- United Kingdom

- /

- Professional Services

- /

- AIM:NBB

Take Care Before Jumping Onto Norman Broadbent plc (LON:NBB) Even Though It's 27% Cheaper

Unfortunately for some shareholders, the Norman Broadbent plc (LON:NBB) share price has dived 27% in the last thirty days, prolonging recent pain. The recent drop has obliterated the annual return, with the share price now down 6.8% over that longer period.

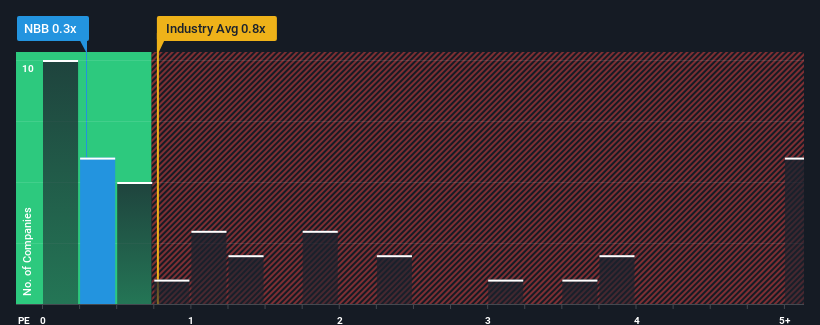

Even after such a large drop in price, there still wouldn't be many who think Norman Broadbent's price-to-sales (or "P/S") ratio of 0.3x is worth a mention when the median P/S in the United Kingdom's Professional Services industry is similar at about 0.8x. While this might not raise any eyebrows, if the P/S ratio is not justified investors could be missing out on a potential opportunity or ignoring looming disappointment.

View our latest analysis for Norman Broadbent

How Has Norman Broadbent Performed Recently?

The recent revenue growth at Norman Broadbent would have to be considered satisfactory if not spectacular. Perhaps the expectation moving forward is that the revenue growth will track in line with the wider industry for the near term, which has kept the P/S subdued. If you like the company, you'd be hoping this isn't the case so that you could potentially pick up some stock while it's not quite in favour.

Want the full picture on earnings, revenue and cash flow for the company? Then our free report on Norman Broadbent will help you shine a light on its historical performance.Is There Some Revenue Growth Forecasted For Norman Broadbent?

In order to justify its P/S ratio, Norman Broadbent would need to produce growth that's similar to the industry.

Retrospectively, the last year delivered a decent 4.4% gain to the company's revenues. This was backed up an excellent period prior to see revenue up by 74% in total over the last three years. So we can start by confirming that the company has done a great job of growing revenues over that time.

Comparing that recent medium-term revenue trajectory with the industry's one-year growth forecast of 5.8% shows it's noticeably more attractive.

With this information, we find it interesting that Norman Broadbent is trading at a fairly similar P/S compared to the industry. It may be that most investors are not convinced the company can maintain its recent growth rates.

The Key Takeaway

Norman Broadbent's plummeting stock price has brought its P/S back to a similar region as the rest of the industry. Typically, we'd caution against reading too much into price-to-sales ratios when settling on investment decisions, though it can reveal plenty about what other market participants think about the company.

To our surprise, Norman Broadbent revealed its three-year revenue trends aren't contributing to its P/S as much as we would have predicted, given they look better than current industry expectations. When we see strong revenue with faster-than-industry growth, we can only assume potential risks are what might be placing pressure on the P/S ratio. It appears some are indeed anticipating revenue instability, because the persistence of these recent medium-term conditions would normally provide a boost to the share price.

Plus, you should also learn about these 4 warning signs we've spotted with Norman Broadbent (including 1 which is a bit unpleasant).

If companies with solid past earnings growth is up your alley, you may wish to see this free collection of other companies with strong earnings growth and low P/E ratios.

Valuation is complex, but we're here to simplify it.

Discover if Norman Broadbent might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About AIM:NBB

Norman Broadbent

Provides professional services in the United Kingdom and internationally.

Good value with adequate balance sheet.