Advertisement

- United Kingdom

- /

- Insurance

- /

- LSE:SBRE

Three Undervalued Small Caps In United Kingdom With Insider Buying

Simply Wall St

Reviewed by Simply Wall St

As the United Kingdom's markets navigate through global uncertainties, such as weak trade data from China impacting major indices like the FTSE 100 and FTSE 250, small-cap stocks present a unique opportunity for investors seeking growth potential amidst broader market challenges. In this context, identifying undervalued small-cap companies with insider buying can be particularly appealing, as these factors may suggest confidence in the company's prospects despite prevailing economic headwinds.

Top 10 Undervalued Small Caps With Insider Buying In The United Kingdom

| Name | PE | PS | Discount to Fair Value | Value Rating |

|---|---|---|---|---|

| Senior | 18.2x | 0.6x | 37.47% | ★★★★★★ |

| NWF Group | 8.2x | 0.1x | 39.15% | ★★★★★☆ |

| John Wood Group | NA | 0.2x | 41.22% | ★★★★★☆ |

| J D Wetherspoon | 14.9x | 0.4x | 12.97% | ★★★★★☆ |

| Genus | 171.7x | 2.0x | 14.36% | ★★★★★☆ |

| Headlam Group | NA | 0.2x | 26.73% | ★★★★★☆ |

| Marlowe | NA | 0.8x | 40.25% | ★★★★☆☆ |

| Optima Health | NA | 1.3x | 37.74% | ★★★★☆☆ |

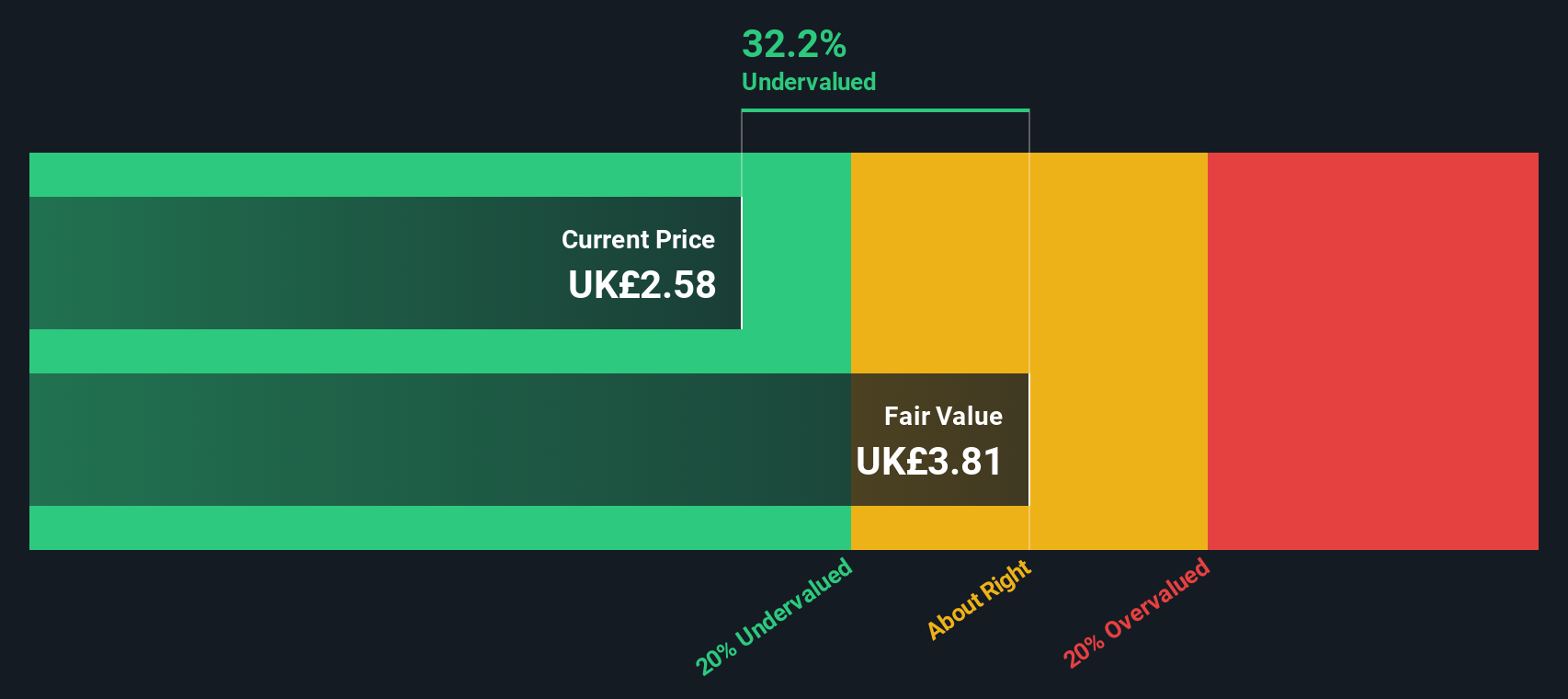

| Sabre Insurance Group | 11.6x | 1.5x | 12.44% | ★★★☆☆☆ |

| THG | NA | 0.4x | -271.68% | ★★★☆☆☆ |

Here we highlight a subset of our preferred stocks from the screener.

