poor share price returns on their investments, suggesting that there's little to no chance of them being in favor of a CEO pay raise. At the upcoming AGM, management will get a chance to explain how they plan to get the business back on track and address the concerns from investors.

While CEO pay is an important factor to be aware of, there are other areas that investors should be mindful of as well. That's why we did some digging and identified 2 warning signs for RPS Group that investors should think about before committing capital to this stock.

Important note: RPS Group is an exciting stock, but we understand investors may be looking for an unencumbered balance sheet and blockbuster returns. You might find something better in this list of interesting companies with high ROE and low debt.

When trading RPS Group or any other investment, use the platform considered by many to be the Professional's Gateway to the Worlds Market, Interactive Brokers. You get the lowest-cost* trading on stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About LSE:RPS

RPS Group

RPS Group plc, a professional services firm, provides consultancy services in the United Kingdom, Australia, the United States, Norway, the Netherlands, Ireland, Canada, and internationally.

Flawless balance sheet with reasonable growth potential.

Similar Companies

Market Insights

Community Narratives