Advertisement

- United Kingdom

- /

- Professional Services

- /

- AIM:TEK

What Can The Trends At Tekcapital (LON:TEK) Tell Us About Their Returns?

If you're looking for a multi-bagger, there's a few things to keep an eye out for. In a perfect world, we'd like to see a company investing more capital into its business and ideally the returns earned from that capital are also increasing. Ultimately, this demonstrates that it's a business that is reinvesting profits at increasing rates of return. Speaking of which, we noticed some great changes in Tekcapital's (LON:TEK) returns on capital, so let's have a look.

What is Return On Capital Employed (ROCE)?

For those who don't know, ROCE is a measure of a company's yearly pre-tax profit (its return), relative to the capital employed in the business. To calculate this metric for Tekcapital, this is the formula:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

0.11 = US$2.9m ÷ (US$26m - US$239k) (Based on the trailing twelve months to May 2020).

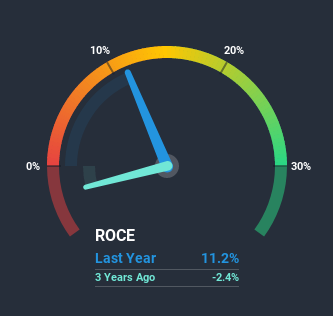

So, Tekcapital has an ROCE of 11%. In absolute terms, that's a pretty normal return, and it's somewhat close to the Professional Services industry average of 13%.

View our latest analysis for Tekcapital

Historical performance is a great place to start when researching a stock so above you can see the gauge for Tekcapital's ROCE against it's prior returns. If you'd like to look at how Tekcapital has performed in the past in other metrics, you can view this free graph of past earnings, revenue and cash flow.

What Does the ROCE Trend For Tekcapital Tell Us?

The fact that Tekcapital is now generating some pre-tax profits from its prior investments is very encouraging. About five years ago the company was generating losses but things have turned around because it's now earning 11% on its capital. In addition to that, Tekcapital is employing 509% more capital than previously which is expected of a company that's trying to break into profitability. This can tell us that the company has plenty of reinvestment opportunities that are able to generate higher returns.

In Conclusion...

In summary, it's great to see that Tekcapital has managed to break into profitability and is continuing to reinvest in its business. And since the stock has fallen 58% over the last five years, there might be an opportunity here. With that in mind, we believe the promising trends warrant this stock for further investigation.

Tekcapital does come with some risks though, we found 4 warning signs in our investment analysis, and 1 of those shouldn't be ignored...

For those who like to invest in solid companies, check out this free list of companies with solid balance sheets and high returns on equity.

If you’re looking to trade Tekcapital, open an account with the lowest-cost* platform trusted by professionals, Interactive Brokers. Their clients from over 200 countries and territories trade stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

Valuation is complex, but we're here to simplify it.

Discover if Tekcapital might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About AIM:TEK

Tekcapital

Provides a range of technology transfer services to universities and corporate clients in the United Kingdom and the United States.

Flawless balance sheet slight.

Market Insights

Advertisement

Community Narratives

SSAB in pole position when it comes to the combination of steel tariffs and the EU's investment drive

Fair Value SEK 86.87|35.6% undervalued

PI

Community Contributor

The Future of Lennar and Homebuilding Faces Short Term Challenges with Potential for Long Term Growth

Fair Value US$162.49|35.2% undervalued

ZE

Community Contributor

Saudi Aramco (SASE:2222): Not The Sexiest High Dividend Yield Stock, But One With Interesting 'Convertible-Like' Qualities

Fair Value ر.س37.02|30.0% undervalued

EV

Community Contributor