- United Kingdom

- /

- Professional Services

- /

- AIM:MRL

Here's Why Marlowe plc's (LON:MRL) CEO Compensation Is The Least Of Shareholders' Concerns

Marlowe plc (LON:MRL) has exhibited strong share price growth in the past few years. However, its earnings growth has not kept up, suggesting that there may be something amiss. Some of these issues will occupy shareholders' minds as the AGM rolls around on 15 September 2021. They will be able to influence managerial decisions through the exercise of their voting power on resolutions, such as CEO remuneration and other matters, which may influence future company prospects. From the data that we gathered, we think that shareholders should hold off on a raise on CEO compensation until performance starts to show some improvement.

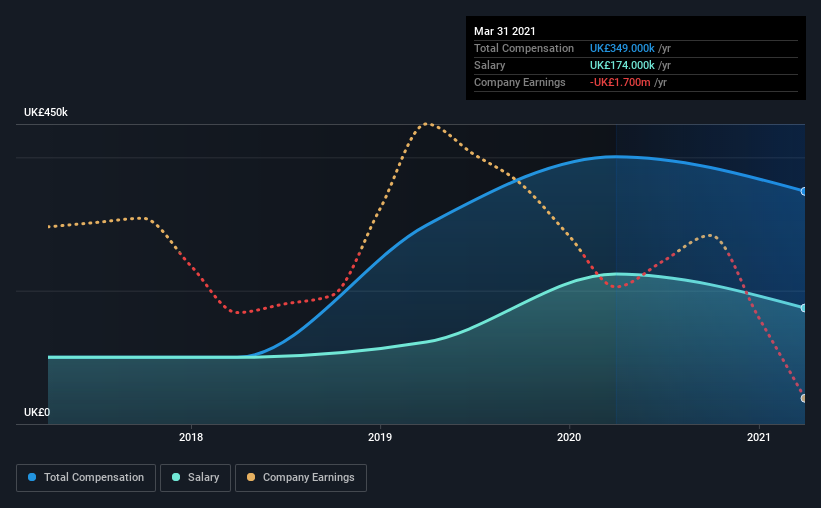

See our latest analysis for Marlowe

How Does Total Compensation For Alex Dacre Compare With Other Companies In The Industry?

At the time of writing, our data shows that Marlowe plc has a market capitalization of UK£676m, and reported total annual CEO compensation of UK£349k for the year to March 2021. That's a notable decrease of 13% on last year. While we always look at total compensation first, our analysis shows that the salary component is less, at UK£174k.

On examining similar-sized companies in the industry with market capitalizations between UK£291m and UK£1.2b, we discovered that the median CEO total compensation of that group was UK£498k. So it looks like Marlowe compensates Alex Dacre in line with the median for the industry. What's more, Alex Dacre holds UK£41m worth of shares in the company in their own name, indicating that they have a lot of skin in the game.

| Component | 2021 | 2020 | Proportion (2021) |

| Salary | UK£174k | UK£225k | 50% |

| Other | UK£175k | UK£176k | 50% |

| Total Compensation | UK£349k | UK£401k | 100% |

On an industry level, around 66% of total compensation represents salary and 34% is other remuneration. Marlowe sets aside a smaller share of compensation for salary, in comparison to the overall industry. It's important to note that a slant towards non-salary compensation suggests that total pay is tied to the company's performance.

Marlowe plc's Growth

Marlowe plc has reduced its earnings per share by 18% a year over the last three years. In the last year, its revenue is up 3.6%.

Few shareholders would be pleased to read that EPS have declined. And the modest revenue growth over 12 months isn't much comfort against the reduced EPS. These factors suggest that the business performance wouldn't really justify a high pay packet for the CEO. Moving away from current form for a second, it could be important to check this free visual depiction of what analysts expect for the future.

Has Marlowe plc Been A Good Investment?

Boasting a total shareholder return of 61% over three years, Marlowe plc has done well by shareholders. So they may not be at all concerned if the CEO were to be paid more than is normal for companies around the same size.

To Conclude...

While the return to shareholders does look promising, it's hard to ignore the lack of earnings growth and this makes us question whether these strong returns will continue. Shareholders should make the most of the coming opportunity to question the board on key concerns they may have and revisit their investment thesis with regards to the company.

While CEO pay is an important factor to be aware of, there are other areas that investors should be mindful of as well. That's why we did some digging and identified 1 warning sign for Marlowe that you should be aware of before investing.

Switching gears from Marlowe, if you're hunting for a pristine balance sheet and premium returns, this free list of high return, low debt companies is a great place to look.

If you decide to trade Marlowe, use the lowest-cost* platform that is rated #1 Overall by Barron’s, Interactive Brokers. Trade stocks, options, futures, forex, bonds and funds on 135 markets, all from a single integrated account. Promoted

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About AIM:MRL

Good value with adequate balance sheet.

Market Insights

Community Narratives