Domino's Pizza Group (LSE:DOM)

Simply Wall St Value Rating: ★★★★★☆

Overview: Domino's Pizza Group operates as a leading pizza delivery and carryout company, primarily generating revenue through sales to franchisees, corporate stores income, national advertising and ecommerce income, rental income from properties, and royalties with a market capitalization of approximately £1.53 billion.

Operations: The company's revenue model is primarily driven by sales to franchisees, contributing significantly to its overall income. Over recent periods, the net income margin has shown variability, reaching a high of 18.28% in June 2023 before declining to 11.44% by November 2024. Operating expenses have consistently risen alongside revenues, with general and administrative expenses forming a substantial part of these costs.

PE: 16.1x

Domino's Pizza Group, a smaller company in the UK market, shows potential for being undervalued. Despite high debt levels and a dip in profit margins from 18.2% to 11.4%, earnings are expected to grow by 10.09% annually. Insider confidence is evident with share repurchases totaling £90.1 million as of May 2024, covering 6.12% of shares since May 2023's buyback announcement. Although sales and net income have declined year-over-year, strategic initiatives aim to boost order counts and like-for-like sales throughout fiscal year 2024.

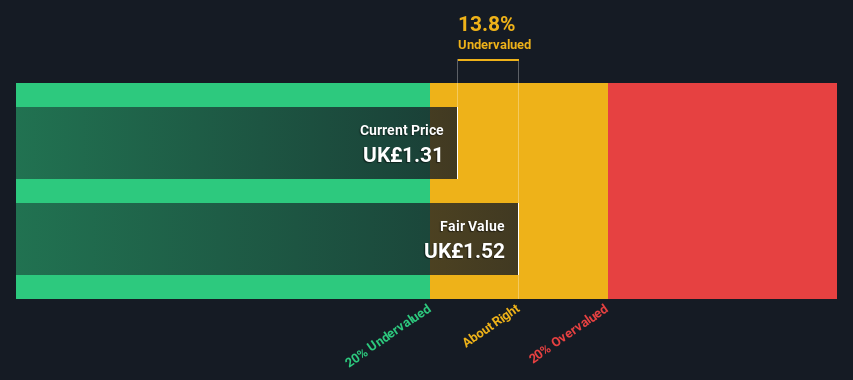

Mears Group (LSE:MER)

Simply Wall St Value Rating: ★★★★☆☆

Overview: Mears Group is a UK-based company specializing in management and maintenance services, with a market cap of £0.37 billion.

Operations: The company generates revenue primarily from management (£591.63 million) and maintenance services (£551.73 million). The net income margin has shown an upward trend, reaching 3.67% in the latest period. Operating expenses are a significant component of costs, with general and administrative expenses being a notable portion of these costs.

PE: 7.9x

Mears Group, a notable player in the UK market, has shown promising insider confidence with recent share purchases. Despite anticipated earnings decline over the next three years, their raised guidance for 2024 projects revenues of £1.13 billion. The company has actively repurchased shares, acquiring 5.6% of its capital for £20 million by June 2024. With a solid interim dividend increase to 4.75 pence per share and no customer deposits as liabilities, Mears presents an intriguing investment case amidst its sector's challenges and opportunities.

- Delve into the full analysis valuation report here for a deeper understanding of Mears Group.

Evaluate Mears Group's historical performance by accessing our past performance report.

Sabre Insurance Group (LSE:SBRE)

Simply Wall St Value Rating: ★★★☆☆☆

Overview: Sabre Insurance Group is a UK-based company specializing in underwriting motor insurance, including taxi, motorcycle, and other motor vehicle coverage, with a market capitalization of £0.23 billion.

Operations: Sabre Insurance Group's revenue primarily stems from its Motor Vehicle segment, excluding taxis, which significantly surpasses the Taxi and Motorcycle segments. The company's cost of goods sold (COGS) has shown fluctuations over time, impacting its gross profit margin, which reached 37.30% in mid-2024. Operating expenses have varied but remain a critical component of overall costs alongside non-operating expenses.

PE: 11.6x

Sabre Insurance Group, a UK-based company, recently reported a rise in gross written premiums to £186.5 million for the first nine months of 2024, up from £162.2 million the previous year. This growth suggests potential despite its reliance on external borrowing for funding, which carries inherent risks. Insider confidence is evident with recent share purchases by key personnel during this period. Earnings are projected to grow at 15.73% annually, indicating promising future prospects in the insurance sector.

- Unlock comprehensive insights into our analysis of Sabre Insurance Group stock in this valuation report.

Understand Sabre Insurance Group's track record by examining our Past report.

Key Takeaways

- Click this link to deep-dive into the 25 companies within our Undervalued UK Small Caps With Insider Buying screener.

- Shareholder in one or more of these companies? Ensure you're never caught off-guard by adding your portfolio in Simply Wall St for timely alerts on significant stock developments.

- Simply Wall St is your key to unlocking global market trends, a free user-friendly app for forward-thinking investors.

Interested In Other Possibilities?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About LSE:SBRE

Sabre Insurance Group

Through its subsidiaries, engages in writing of general insurance for motor vehicles in the United Kingdom.

Very undervalued with excellent balance sheet.

Market Insights

Advertisement

Community Narratives

BMW cruising ahead with new EVs and premium models to boost revenue 5%

Fair Value €135.07|45.0% undervalued

UN

Community Contributor

EU#2 - From Humble Beginnings to Global Powerhouse

Fair Value DKK 851.04|47.8% undervalued

TO

Community Contributor